By:

Saketh Reddy, CFA, Research Analyst, Investment Strategy and Research

Dane Smith, Head North American Investment Strategy and Research

The US utilities sector is set for its biggest growth in decades, powered by rapid AI adoption and electrification. Explosive data center demand is driving earnings, valuations, and capital deployment.

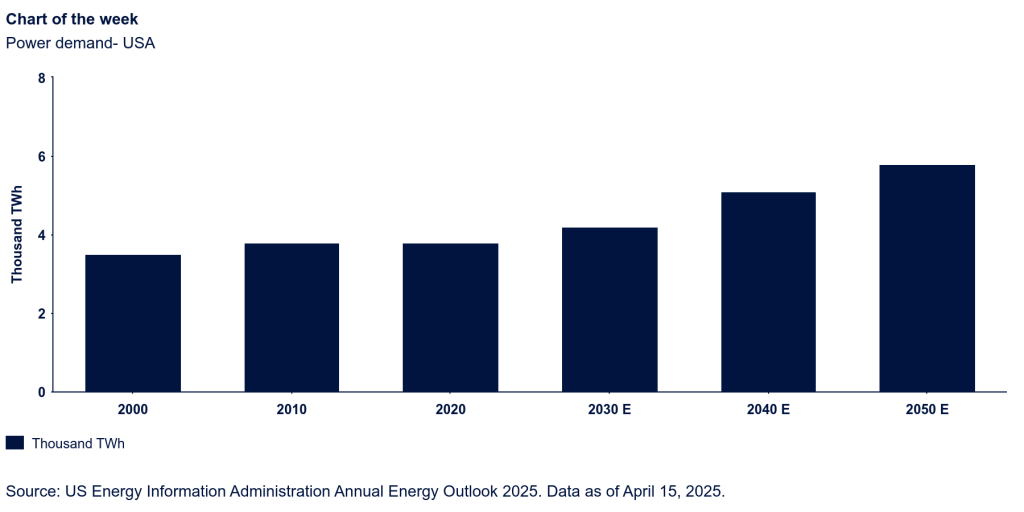

US electricity demand was essentially flat from the mid-2000s to early 2020s. Growth from population and economic activity was offset by efficiency improvements and a shift from manufacturing to service sectors, which consume less energy. Now, demand is accelerating, driven by electrification, industrial reshoring, and rapid data center expansion. Electricity demand is expected to rise by more than 50% from 2020 levels to 2050, driven largely by commercial and industrial sectors—especially data centers.

Powering the AI economy: Utilities enter their biggest growth cycle in decades

The US utilities sector is entering a transformative phase, fueled by structural demand shifts from electrification and the rapid adoption of AI. US power demand is set to accelerate meaningfully in the years ahead. A key driver of this shift is the explosive rise of data centers—powered by AI workloads and hyperscaler capital spending-which are emerging as a major growth engine. Their share of total electricity consumption could nearly triple by 2028, rising from 4.4% in 2023 to an estimated 6.7%–12%1. Meeting this surge may require over 50 GW of incremental capacity by 20282. This unprecedented demand acceleration positions utilities for a significant growth opportunity, with far-reaching implications for earnings, valuations, and capital deployment strategies.

