By:

Simona M. Mocuta, Chief Economist

Amy Le, CFA, Investment Strategist

Venkata Vamsea Krishna Bhimavarapu, Economist

The ECB and BoJ held rates, signaling caution. UK retail sales rebounded slightly, but consumer sentiment and global growth indicators remain mixed, keeping markets on edge.

ECB in hawkish hold

As widely expected, the ECB Governing Council left all interest rates unchanged at the July 24 meeting. There was little new in the accompanying statement and on the surface at least, the key message is simply that the ECB is “not pre-committing any particular rate path.” Still, the totality of the messaging—especially the press conference—was hawkish.

President Lagarde highlighted the resilience of the economy in the first quarter and noted that this was not entirely the result of export frontloading, but also due to investment and consumption. Moreover, the robust labor market and strong household balance sheets support consumer spending. Easier financing conditions and fiscal expansion (defense and infrastructure spending) are also supporting growth. In other words, the economy does not appear to require additional policy support. This has been our view for some time, so we evidently concur with the assessment. The inflation picture suggests the same, with inflation not only currently at target but expected to be stable at 2.0% over the medium term. On that point, President Lagarde, during the press conference, minimized concerns about the anticipated inflation undershooting in 2026, given its temporary nature. Given that the primary argument for additional cuts is precisely this expected undershooting, this suggests that the ECB is not only briefly on hold, but on an extended hold at least.

UK: Retail sales recovered but in limited fashion

Following a 2.8% MoM decline in May, retail sales volumes (excluding auto fuel) increased by 0.9% in June, falling short of the consensus forecast of 1.2%. The housing market continued to be affected by changes to stamp duty, contributing to a further 0.1% MoM decrease in household goods retailer sales for the second consecutive month. Food sales rose by 0.7% MoM; however, this uptick did not offset the previous month’s 5.4% decline, and some of June’s improvements may be attributable to temporary factors such as warm weather influencing beverage purchases. Consequently, retail sales grew modestly by 0.2% QoQ in Q2.

Meanwhile, consumer sentiment remained subdued. The GfK measure of consumer confidence declined from -18 in June to -19 in July. Going forward, slower wage growth, fiscal consolidation, and the delayed effects of prior interest rate increases will continue to present challenges for the sector.

BoJ: Baby steps toward the next hike

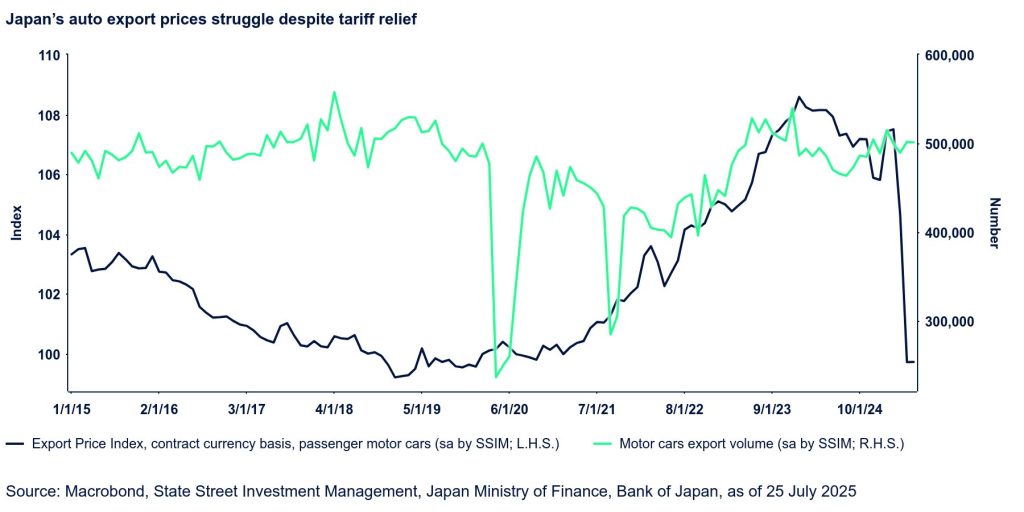

President Trump announced a trade deal with Japan in a surprise move that lowered the baseline tariff rate to 15% (from 26%), which is crucially also matched by lower auto tariffs (25%). In exchange, Japan will improve market access for US companies, including in autos and agricultural products such as rice. Japan also agreed to import more rice from the US, but the overall tariff-free quota remains at 770,000, so we expect fewer imports from other countries. Most importantly, Japan committed to a $550 billion investment in the US. Steel and aluminum exports will still be tariffed at 50%.

The deal is undoubtedly positive for the outlook, but we still maintain our growth forecasts at 0.4% in 2025 and 0.6% in 2026, as despite lower tariffs, the overall tariff level is significantly higher than a year ago.

For our forecasts to change, we need to see a pickup in auto export prices, which have collapsed since Liberation Day. It is likely that these export prices on a contractual basis may recover, but we are not convinced of a full rebound in light of the still-high tariff rate. Overall volumes remained stable, making it more critical that these prices recover. This is essential for the medium-term outlook because next year’s shunto wage negotiations depend on the profitability of the auto firms.

Tokyo CPI remained firm in July, although the core metric (excluding fresh food) was down two-tenths to 2.9% YoY. The global core metric (excluding fresh food and energy) declined only a tenth to 1.7%. Most importantly, price pressures are firming up in other food categories—as despite a decline in rice prices, the momentum remained strong in other food items at 0.4% MoM, or 6.9% YoY.

Nonetheless, the Bank of Japan (BoJ) next week is likely to reiterate that there is still ‘some distance’ in underlying inflation from their target. We do not expect the Bank to make any policy changes, but markets will remember the Bank’s surprise last August when it raised the policy rate to 0.25% while halving bond purchases. If the BoJ lifts its inflation forecasts, it can be seen as a stronger message that they are keeping rate hike possibilities open in H2 2025.

Originally posted on July 28, 2025 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/judyjump

VIA SHUTTERSTOCK

DISCLOSURES

Marketing Communication

State Street Global Advisors (SSGA) is now State Street Investment Management. Please go to statestreet.com/investment-management for more information.

State Street Global Advisors Worldwide Entities

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the applicable regional regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator”) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

The views expressed in this material are the views of SSGA Economics Team through the period ended 25 July 2025 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

© 2025 State Street Corporation. All Rights Reserved.