By: Mayuranki De, GlobalX

Consumers may be going offline and back into stores to shop, but when they do, they want to go digital to pay. Smartphone payments and tap to pay options continue to gain acceptance, leading the transition away from cash and card swipes as merchants rapidly install modular point-of-sale (POS) systems. Macro pressures took some of the air out of fintech overall in 2022, including the emerging online lending and buy now, pay segments. However, it’s important to remember that the pandemic pulled forward growth for many fintech companies. With nearly 1.4 billion people worldwide above the age of 15 still without bank accounts, fintech has a critical role to play in expanding access to financial services.1

Even amid challenging economic conditions, we believe the Fintech mega theme can deliver growth and gain transformative ground, particularly at the point of sale.

Key Takeaways

- Shoppers increasingly prefer their in-store time to be as limited and efficient as possible, and POS systems have emerged as a sophisticated and cost-effective solution to meet this demand.

- Rising payment volumes for first movers and industry leaders including Square, Toast, and Clover have Big Tech entering the space.

- As major players like Apple adopt POS features, traditional fintech companies are adapting through collaboration and new business verticals.

Consumers’ Pandemic Shopping Habits Are Here to Stay, Forcing Innovation

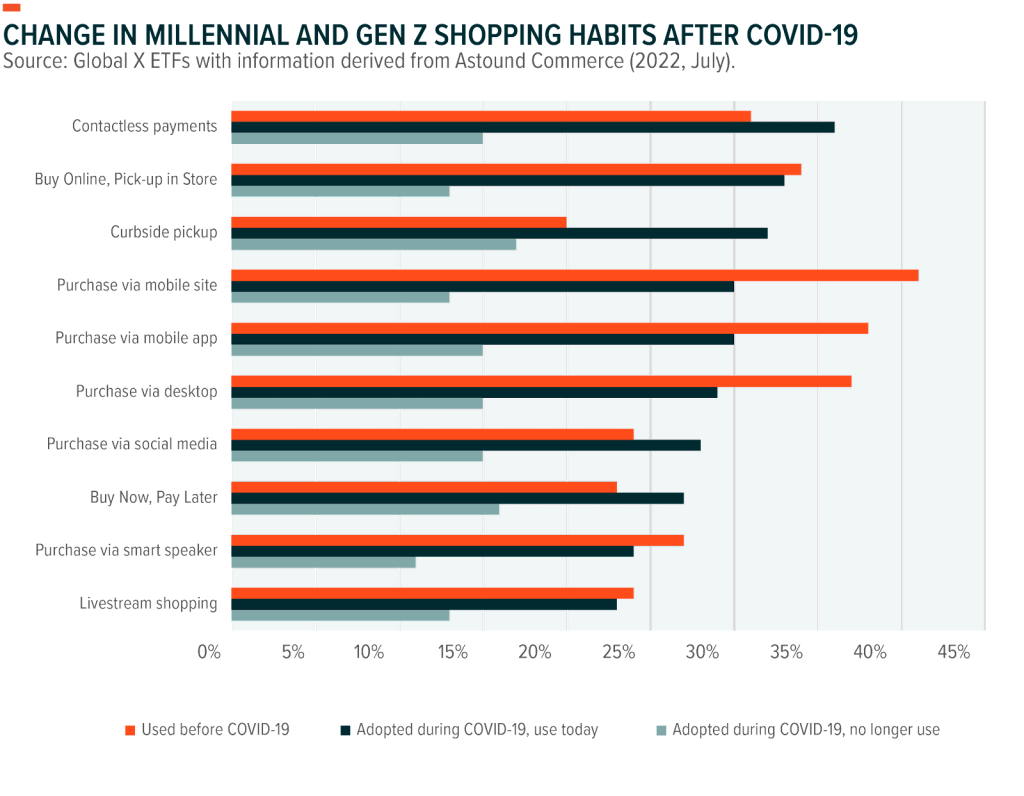

The way in which the average shopper needed to acquire products and services shifted drastically during the pandemic. COVID-19 gave rise to consumer expectations for cashless payment methods, which led to a surge in the use of mobile wallets and contactless payments at the point of sale.

