By: Jose Torres, Senior Economist

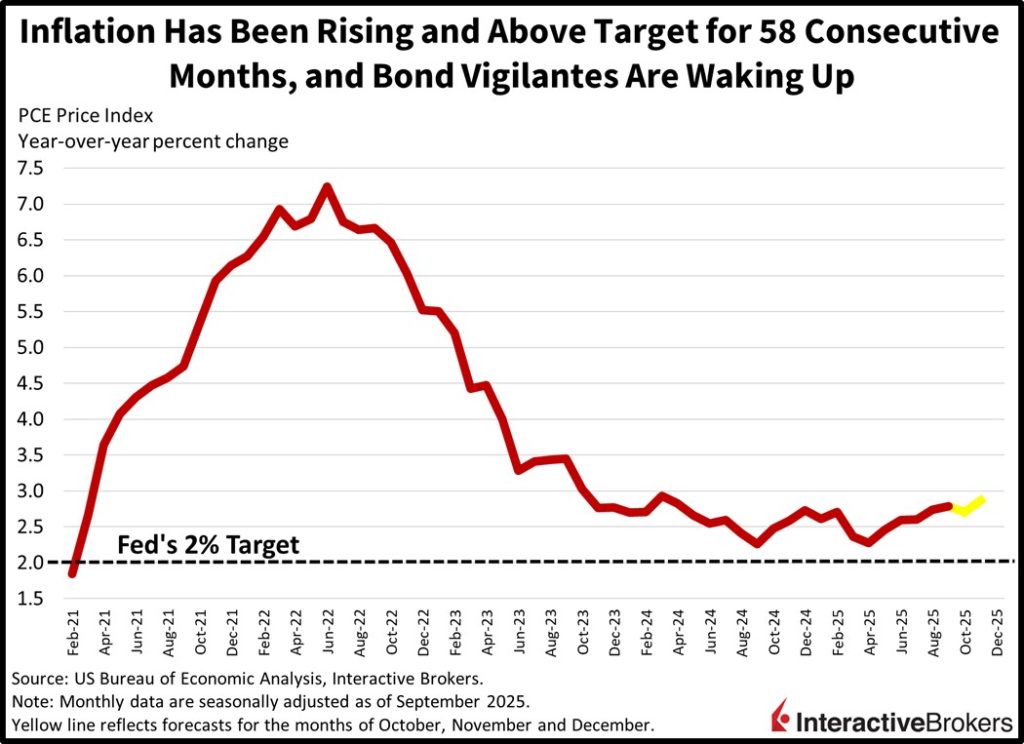

Stocks are getting pounded and risk-off sentiments are dominating Wall Street as a weaker-than-anticipated outlook from Broadcom coincides with the reawakening of the bond vigilantes. On the earnings front, a miss on the AI leader’s guidance comes on the heels of Oracle disappointing tech bulls. Worries are mounting that the significant investments committed to the modern technology’s infrastructure and the associated profitability may pale in comparison to the remarkable valuation expansion that has occurred among AI related companies. Meanwhile, fixed-income watchers are lifting long-term inflation expectations in response to a Fed is cutting against the backdrop of cost pressures running above target for 58 months when including this December, although official data is only available through September. Multiple central bank speakers, including Regional Presidents Hammack of Cleveland, Goolsbee of Chicago and Schmid of Kansas City, contributed to the violent bear-steepening occurring across the Treasury curve as well, with the 30-year yield rising to its highest level since September; it’s up a whopping 7 basis points. Participants tried to ignore the negative AI news and the heavier borrowing costs by piling into reacceleration trades near the open, as the Dow Jones reached a fresh record for its second consecutive day while the Russell 2000 hit an all-time high for the fourth session in a row, but those cyclically oriented indices are severely affected by the spiking price of duration and are currently suffering sharp losses. Investors are behaving defensively, raising exposures to names in healthcare and staples, volatility protection instruments, the greenback and forecast contracts. Conversely, a lack of speculative enthusiasm and a dip in cyclical activity forecasts as a result of climbing interest rates are punishing cryptocurrencies and commodities.

