By:

Simona M Mocuta, Chief Economist

Amy Le, CFA, Investment Strategist

Venkata Vamsea Krishna Bhimavarapu, Economist

Chair Powell signals potential rate cuts, UK inflation remains high, Japan’s CPI surprises, and global data releases offer mixed signals on growth, sentiment, and monetary policy direction.

US: Welcome Jackson Hole developments

The Fed Chair’s speech at the Jackson Hole symposium is always acutely relevant for investors, and it proved so once again this year. There were always going to be two key parts to this: the short-term outlook, on one hand, and changes to the policy framework, on the other.

In respect to the first, Chair Powell came across a little more dovish than we had dared hope. We welcome this, given our view that rate cuts are needed. Prior to the speech, we would have said that the data still needed to convince the FOMC to cut in September. After the speech, we would say that it needs to convince the FOMC not to cut. The big negative revisions to payrolls earlier this month have clearly shifted the balance. We may well move from dissents in favor of a cut in July to dissents in favor of a hold in September, but the center of gravity has shifted closer toward a cut. To be fair, Chair Powell only said that the outlook “may warrant adjusting” the policy rate. However, the lack of obvious caveats made this sound less like a possibility and more like a promise—one that markets evidently liked, with both equities and bonds up sharply.

There was a subtle hint to the political backdrop and ongoing open pressure from the administration toward rate cuts in Chair Powell’s reminder that “FOMC members will make these decisions, based solely on their assessment of the data and its implications for the economic outlook and the balance of risks. We will never deviate from that approach.” Concise and clear; just the right touch.

As to the strategy review, this is a perfect example of vision always being 20/20 in hindsight. Back in 2019/2020, with a decade of struggles with low inflation and operating at the effective lower bound (ELB), the Fed introduced several innovations to its policy approach, all of which have now been essentially reversed. Below is a summary of the latest changes.

- Instead of viewing ELB as a “defining feature of the economic landscape,” there is a commitment to “promote maximum employment and stable prices across a broad range of economic conditions” (our emphasis).

- Return to a pure form of average inflation targeting, without intentionally “making up” inflation shortfalls, since the need to do so has been rendered obsolete by post-Covid experiences.

- Maximum employment is no longer specifically described as a “broad and inclusive” concept but rather as “the highest level of employment that can be achieved on a sustained basis in a context of price stability.”

- Focus shifts from mitigating “shortfalls” back to the original approach of mitigating “deviations” in employment relative to the estimated equilibrium level. This was a practical choice to avoid communication challenges. The Fed remains primarily concerned about employment shortfalls but does not want that to be interpreted as “a commitment to permanently forswear preemption or to ignore labor market tightness.”

The changes were non-controversial and largely expected and bring the Fed back to the general approach followed pre-Covid. There is more of a two-sided approach to risks that could improve policy responsiveness.

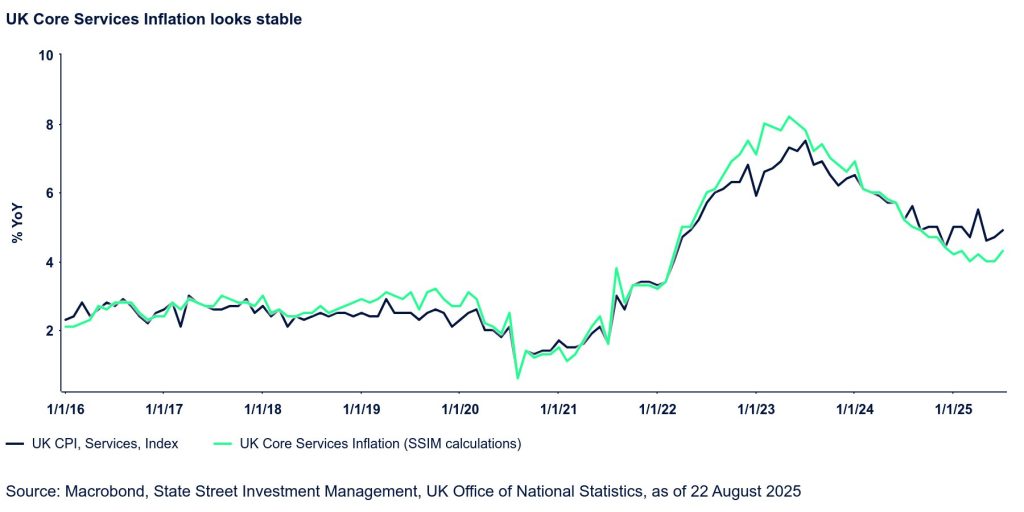

UK: Lower chance of November rate cut

Inflation remained persistently high in July, with underlying data highlighting several nuances. Services inflation, a key indicator tracked by the Bank of England, increased from 4.7% y/y to 5.0% y/y, driving a modest rise in core inflation largely due to a significant escalation in airfares. This airfare volatility is typical for July, as it is influenced by the timing of school holidays relative to survey periods. In contrast, hotel prices exhibited little month-on-month change, defying earlier projections of considerable growth linked to Oasis’ tour dates.