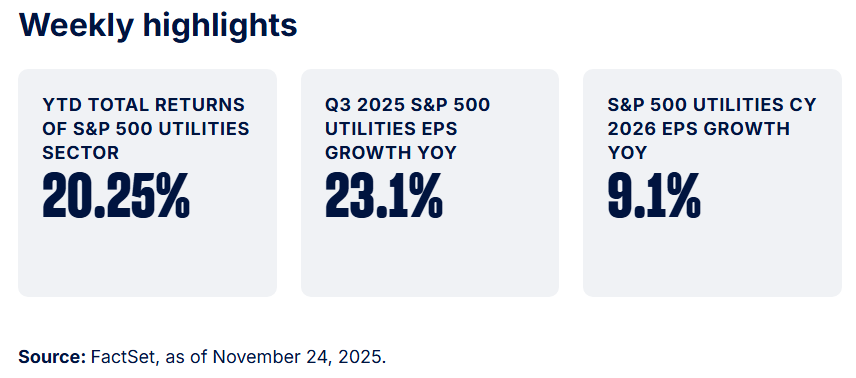

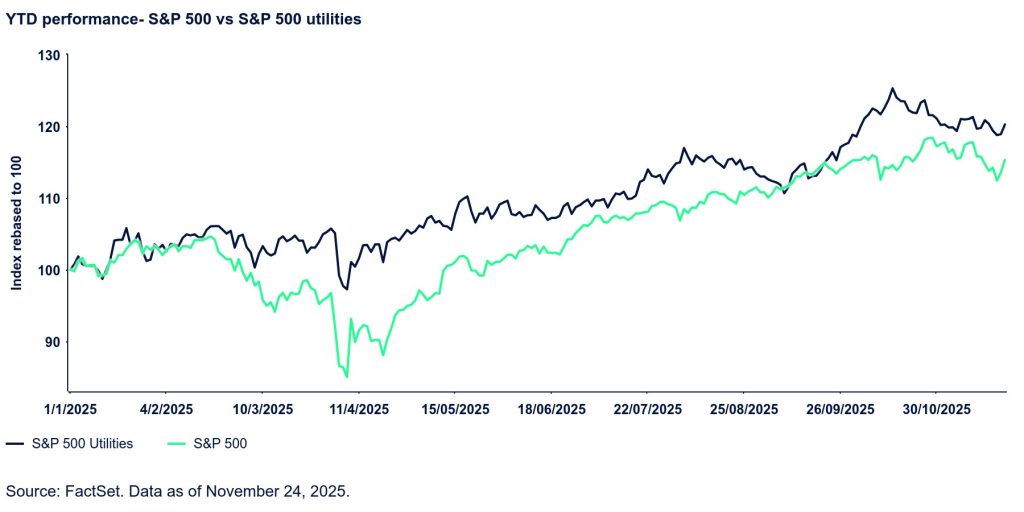

After ending 2023 as the weakest S&P 500 sector with a 15% decline in earnings, utilities staged a sharp rebound in 2024, delivering a 23.4% return driven by robust earnings growth of 24.7%. The sector has maintained strong momentum into 2025, posting year-to-date gains of 20.25% and outperforming the broader index by 493bps3. Q3 2025 results were particularly strong: Utilities reported the third-highest year-over-year earnings growth among all eleven sectors at 23.1%, with 74% of companies beating estimates. At the industry level, all five subsectors posted positive earnings growth: Independent Power and Renewable Electricity Producers (+32%), Gas Utilities (+29%), Electric Utilities (+25%), Multi-Utilities (+17%), and Water Utilities (+8%)4. The sector’s low beta and defensive characteristics have proven attractive amid heightened volatility and macro uncertainty, while expectations of rate cuts have further supported the rally.

At the start of 2024, utilities traded at a forward P/E of 15.8, about a 19% discount to the S&P 500, but as investors recognized growth potential tied to AI-driven energy demand, valuations climbed, with current forward P/E ratios near 18.5x-above the historical 15x average5 yet still below the market’s 21.7x. This multiple expansion reflects optimism around the AI CapEx boom, though earnings have lagged due to the sector’s typical delay between capital deployment and revenue realization. This optimism is underpinned by hyperscaler-driven demand, which has set the stage for an unprecedented investment cycle: utilities plan $208 billion in grid upgrades for 2025 and more than $1 trillion through 2029, aimed at expanding generation, transmission, and storage capacity to meet surging power needs.

Historically, lower yields have supported the utility sector by reducing capital-raising costs. With rate-cut expectations gaining traction, falling yields further enhance the sector’s defensive appeal. Utilities currently offer a dividend yield of 2.68%6, alongside consensus EPS growth estimates of 7.2%, 9.1%, and 9.2% for CY25-277. This positions utilities as a rare combination of income stability and secular growth. Structural tailwinds from AI adoption and electrification are transforming the sector from a traditional yield play into a growth-plus-income opportunity. While valuations have partially priced in the AI-driven demand story, earnings acceleration is expected to unfold over the next several years, creating potential for durable upside. Despite regulatory and execution risks, the long-term outlook suggests utilities could deliver superior risk-adjusted returns-making them a compelling choice for investors seeking defensiveness with upside.

Originally posted on December 1, 2025 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/TarikVision

VIA SHUTTERSTOCK

DISCLOSURES

Marketing Communication

ssga.com

State Street Global Advisors Worldwide Entities

State Street Global Advisors (SSGA) is now State Street Investment Management. Please go to statestreet.com/investment-management for more information.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the applicable regional regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator”) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

The views expressed in this material are the views of Saketh Reddy and Dane Smith through the period ended November 26, 2025 and are subject to change based on market and other conditions. and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Investing involves risk including the risk of loss of principal.

Investing involves risk including the risk of loss of principal.

Past performance is not a reliable indicator of future performance.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Currency Risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

Generally, among asset classes, stocks are more volatile than bonds or short-term instruments. Government bonds and corporate bonds generally have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. U.S. Treasury Bills maintain a stable value if held to maturity, but returns are generally only slightly above the inflation rate.

{kind=link}