By: Blake Heinman, Senior Associate (Quantitative Research)

Key Takeaways

- SMCI’s 30% stock drop, due to a short-seller report, creates potential opportunities for competitors like Dell and HPE to step in and grab market share.

- The AI server market is expected to grow to $430 billion by 2030, offering significant growth potential for those operating in the space.

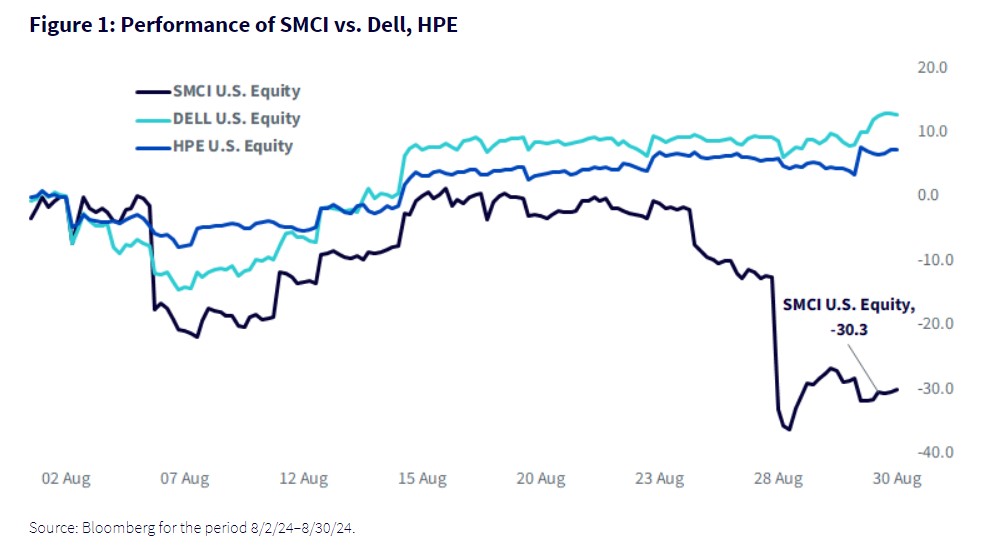

Super Micro Computer (SMCI), a leading provider of AI servers, saw its stock price plummet by over 30% following the release of a short-seller report from Hindenburg Research on August 27. The report alleges that SMCI has been misrepresenting its sales on financial statements and engaging in other nefarious activities. Compounding these concerns, the company recently delayed submitting its annual filings to the SEC, raising further doubts about its financial reporting credibility. These revelations could potentially open the door for some of the more traditional competitors to capture a larger share of the AI server market, a sector in which SMCI is a dominant player.

Background

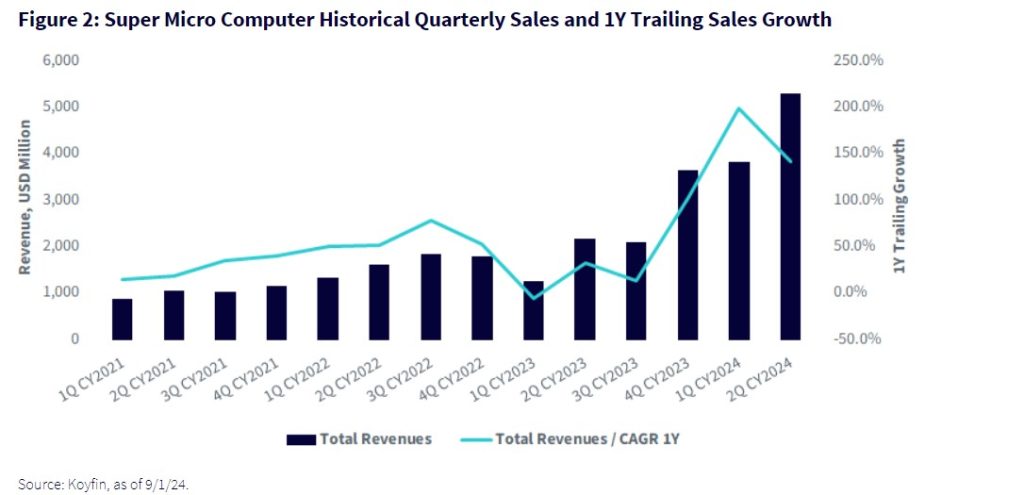

Super Micro Computer, once an obscure small cap, has emerged as a top AI market performer, soaring 1,000% over the last three years to recently earn a spot in the S&P 500. As a key provider of AI servers, primarily built around Nvidia’s most advanced chips, SMCI has experienced significant sales growth since the start of 2023. The company’s annual revenue jumped from $5.2 billion in 2022 to $7.1 billion in 2023, and then to an impressive $14.9 billion in 2024.1 In the most recent quarter, it reported $5.3 billion in revenue, a year-over-year increase of 140%, and is on track to hit the Wall Street consensus estimate of over $28 billion for the end of this fiscal year.1

Approximately 92% of SMCI’s business is driven by its AI server segment, which integrates essential components—such as GPUs, CPUs, memory modules and liquid cooling systems—into high-performance AI servers designed for data center deployment.

At the Computex conference earlier this year, SMCI showcased its AI servers powered by Nvidia GPUs, emphasizing their key role in the AI revolution. These servers integrate up to several hundred thousand chips,2 working alongside Nvidia GPUs. While Nvidia CEO Jensen Huang called GPUs the “brains” of AI, he acknowledged that their true power emerges only when combined with other essential components like CPUs, memory and network switches from various semiconductor firms.2 This intricate hardware ecosystem is crucial for AI training and inference, and SMCI, among others, package these elements into servers for deployment in data centers.