Nowhere to Hide

The last several sessions have featured waning AI enthusiasm being replaced by excitement about monetary policy accommodation prospects, backed by three consecutive cuts to end 2025, a dot plot pointing to another on the way and a Fed that is now expanding its balance sheet to support smooth functioning in the banking system. Folks have been incrementally rotating out of tech shares and into cyclically oriented, rate sensitive areas that are levered to an economic reacceleration, looser financial conditions and domestic activity. But today’s hawkish remarks from Fed governors combined with adverse news on the profitability and outlook front have left participants with nowhere to hide as markets experience broad-based losses across the indices, Treasuries, commodities and cryptocurrencies. With the US central bank nearing or at its neutral interest level against the backdrop of a long stretch going back to March 2021 of above-target inflation, bullish traders need earnings to come through for further upside in stocks. The last few days, however, have offered negative developments from technology companies, which alongside rising yields, leave investors without refuge.

International Roundup

China Pledges to Continue Economic Stimulus in 2026

China intends to continue providing stimulus in 2026, but it will be at a moderate, or measured, level, according to a statement from officials after yesterday’s Central Economics Work Conference yesterday. The country will continue deficit spending and will use interest rates and reserve requirements to help improve activity. Goals include stopping a steep decline in investment, improving housing market conditions and preventing a further decline in births.

China’s Loan Growth Disappoints

China’s chronic housing glut contributed to new loan growth slowing and missing expectations in November. Debt issuance growth weakened from 6.5% year over year (y/y) in the preceding month to 6.4% and was a record low, according to the People’s Bank of China. An economist consensus anticipated growth would match October’s pace. Reuters estimates that corporate loan issuance increased but mortgage volumes slipped.

UK GDP Posts Short-Term Contraction

Gross domestic product (GDP) slipped 0.1% in the UK during the three months ended in October compared with the reporting period ended in July, according to an estimate from the Office for National Statistics. Within the most recent headline number, services were flat after climbing 0.2% quarter over quarter (q/q) in the three-month period ended in September. Production output, furthermore, sank 0.5% with declines in manufacturing of motor vehicles, trailers and semi-trailers. Output descended at the same pace during the period concluded in September. Construction also disappointed, sinking 0.3% after being 0.1% higher q/q in the previous period.

More specifically, output sank in 7 of 14 sectors with the following categories and the extent of their changes being the most significant:

- Other service activities, down 2.6%

- Professional, scientific and technical activities, 1.6%

- Information and communication, 0.4%

On a y/y basis, however, GDP was up 1.1%. While production retreated 1.3%, services and construction were 1.5% and 1.1% higher, respectively.

Canada Wholesaling Was Nearly Flat in October

Total sales by Canadian wholesalers in October climbed 0.1% month over month (m/m), defying the economist consensus estimate for a 0.1% drop following September’s 0.6% ascent.

The metric, which excludes oilseed, grain and hydrocarbons, received the largest assist from the motor vehicle and motor vehicle parts and accessories subsector, up 2.3%, and the farm product category, up 16.7%.

But Capacity Utilization Climbed

Overall capacity utilization in Canada hit 78.5% in the three months ended in September compared to 77.6% in the second quarter. The metric, however, missed the economist consensus estimate of 79.3%. Construction utilization climbed 1.3 percentage points to 80.2% and mining, quarrying and oil and gas extraction ascended 0.7 points to 77.1%. Conversely, utilization headed south 1.7 percentage points to 78.8 in the electric power generation, transmission and distribution sector.

And Building Permits Defy Expectations

Building permits issued in Canada climbed 14.9% m/m during October, accelerating from 5.9% in September and defying the economist consensus expectation for a 1.4% descent.

Originally posted on December 12, 2025 on Traders’ Insight blog

PHOTO CREDIT: https://www.shutterstock.com/g/78image

VIA SHUTTERSTOCK

DISCLOSURES

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.