By: Toby Warburton. CFA, Ph.D.

Equity markets, led by the US, are on track to finish the year close to or at all-time highs. Since the Global Financial Crisis (GFC), developed market equity returns have been remarkably strong, and above long-term averages. Returns recently have been driven by a concentrated band of stocks. We reexamine the current market environment, assessing what it may mean for future returns.

The Death of the Cult of Equities

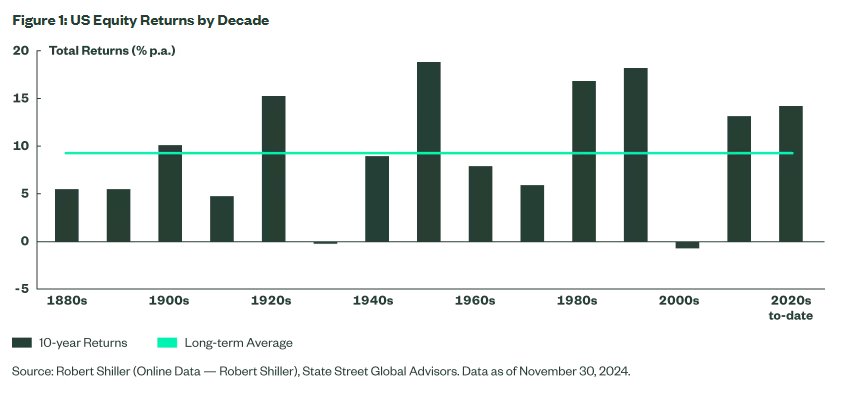

The phrase “The Death of the Cult of Equities” reemerged again in the early part of the last decade, echoing a refrain first launched in a Bloomberg Businessweek article in 1979. In the decade plus since that publication, developed market equities, as measured by the MSCI World Index, have been in robust health, returning 12% per annum. Since the inception of the MSCI World Index, equities have returned 9.7%. In the US equity market, where we have a significantly longer history, a similar story holds, with recent returns above average.

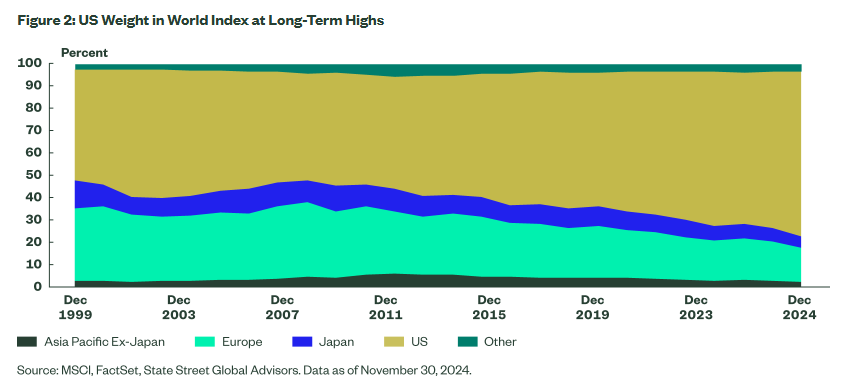

Returns in recent years, however, have become more and more concentrated in the US equity market, and in a few stocks in that market. The US equity market currently makes up 74% of the weight in the MSCI World Index, significantly above the long-term average of 57%.1

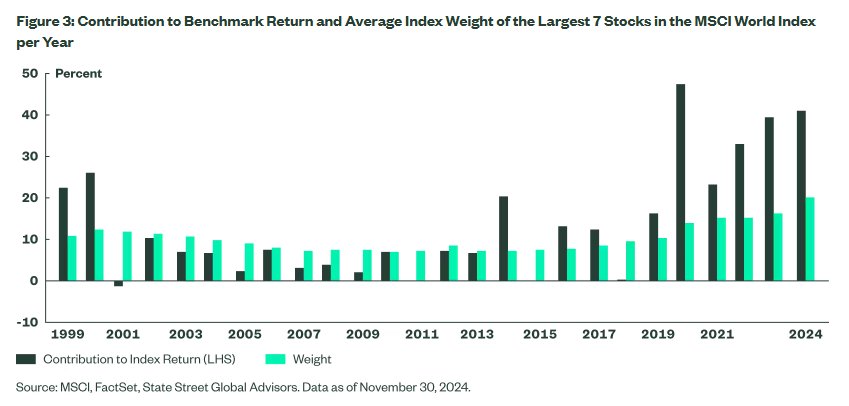

The current cohort of the world’s largest stocks, colloquially known as the Magnificent 7 is a significantly larger proportion of the market than its predecessors and over the past two years contributed 40% of the total index return. This return level is significantly above longer-term expectations and exceeds the returns from past top performing cohorts from past Technology, and Media and Telecommunications bubbles in the late 1990s and 2000s, respectively.