The Hindenburg Report

The Hindenburg Research report casts a long shadow over SMCI’s recent success. The short seller highlights historical issues with the company’s accounting practices, including a delisting back in 2018 that led to the firing of most of the staff involved.3 Shockingly, some of these personnel were later rehired, raising red flags about the company’s internal controls.

The report also raises serious concerns about “channel stuffing,” a practice where a company inflates its sales by sending more products to distributors than distributors can sell. Even more alarming, Hindenburg suggests that SMCI might be funneling sales to entities on the U.S. government’s export ban lists or even the Office of Foreign Assets Control (OFAC) list, possibly through partner intermediaries or shell companies abroad. If true, this could mean that Nvidia’s most advanced chips are finding their way into Russia and China, potentially putting SMCI in the crosshairs of the U.S. government.

Moreover, the report highlights significant issues with SMCI’s customer service, pointing to poor post-sales support and dissatisfied clients. Allegations include faulty equipment and inadequate client service support, with just 20 personnel reportedly managing all service needs across the U.S. Some clients, according to the report, have already begun transitioning to more trusted competitors like Dell and Hewlett Packard Enterprise (HPE), with companies such as Tesla, Amazon and DigitalOcean among those mentioned.

The AI Server Market

The AI server market is very competitive, with major players like Dell, HPE, IBM and Oracle aggressively targeting the enterprise segment. Smaller companies, such as ASUS, are also vying for market share. ASUS has ambitious goals to increase its footprint fivefold from 2022 year-end sales numbers.4 With operating margins hovering just above 10%, competition remains intense. SMCI has garnered significant attention due to its concentrated focus in this space, whereas industry veterans like Dell and HPE derive approximately 50% of their revenue from their broader AI and cloud infrastructure segments, with a strong emphasis on growth.

Recently, Dell reported earnings that exceeded expectations, with its server and networking segment growing 80% year over year, amounting to $11.6 billion in revenue. The company provided Q3 guidance of $24–$25 billion in total revenue, with its server group expected to see a 30% increase from this quarter, bringing in $15 billion.5 Dell is also anticipating tailwinds from the device upgrade cycle and the introduction of AI PCs in the second half of the year.

HPE is similarly benefiting from growing demand for AI servers, which contributed $1.6 billion to the recent quarter’s total revenue of $7.7 billion. The firm beat sales expectations by nearly $50 million,6 but reported lower margins than expected, causing investors to punish the stock. With approximately 50% of HPE’s revenue coming from the server segment, we would expect AI servers to continue to become more important to the business—with an opportunity to tie in higher margin services alongside this offering in the future.

On the other hand, SMCI recently reported $5.3 billion in sales and projected $6.5 billion for Q3, aiming for over $28 billion in revenue for the 2024 calendar year, marking a 90% increase from the previous year. However, the release of the Hindenburg report raises the possibility that a portion of SMCI’s sales—a meaningful amount of market share—could shift to competitors or be lost entirely if linked to channel stuffing activities or banned entities.

Valuations

The AI server market is projected to grow at a 30% compound annual growth rate (CAGR) to over $430 billion by 2033, according to Statista.7 With many firms seeking to capitalize on this strong growth opportunity, the recent information released by the Hindenburg report could lead to a shift in market dynamics.

Following SMCI’s stock sell-off in reaction to the report, the firm’s valuation multiples took a hit. It has historically traded at a premium, but has since aligned more closely with its competitors, with most peers now trading around 1x FY25 sales or 10x FY26 earnings. If the allegations in the Hindenburg report are substantiated, it could create opportunities for other players to capture market share.

Dell and HPE are particularly well positioned to benefit from SMCI’s challenges. By attracting SMCI’s disgruntled customers or those wary of associating with a company under scrutiny, they could experience higher-than-expected sales growth. This scenario might also drive multiple expansion, making the stocks attractive from both growth and valuation perspectives.

Bank of America’s $155 price target for Dell,8 based on a 15x EPS 2026 multiple, reflects confidence in such expansion. Additionally, continued capital expenditures by major hyperscalers indicate continued strong investment in AI infrastructure, supporting ongoing sales growth.

The market may not yet fully recognize Dell and HPE’s potential to capitalize on SMCI’s difficulties, presenting a nice opportunity ahead for these two trusted, long-standing server providers.

Conclusion

As AI enterprise adoption accelerates, the AI server hardware market offers a compelling investment opportunity. While SMCI’s recent challenges introduce significant risk, other players like Dell and HPE are well positioned to capture market share. These trusted industry players stand to benefit from SMCI’s setbacks, making them attractive options for investors looking to capitalize on the growing demand for AI infrastructure.

This post first appeared on September 19, 2024 on WisdomTree blog

PHOTO CREDIT: https://www.shutterstock.com/g/Sittipong+Phokawattana

VIA SHUTTERSTOCK

FOOTNOTES:

1 Koyfin, as of 9/1/24.

2 Super Micro Computer Inc at Taipei Computer Association COMPUTEX Trade Show, 6/5/24.

3 Hindenburg Research, “Super Micro: Fresh Evidence of Accounting Manipulation, Sibling Self-Dealing and Sanctions Evasion at This AI High Flyer,” hindenburgresearch.com, 8/27/24.

4 ASUS FY Q2 2024 Earnings Report Presentation, 8/7/24.

5 Dell FY Q2 2025 Earnings Call, 8/29/24.

6 HPE Q3 2024 Earnings Call, 9/4/24.

7 “Value of the Worldwide AI Server Market from 2023 to 2033,” Statista, 6/7/24.

8 Bank of America Equity Research, as of 8/29/24.

DISCLOSURES:

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

{kind=link}