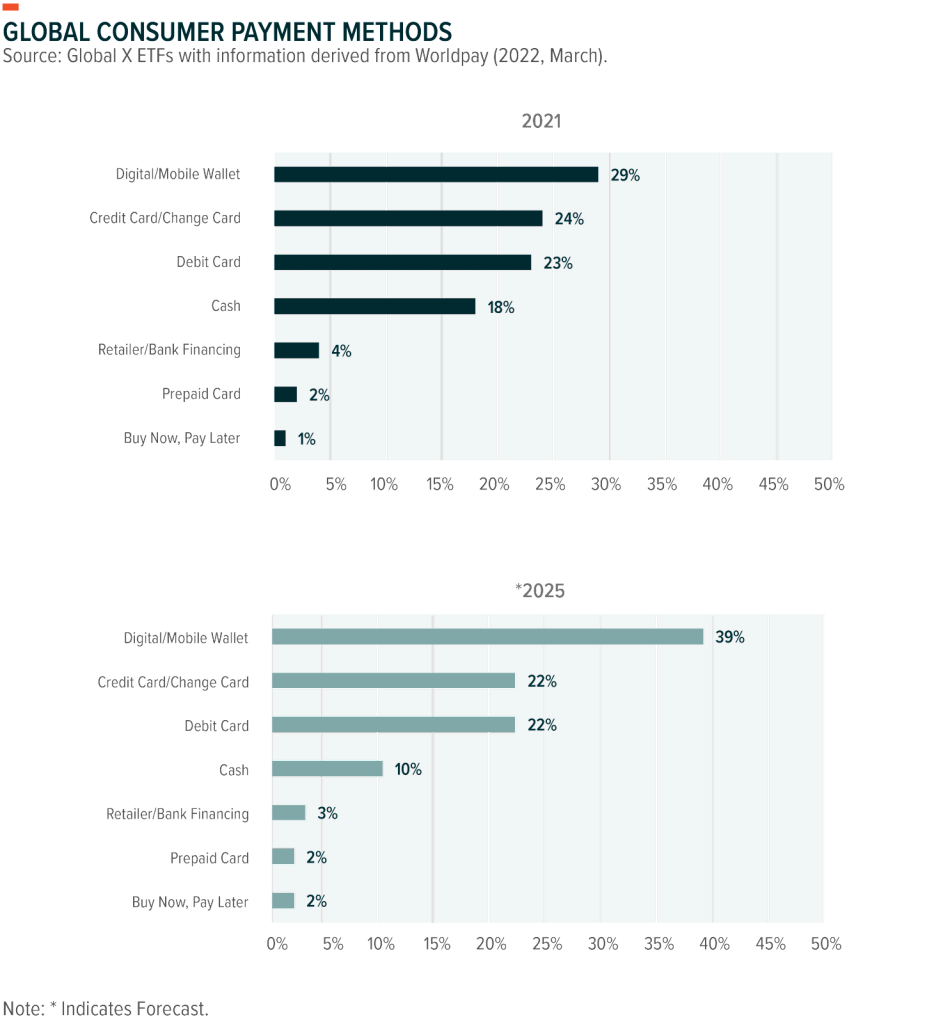

In 2021, payment by mobile wallet was the most widely used POS method globally, accounting for 29% of the market share, up from less than 26% in 2020.2,3 By 2025, mobile wallets are projected to account for nearly 40% of all POS transactions worldwide.4 Despite progress in mature economies like the United States, cash still accounts for 11% of the market for payment methods at the point of sale, indicating meaningful growth potential.5 In emerging markets, where the penetration for digital payments is much higher due opportunities for financial inclusion and favorable demographics, China leads the market for POS payments at 54% of consumers, followed by India at 25%.6

Shoppers increasingly prefer their in-store time to be as limited and efficient as possible. Deemphasizing cash is a step towards this type of shift, but efficient POS processing is equally important. In a recent Visa survey, 41% of consumers surveyed in nine markets around the world said that they had abandoned their shopping carts in a physical store because it didn’t have digital payment options.7 Global POS transaction values are projected to approach $58.9 trillion by 2025.8 Adjacent to this rapid digitization of the global economy is the decline in physical cash payments, which are expected to dip from 18% in 2021 to 9.8% of the total share by 2025.9

As a result of these evolving consumer habits and systemic shifts, today’s POS systems are much more sophisticated than they were a decade ago. Small businesses demanded more solutions from POS vendors to serve omnichannel operations, and platforms obliged, now selling services such as inventory management, back-office software, time management tools, and internal accounting. Businesses also evolved to access, analyze, and control customer information generated at the point-of-sale, through a singular interface. In the past few years, this started to allow retailers to power loyalty programs, offer promotions, and strengthen effective social marketing.

