Greed is back in fashion.

Despite high equity valuations and weakening earnings, the stock market bounds from strength to strength.

On February 13, the S&P 500 Index (SPX) set a new all-time record and the Dow Jones Industrial Average (INDU) broke through the 18,000 mark for the first time this year.

The Nasdaq Composite Index (CCMP) is trading at a 15-year high.

Apple (AAPL), whose shares are up nearly 20% already this year, boasts a remarkable $750 billion market capitalization.

Stretched valuations

But valuations, as Goldman Sachs (GS) analysts noted this week, are getting really stretched. If that trend continues, at some point the stock market rally that began in March of 2009 is in danger of a sharp pull back.

Here are the key metrics that money pros are watching.

Goldman’s chief U.S. equity strategist David Kostin co-authored a note to clients on Feb. 20 that attracted a lot of attention.

His analysis of two key valuation ratios–share price to forecasted earnings and enterprise value to earnings before interest, taxes, depreciation and amortization–were flashing red.

As the Goldman analysts pointed out:

“The only time during the past 40 years that the index traded at a higher multiple was during the 1997-2000 Tech Bubble”

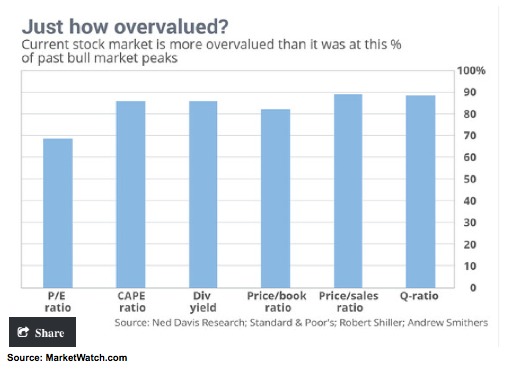

Six metrics

Back in mid-January, Marketwatch stock watcher Mark Hulbert analyzed six time-honored valuation measures and found that stock prices were “more overvalued today than they’ve been between 69% and 89% of the past century’s bull-market tops.”

The six metrics included price-to-earnings, price-to-book and price-to-sales ratios. Hulbert also looked at the Q ratio, which compares the market value of a company divided by the replacement value of the firm’s assets.

Rounding things out was the cyclically-adjusted price/earnings ratio (CAPE).

By all of these measures, this bull market is looking pricey compared to past rallies.

Timing is everything

Yet here’s the thing. Overvalued markets can party on for a very long time before a big correction or bear market appears.

U.S. Federal Reserve Chairman Alan Greenspan made his fabled “irrational exuberance” call in a speech he gave in December of 1996.

The dot.com-fueled Nasdaq didn’t peak until March of 2000.

In between, there was a lot of money to be made.

Bull’s case

Optimists don’t deny stocks are expensive for the most part. They just see countervailing forces that will keep share prices powering up.

While the Fed has ended its quantitative easing program and probably will raise rates at some point this year, it likely will move in baby steps.

In other words, credit conditions may be loosened well into 2016.

The job market is expanding at its fastest pace in 15 years. Wages have at long last started to climb.

The U.S. economy looks pretty good in comparison with the Eurozone and Japan.

Takeaway

All bull markets end at some point. The bedeviling thing, though, is that nobody has built a crystal ball to know exactly when.

Yet the data strongly supports the idea that market valuations are sky-high by historical averages.

High valuations, alone, may not tip the market in a different direction. But it’s definitely a risk factor.

Continued Learning: This bull market is on thin ice

Photo Credit: thenails via Flickr Creative Commons

The investments discussed are held in client accounts as of February 26, 2015. These investments may or may not be currently held in client accounts. The reader should not assume that any investments identified were or will be profitable or that any investment recommendations or investment decisions we make in the future will be profitable.

{kind=link}