By: Steve Sosnick, Chief Strategist

Like a pilot advising his passengers to keep their seat belts buckled in case of potential air pockets, over the past two days we have referenced 1 why it seemed advisable to “buckle up” 2 for a potential pop in volatility. From the nearly 1% pop shortly after yesterday’s open to the lows of earlier this morning, we have seen a nearly 3.5% range in the S&P 500 over a roughly 25-hour period. That seems like a bit of turbulence, no?

The reasons for today’s gloom are fairly obvious – the imposition of tariffs at the stated deadline, for which many investors had been expecting a reprieve, and this morning’s woeful jobs report. But the trouble began a day earlier.

Yesterday we noted that major indices had given back most of their pre-market gains by mid-morning, but things got notably worse by mid-afternoon. We had actually completed what technical analysts call an “outside reversal”, or “key reversal”. This occurs when the intraday range on a given day exceeds that of the prior day. It is considered most meaningful if the close is above the prior day’s high or below its low. Yesterday’s move nearly achieved that pattern, but the close was just above Wednesday’s low. (I realize that many investors have no love for technical analysis, but when enough folks believe in an indicator it can be self-fulfilling in the short-term.)

In the US, most of us awoke to see futures sharply lower. There was a sort of “this stuff got real” aspect to the news flow regarding tariffs. Indeed, while there is still the chance for some reprieves in the seven days until their full implementation (and perhaps in the courts 3), there appeared to be a broader concern that tariffs against nearly all countries would be here to stay. Global markets echoed those concerns, meaning that stocks were already on precarious footing even before this morning’s employment report.

That report turned out to be a stunner! It wasn’t necessarily horrible on the surface. Nonfarm Payrolls for July rose by 74,000, which was below the consensus 104k. That’s a miss, but not a huge one. The Unemployment Rate rose by 0.1% to an as expected 4.2%. Average Hourly Earnings rose by an as expected 0.3% and the Labor Force Participation Rate ticked down slightly to 62.2%. OK, then…

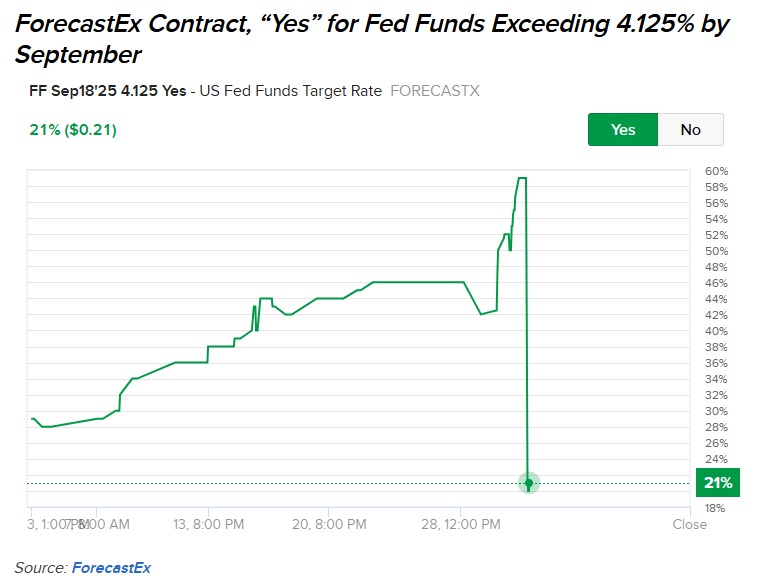

But the revisions were stunning! June Nonfarm Payrolls were revised down to 14K from 147k. Yes, that’s 1/10 the prior increase. Furthermore, the two-month revision was a staggering -258k. That means, with the June number revised down by 133k, the May revision was -125k and that only 19k jobs were created that month. Quite frankly, that is horrible, and markets reacted accordingly. I’ll refrain from speculation, but one has to wonder how the Bureau of Labor Statistics got it so wrong. As I type this, 2-year Treasury yields are 23 basis points lower, at 3.72%, and 10-year yields are about 14 bp lower at 4.24%. Those figures imply that rate cut expectations changed dramatically – which indeed was the case. Fed Funds futures 4 are now pricing in a roughly 85% chance for a cut in September. That is up from about 40% yesterday! They also implied a 31% chance for a second cut by December. That is now the probability for a third cut by December! The chart below shows the plunge in ForecastEx’ “Yes” market 5 for a rate above 4.125% by September:

The thrust of yesterday’s piece was about Chair Powell’s contention that rates were not, in fact, too restrictive. Based upon the available data, that was a defensible position, and one that I frankly agreed with. John Maynard Keynes is quoted as saying 6, “When the facts change, I change my mind. What do you do, sir?” Boy, did the facts change and so have many of the market’s assumptions about risk and the economic backdrop. That applies to my thinking and must apply to Powell’s. It certainly seems to apply to a wide range of investors. We have witnessed a notable flight to safety with money flowing into bonds and VIX and away from stocks and crypto.

Regarding VIX, we have opined:

VIX is the price of parachutes when a plane hits turbulence.

We explained:

This comes from my experience as a market maker. Nobody really wants umbrellas when it’s when there’s a drought, nobody really thinks about a parachute if the plane is moving along smoothly at 30,000 feet, but as soon as you hit some turbulence, or as soon as the rain clouds develop, people want them, and they want them in a hurry. And to me, VIX is still the most efficient way for an institutional manager to hedge his or her risks.

At 20, VIX is hardly displaying panic. Nor should it. But remember that it was below 15 yesterday morning. Better to keep one’s seat belt loosely fastened when the plane is cruising than when it hits an air pocket.

Originally posted on August 1, 2025 on Traders’ Insight

PHOTO CREDIT: https://www.shutterstock.com/g/Sorapop

VIA SHUTTERSTOCK

FOOTNOTES AND SOURCES:

1https://www.interactivebrokers.com/campus/traders-insight/securities/options/fomc-msft-meta-anything-to-see-here/

2https://www.cnbc.com/video/2025/07/29/steve-sosnick-buckle-up-if-markets-dont-get-best-case-scenario-on-trade.html?&qsearchterm=sosnick

3https://www.msn.com/en-us/news/us/us-appeals-court-scrutinizes-trumps-use-of-tariffs-as-trade-deadline-looms

4https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

5https://forecasttrader.interactivebrokers.com/eventtrader/#/market-details?id=658663572%7C20250917%7C4.125&detail=contract_details

6https://www.economicshelp.org/blog/613/economics/quotes-by-john-maynard-keynes/

DISCLOSURES

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: ForecastEx

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx forecast contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

Disclosure: Forecast Contracts

Forecast Contracts are only available to eligible clients of Interactive Brokers LLC, Interactive Brokers Canada Inc., Interactive Brokers Hong Kong Limited, Interactive Brokers Ireland Limited and Interactive Brokers Singapore Pte. Ltd.

Disclosure: ForecastEx Market Sentiment

Displayed outcome information is based on current market sentiment from ForecastEx LLC, an affiliate of IB LLC. Current market sentiment for contracts may be viewed at ForecastEx at https://forecasttrader.interactivebrokers.com/en/home.php. Note: Real-time market sentiment updates are only active during exchange open trading hours. Updates to current market sentiment for overnight activity will be reflected at the open on the next trading day. This information is not intended by IBKR as an opinion or likelihood of a potential outcome.

Disclosure: Forecast Contracts Risk

Futures, event contracts and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy visit our Warnings and Disclosures Page.

Disclosure: CFTC Regulation 1.71

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.