Fintech’s Success Encourages Big Tech to Seize an Opportunity

Disruptive fintech platforms achieved great success in helping the local vendor digitize. Square, the pioneer of the smartphone-based POS system, processed $180 billion on an annualized basis through Q3 2022 following the strong resurgence of the offline consumer.10 Toast, which sells modular POS solutions to restaurants, reported top-line growth of 55% and payment volume growth of 53% for the same period.10 Legacy payment processors such as Fiserv and Fidelity National also reported strong growth, particularly for their modular solutions. Fiserv, which owns Clover, reported that its gross payment volumes (GPV) grew to $236 billion in the 12 months through Q3 2022.12 This is compared to $196 billion over the same period a year ago.13

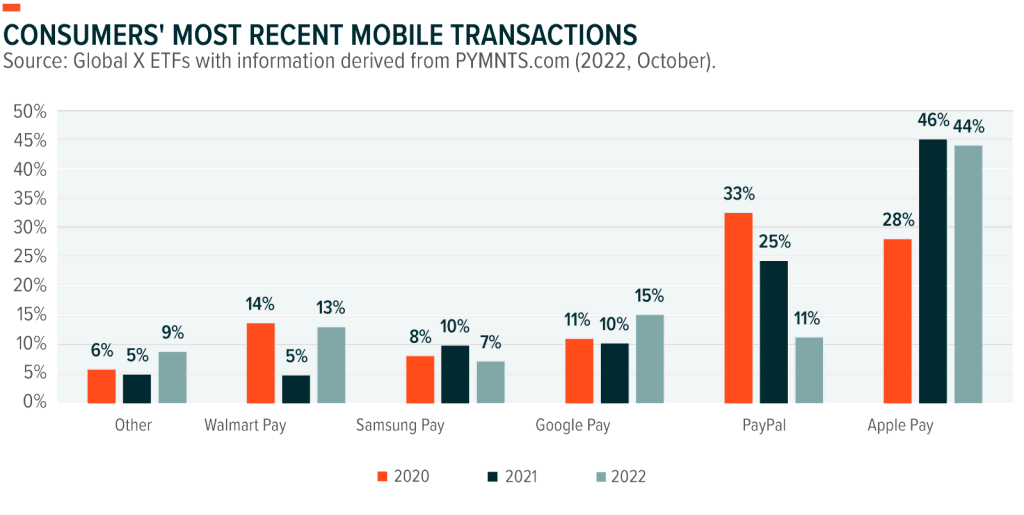

The success of disruptors like Square, Toast, Clover, and technology-first companies in digital wallet and POS system spaces did not go unnoticed by the biggest tech companies. Apple Pay leads in mobile payment platforms, capturing nearly 44% of in-store mobile wallet transactions as of Q3 2022.14 On a relative basis, Apple Card holders numbered 6.4 million in the U.S. as of May 2021—70% of whom are in their 20s and 30s.15

New product launches outline big tech’s vision. For example, in June 2022, Apple announced its impending buy now, pay later service known as Apple Pay Later. The feature seamlessly integrates into the preinstalled Wallet app, and when available, it will appear as another option on the Apple Pay payment screen. Additionally, Apple Pay Later works with any credit or debit card that Apple Pay supports.

The pandemic helped digital channels such as POS systems quickly gain traction among younger, tech-savvy generations in developed countries. Digital wallet adoption by these demographics shows clear growth in recent years. Sixty-five percent of young millennials used a digital wallet in 2021, compared to 59% in 2020. For Gen Z, digital wallet use rose to 57% in 2021 from 50% a year earlier.16 With combined spending power of nearly $350 billion in the U.S., these consumers are an ever-powerful target for businesses, and the investments here are also acting as a hedge against demographic shifts.17

Tap to Pay, Fintech’s Next Big Thing?

One of the key implications of POS systems upgrades is the boost that they have offered to contactless payments, further boosting growth of fintech offerings by big tech companies. Tap to pay volumes continue to rise in the United States. For 2022, U.S. tap to pay spending per user is expected to grow 30% year-over-year (YoY) to $4,177.18 Big tech and fintech giants are jumping to make the most of the opportunity.