These short-term price fluctuations are generally deemed of limited significance for monetary policy considerations. Notably, the Bank’s preferred measure of services inflation, which excludes volatile and indexed elements, reached 4.3% y/y, well below the overall services inflation figure.

In August, the UK PMI reflected economic expansion at its highest pace in a year, driven by the services sector, while manufacturing activity stabilized. Nevertheless, demand remains subdued amid global uncertainty and concerns regarding Autumn Budget policy announcements. Goods exports continue to decline sharply, while firms reduced their workforce in response to weak orders and elevated costs, as inflation persists at 3.8%.

Accompanying the positive PMI results, an increase in GFK consumer confidence to -17 further underscores the economy’s resilience amid continued challenges for businesses and consumers. Survey improvements were generally broad-based, highlighted by a notable three-point improvement in household expectations for future public finances, reaching their highest level since August 2024. This level of optimism is notable considering the various factors currently influencing consumers, such as slower employment growth, weaker wage growth, higher inflation, and the potential for tax increases in the upcoming Budget.

Overall, ongoing resilience in economic activity and persistently elevated inflation indicate that the threshold for an additional rate cut remains substantial. However, regarding the services sector, we expect inflation to be somewhat lower than the Bank of England’s projections. As a result, we now view a November rate cut as probable, though there is uncertainty due to differing views within the rate-setting committee. The employment outlook will also be key, with jobs having declined in recent months, but recent survey data points to potential stabilization.

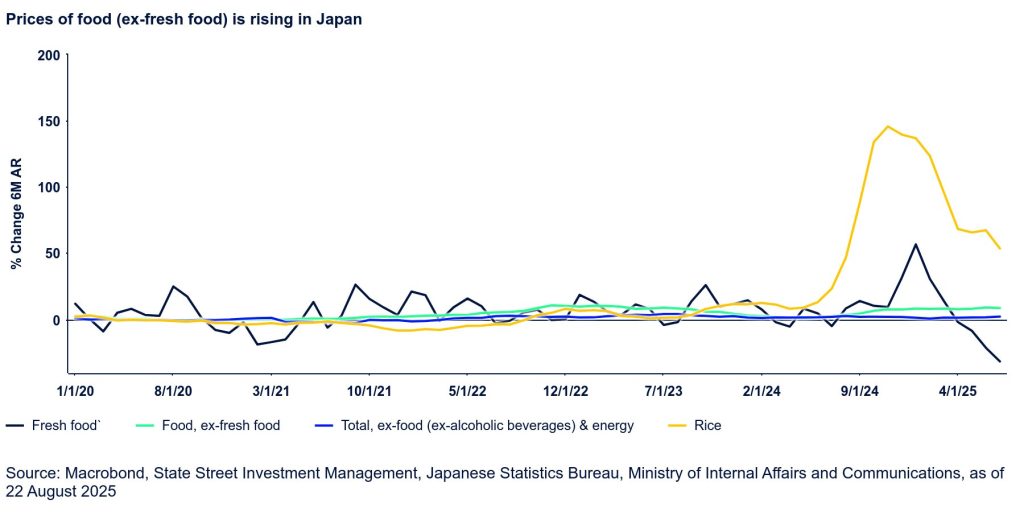

Japan: Inflation remains underrated

Headline CPI came a tenth above expectations at 3.1% y/y, marking the eighth month above 3%. The Bank of Japan’s (BoJ) preferred core metric (which excludes fresh food and energy) was up 3.4%.

Price pressures unsurprisingly remained strong in food at 0.5% m/m or 8.3% y/y. The BoJ believes this is due to supply constraints in rice, which has been leading the overall rise in prices; the Bank expects this to mean revert as supply normalizes. However, we believe that the Bank is underestimating the potential pass-through to other categories, as we notice that the 6-month annualized change of prices in food excluding fresh food is faster than fresh food. Furthermore, rice prices declined for the first time since April 2023 by 0.6% m/m, but we expect they rose sufficiently to begin lifting prices in other categories.

Electricity subsidies resumed in July, and together with other subsidies and mean-reverting rice prices, they would slow the annual inflation from August. Whether this will deepen the BoJ’s thinking on prices or whether the BoJ will change their outlook will depend on how much inflation slides in the coming months. We still expect CPI to average 3.0% y/y this year and see a small but rising chance for a BoJ hike in October.

Originally posted on August 25, 2025 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/sommart+sombutwanitkul

VIA SHUTTERSTOCK

DISCLOSURES

Marketing Communication

State Street Global Advisors (SSGA) is now State Street Investment Management. Please go to statestreet.com/investment-management for more information.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the applicable regional regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator”) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

The views expressed in this material are the views of SSGA Economics Team through the period ended 22 August 2025 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.