By:

Simona M Mocuta, Chief Economist

Venkata Vamsea Krishna Bhimavarapu, Economist

Amy Le, CFA, Investment Strategist

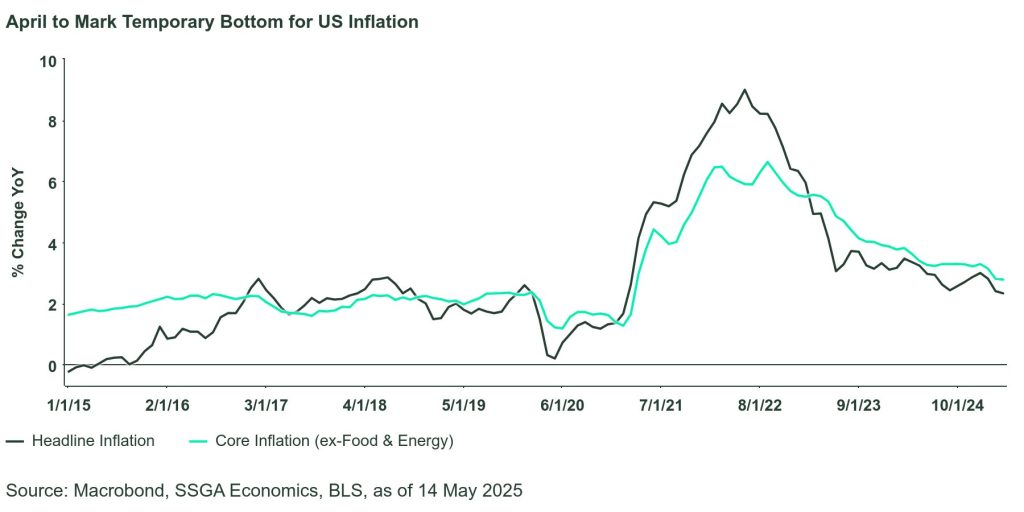

Both overall and core (excluding food and energy) consumer prices rose by 0.2% MoM. This allowed the headline inflation rate to ease to 2.3% YoY, while the core inflation rate remained unchanged at 2.8% YoY. These figures are the lowest since early 2021. However, these numbers are likely to be local bottoms due to challenging base effects and the impact of tariffs in the coming months.

US: OK Inflation, More Tariff Relief

Last week we said that the April inflation data could be a slight dovish surprise; the data this week confirmed that expectation. Both overall and core (ex food and energy) consumer prices rose 0.2% m/m, allowing the headline inflation rate to ease a tenth to 2.3% y/y and keeping the core inflation rate unchanged at 2.8% y/y. For headline, this was the lowest print since February 2021; for core, the twin-lowest since March 2021. That being said, these numbers are almost guaranteed to mark local bottoms for each of these series due to difficult base effects and tariffs impact over the next several months. Nevertheless, with the labor market already in balance, tariff risks greatly diminished amid ongoing negotiations, and the Fed Funds rate still in moderately restrictive territory, we very much continue to believe that the Fed should calibrate rates lower.

The details were perhaps less dovish than the headline. Goods prices were flat and service prices rose 0.4%, double the March rate. In addition to energy services, medical care services were a big driver, with prices jumping 0.5% m/m. Shelter prices increased 0.3% m/m, with OER up 0.4% m/m. Other, more discretionary areas of services were better behaved, with recreation flat and airline fares down 2.8% m/m. Food prices were bifurcated: Food at home prices declined 0.2% m/m, reflecting—among others—a big drop in egg prices (we think there is room for further reductions) while food away from home prices rose another 0.4% m/m. Energy prices increased 0.7%, largely on the back of a sizable increase in piped gas services. This was somewhat at odds with gas price behavior but may reflect delayed passthrough of prior cost increases.