In February 2022, Apple unveiled its Tap to Pay feature, which allows users to pay someone by simply tapping their iPhone against theirs. With Apple Pay accepted at more than 90% of U.S. retailers already, merchants of all sizes are expected to gravitate towards Tap to Pay.19 For small businesses, Apple’s Tap to Pay can be particularly beneficial because merchants can accept contactless payments without the need for additional hardware, making it a cheaper option. Google is another tech giant that entered the tap to pay space. In 2022, the company launched Google Wallet to pair it with Google Pay. Google Wallet’s features a near-field communication (NFC) card interface, emphasizing POS emergence.

The vast reach of companies like Google and Apple, which serve billions of consumers globally, could boost the adoption of digital payments globally for merchant processing. With a smartphone, merchants do not have to invest in a POS machine. The implications of low-cost mobile processing gaining momentum in underbanked emerging markets such as Africa, Asia, and Latin America can be transformative, in our view.

By 2027, 99% of smartphones will be capable of making contactless payments, and U.S. contactless payments are forecast to nearly double to 8.3 billion transactions.20 This growth translates into a promising outlook for fintech companies playing in this arena, especially those that closely collaborate with big tech players.

For example, Square Seller Services and Cash App are established partners with Apple Pay. Even PayPal implements Apple Pay into its back-end payments platform, Braintree. These partnerships also help accelerate the transition of modern POS vendors away from selling hardware to small merchants, allowing them to focus on monetization through services and subscriptions where they earn a bulk of gross profits.

POS payments are forecast to grow at a consistent 6% compound annual growth rate (CAGR) globally through 2025, with the strongest growth in Latin America at 8% and Asia-Pacific at 7%.21 However, we believe actual growth could result in easily surpassing these projections.

Conclusion: Digital Payments a New Standard

Modular POS solutions are gaining ground rapidly as small and medium enterprises (SMEs) digitize to meet new consumer preferences, especially those of younger generations. The increasing use of digital payments in the United States is driving demand for tap to pay options and providing cost-effective options for merchants to digitize. Additionally, fintech companies are expanding their offerings to include features such as lending, accounting, and back-office operations. Despite current economic conditions limiting growth in 2022, we expect widespread adoption of these fintech solutions over the long term as the consumer goes even more digital – positioning these companies for upside surprises.

FOOTNOTES

1. World Bank. (2021. Accessed 2023, February 3). The Global Findex Database 2021: Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19.

2. Worldpay from FIS. (2022. Accessed 2023, February 3). The Global Payments Report 2022.

3. Worldpay from FIS. (2021. Accessed 2023, February 3). The Global Payments Report 2021.

4. Worldpay from FIS. (2022. Accessed 2023, February 3). The Global Payments Report 2022.

5. Ibid.

6. Ibid.

7. Visa. (2021, December. Accessed 2023, February 3). Visa Back to Business Global Study.

8. Worldpay from FIS. (2022. Accessed 2023, February 3). The Global Payments Report 2022.

9. Ibid.

10. Block. (2022, November 2). Q3 2022 Block Shareholder Letter.

11. Toast. (2022, November 10). Third Quarter 2022 Financial Results [Investor Presentation].

12. Fiserv. (2022, October 27). Third Quarter 2022 Financial Results [Investor Presentation].

13. Fiserv. (2021, October 27). Third Quarter 2022 Financial Results [Investor Presentation].

14. PYMNTS. (2022, October 25). Apple Pay Leads Among Wallets but Lags in Total Purchases.

15. Forbes. (2021, May 4). Apple Card Grows To 6.4 Million Cardholders Thanks To Women.

16. Global Payments. (2022, January 31). How Millennials and Gen Z are shaping the future of payments.

17. Ibid.

18. Insider Intelligence. (2022, May 27). US Proximity Mobile Payments 2022: How Providers Can Use Pandemic Growth as a Springboard to Future Engagement.

19. Apple. (2022, February 8). Apple empowers businesses to accept contactless payments through Tap to Pay on iPhone.

20. NFCW. (2022, September 12). Contactless payments set to hit US$10tn globally by 2027.

21. Worldpay from FIS. (2022. Accessed 2023, February 3). The Global Payments Report 2022.

Originally Posted February 10th, 2022, GlobalX

PHOTO CREDIT:https://www.shutterstock.com/g/BlackSalmon

Via SHUTTERSTOCK

Disclosure

Investing involves risk, including the possible loss of principal. Diversification does not ensure a profit nor guarantee against a loss.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information is not intended to be individual or personalized investment or tax advice and should not be used for trading purposes. Please consult a financial advisor or tax professional for more information regarding your investment and/or tax situation.

{kind=link}