By:

Chris Carpentier, CFA, FRM, Senior Investment Strategist

Samuel Rudin

Despite rising geopolitical risks, tariff threats, and shifting rate expectations, global markets remain resilient—buoyed by strong fundamentals, easing inflation, and tactical policy pivots across major economies.

What’s striking about this chart isn’t how the lines are reacting—but how they aren’t. Historically, as a safe haven, the US dollar strengthens during volatility spikes. Yet in April, during the initial tariff announcements, that relationship broke down. Instead of rallying, the dollar softened—suggesting a shift in market dynamics worth watching. In addition, the weakening dollar has given a boost to international allocations in local terms.

Geopolitical Volatility and Market Resilience

The past week has been marked by a flurry of geopolitical developments, underscoring the persistent uncertainty that continues to shape the global investment landscape. From sweeping tariff threats to enhanced military alliances, the headlines have been anything but quiet. Yet, amid the noise, markets have shown surprising resilience.

One of the most significant developments is the US Senate’s move to empower President Trump with the authority to impose up to 500% tariffs on any country aiding Russia, including major economies like Brazil, China, and India. This comes alongside discussions to utilize interest from Russia’s seized assets (valued at approximately $300 billion) to support Ukraine’s defense.

In a notable pivot, Trump has announced plans to send Patriot missile systems to Ukraine. While he has criticized the Biden administration’s approach of donating military aid, Trump’s strategy leans toward selling equipment—a move that has garnered support from European partners. NATO, however, is not expected to contribute financially to these arms purchases.

On the trade front, tensions between the US and the EU are escalating. Brussels is preparing retaliatory tariffs on €72 billion worth of US goods in response to Trump’s proposed tariff hike from 10% to 30%. French President Emmanuel Macron is pushing for immediate countermeasures targeting €21 billion in U.S. exports, including soybeans, motorcycles, and orange juice. The EU has already downgraded its 2025 growth forecast from 1.3% to 0.9%, citing the potential economic drag from these tariffs. While Southern European economies may be less exposed due to limited US trade ties, the broader EU outlook remains fragile. Corporate earnings expectations across Europe remain mixed, as reflected in the wide range of 2025 earnings growth forecasts among major markets in the MSCI Europe Index—ranging from a slight decline in the UK (-0.4%) to moderate growth in France (5.2%) and strong gains in Germany (16.8%).

Adding to the complexity, Trump has warned that any EU retaliation will be met with additional tariffs—effectively stacking penalties. Mexico is also in the crosshairs, with Trump citing insufficient action on border security as justification for new tariffs. Further, President Trump has signaled that new tariffs on pharmaceutical imports could take effect by the end of the month, with semiconductors also under consideration for future trade measures.

Offsetting Forces and Market Surprises

Despite this geopolitical turbulence, there are notable counterbalances. Domestically, the recently passed “One Big Beautiful Bill” is expected to provide fiscal support that could cushion the impact of tariffs. Internationally, his willingness to provide military equipment to Europe while also allowing Nvidia to resume chip sales to China may help stabilize key relationships.

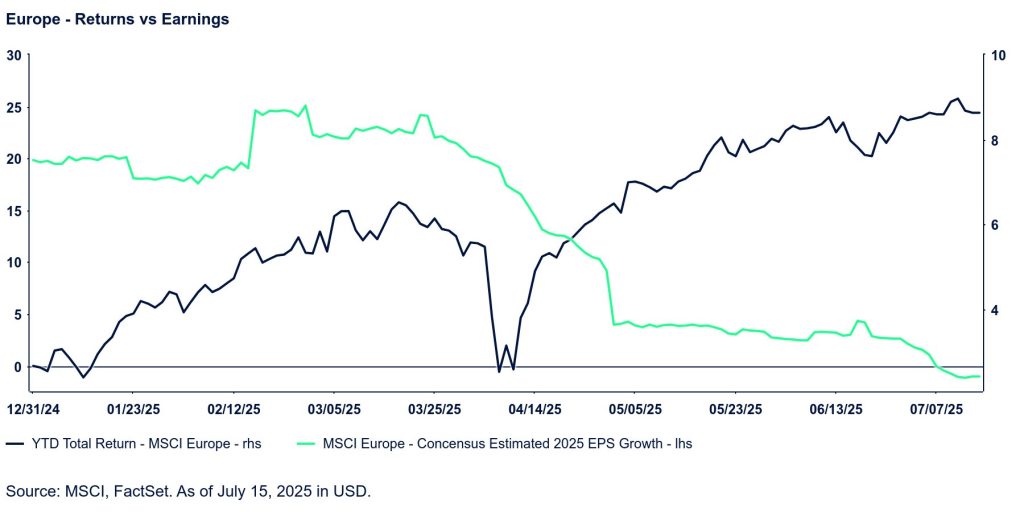

Perhaps one of the more surprising developments has been Europe’s market performance. Year-to-date returns are approaching 25% for MSCI Europe in USD terms, driven in part by a weakening dollar along with expectations of increased defense and infrastructure spending. Even when adjusting for currency effects, European equities are still up 11% YTD.

However, this optimism is tempered by a sharp decline in earnings expectations. Forecasts for 2025 earnings growth have dropped from 9% earlier this year to just 2.5% today. This suggests that while markets are pricing in future fiscal expansion, the actual impact on corporate earnings may be delayed.

Much of today’s geopolitical tension is centered around the US One of the clearest signs of dislocation has been the US dollar, which has diverged from historical patterns. As global uncertainties continue, we’ll see whether markets are right to remain relatively calm through the recent noise.

Originally posted on July 18, 2025 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/Aun+Puttipong

VIA SHUTTERSTOCK

DISCLOSURES

ssga.com

State Street Global Advisors Worldwide Entities

State Street Global Advisors (SSGA) is now State Street Investment Management. Please go to statestreet.com/investment-management for more information.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the applicable regional regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator”) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

The views expressed in this material are the views of Dane Smith, Kyle Murray and Christopher Carpentier through the period ended July 17, 2025 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Investing involves risk including the risk of loss of principal.

Investing involves risk including the risk of loss of principal.

Past performance is not a reliable indicator of future performance.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Currency Risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

Generally, among asset classes, stocks are more volatile than bonds or short-term instruments. Government bonds and corporate bonds generally have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. U.S. Treasury Bills maintain a stable value if held to maturity, but returns are generally only slightly above the inflation rate.

© 2025 State Street Corporation – All Rights Reserved.

{kind=link}