Much more important than the April inflation data was the announcement of tariff de-escalation with China. In the April 14 Weekly Economic Perspectives we wrote the following: “The further increase in US tariffs on China (to 145%) and retaliatory Chinese tariffs on the US (125%) is no ‘joke’; it is very serious business, but not good business. We argued that the April 2 tariffs were unsustainable, and we argue the same here. There are many valid grievances that the US has vis-à-vis China’s trade practices. However, imposing tariffs of this magnitude goes far beyond making the point; it actually diminishes it. And so, we look forward to a near-term de-escalation so that meaningful negotiations can unfold. At the end of the day, the world needs the US, the US needs the world, and we all need trade.” The announcement this week of a 90-day delay in reciprocal and retaliatory tariffs between US and China bring back a sense of normality to global trade. It may be a fragile equilibrium, but the 90-day negotiation window is not just a holding place – its purpose is to turn it into something more robust. We remain watchful, but we are doing the watching with much less oppressive anxiety.

UK: Firm Growth, But on the Surface

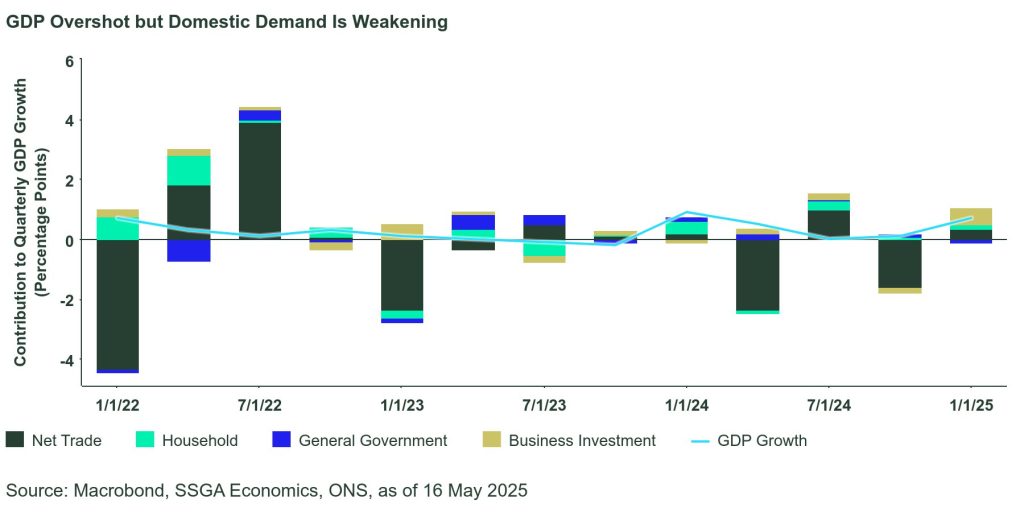

On the surface, the economy is expanding robustly with stronger-than-expected Q1 print. But the details were mixed.

The UK Q1 2025 print this week came in stronger than expected. Growth was 0.7% q/q, a sharp increase from the 0.1% q/q previous quarter and above market expectation of 0.6% q/q. Importantly, most of the strength in this quarter came from gross fixed capital formation (GFCF), and particularly business investment. Trade also outperformed with both exports and imports beating expectations. In contrast, household and government consumption performance was disappointed.

Nevertheless, the details raise questions about the sustainability of Q1 strength. Higher investment was mainly driven by large increases in transport equipment which is the major export to the US. Admitted, not all of these will be exported to the US, but it does suggest some element of Trump effect and is linked to front-loading. Exports to the US rose by £2.4bn in Q1 (to £17.5bn) while imports were up £1.3bn (to £15.4bn). That said, we would expect this growth to fade in the coming months.

The modest increase 0.2% q/q in household consumption reflects higher spending on household goods and services and housing. This is contrast to recent retail sales figures, which have been surprisingly strong. However, GDP data does lag retail sales and so there are chances that these measures could converge over the coming months. Meanwhile, the decline in government spending (-0.5% q/q) was due to lower healthcare and education spending. Here, it suggests that the fiscal stimulus has faded faster than we expected.

Overall, the implications of this print are still unclear. On one hand, the GDP overshot on the back of a decline in government spending does suggest an underlying strength that has not been captured in recent data. On the other hand, it’s now looking that supply has not been constrained as much as previously thought while demand weakening continues. That will help to limit the upside risks to the inflation.