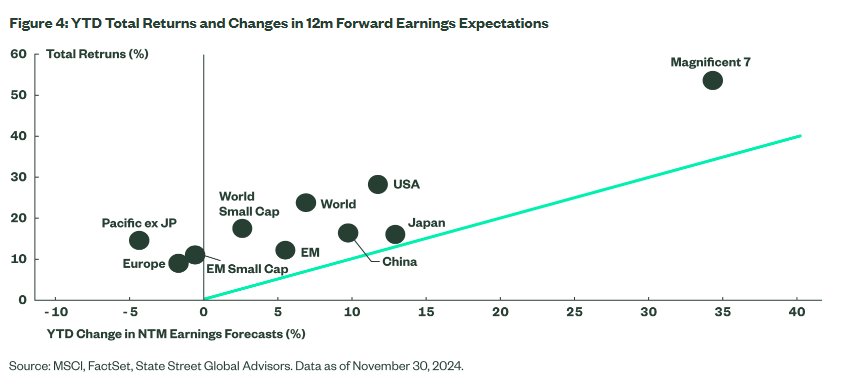

While this extreme positioning creates concentration risk for indexed investors, it does not necessarily represent irrational positioning in the markets. Over the past year there has been a strong correlation between returns and changes in earnings expectations, with stock prices following the direction of earnings. We show this trend in Figure 4, although we should note that as demonstrated by all the data points above the diagonal line, returns appear to be outpacing fundamentals— i.e., equity returns have been boosted by valuations getting more expensive.

As a result of the significant re-pricing across most equity markets, valuations now appear to be stretched even if not quite at extremes. Comparing current prices to earnings expectations over the next twelve months, the US market, for example, currently trades at 23x earnings, while Europe is around 13x earnings, and emerging markets small caps are at 14x. The standouts are the Magnificent 7 stocks, which on average trade at 40x earnings over the next twelve months.

The Bottom Line

Since the GFC, equity markets have generated robust returns, yet have become much more concentrated and more narrowly led. While fundamentals have largely driven this alpha generation, and in particular led by the exceptional performance of US stocks and the US economy, we think some re-assessing of the nature of the equity markets is worthwhile as we look forward to 2025. A healthy broadening out of market leadership, into previously unloved areas such as small caps or emerging markets, for example, could accompany a soft-landing scenario and be positive for market direction.

Given the very strong returns over recent years and stretched valuations particularly from the largest stocks, we would warn against extrapolating recent returns into the future. Returns for cap-weighted indices over the next decade may well be lower than those we have got used to. In a lower return world, incremental positive returns generated from active management could be more highly prized. We believe investors should start to reassess the balance of indexation with lower active risk (enhanced) approaches within the core of their portfolio along with fully active management in sectors where they believe they will be commensurably rewarded. Investors should prepare their portfolios accordingly as the next decade may be one of vigorous markets and healthy active management.

Originally posted on December 24, 2024 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/Creativa

VIA SHUTTERSTOCK

FOOTNOTES:

1 Average since December 31, 1998.

DISCLOSURES:

Marketing Communication

State Street Global Advisors Worldwide Entities

For use in EMEA: The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the appropriate EU regulator) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons, and persons of any other description (including retail clients) should not rely on this communication.

Important Risk Information

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

All information is from State Street Global Advisors unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Investing involves risk including the risk of loss of principal.

The views expressed are the views of Systematic Equity – Active through December 10, 2024, and are subject to change based on market and other conditions.

Quantitative investing assumes that future performance of a security relative to other securities may be predicted based on historical economic and financial factors, however, any errors in a model used might not be detected until the fund has sustained a loss or reduced performance related to such errors.

Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions.

© 2024 State Street Corporation. All Rights Reserved.

{kind=link}