Japan: GDP Disappoints, but Domestic Demand Is Firm

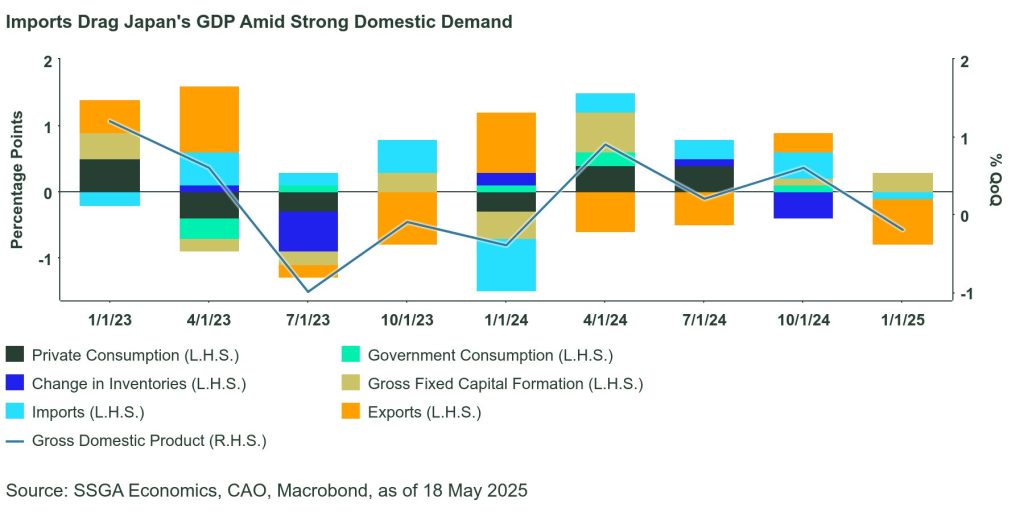

The preliminary estimate of Q1 GDP showed that it contracted -0.2% q/q (-0.7% annualized), missing our +0.3% pick by a big margin. The key difference came from external demand, which turned negative for the first time in four quarters. Exports were in line with expectations at 3.8% y/y, although services exports (tourism) eased as usual in the first quarter owing to seasonality. However, very interestingly, imports overshot expectations at 6.5% and within that, services imports were even stronger with a sequential rise of 4.5% q/q, highest since Q3 2023. All this meant that net exports detracted a massive 0.8 pp off of growth.

On the contrary, domestic demand was very resilient as expected and added 0.7 pp to growth. Private consumption rose 1.6% y/y, the strongest showing since Q1 2023. Durable goods consumption shot up 13.6%, highest since Q2 2021. All other categories also performed better with expectations.

The most significant positive surprise however was capital expenditures, which rose 3.6% y/y, the highest since Q3 2019! This is all the more surprising as we expected capex to have stalled on heightened uncertainty; notwithstanding it, the rise came on the back of labor shortages as well as a strong corporate intent on investments. Private housing investments also rose sharply by 3.0%.

So, on the surface, GDP missed our expectations by a lot, but details imply more of an upside surprise. Hence, we view the data as very encouraging, especially as consumption was strong while capital expenditures remained resilient.

From hereon though, the outlook depends entirely on how, when, and whether Japan signs a trade deal with the US, on which there has been little progress. Media reports suggest that Japan is negotiating hard on auto tariffs, which account for over three-fourths of its deficit with the US and also a key focus for President Trump.

Prime Minister Ishiba is positioning himself for the upper house elections in July, which is a very hard given his weaning popularity and tough choices on trade. He reportedly is not willing to let US agricultural imports into Japan too, failing which could weaken the prospects for his Liberal Democratic Party, considering the sector’s powerful lobby. The hard-bargain strategy could backfire not only on PM Ishiba, but also on the Japanese economy and we worry if the Bank of Japan (BoJ) will have to eventually take a longer pause than expected. In the face of this raging uncertainty we maintain our macro outlook, that Japan’s GDP may rise between 0.7%-1.0% in 2025 and that the BoJ might hike only once, likely in Q4.

The focus for the next week will squarely be on the third round of negotiations with the US in Washington. We look forward to some positive developments.

Originally posted on May 19, 2025 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/Mattdoodles

VIA SHUTTERSTOCK

DISCLOSURE:

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the applicable regional regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator”) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

The views expressed in this material are the views of SSGA Economics Team through the period ended 16 May 2025 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.