By: Samuel Rines, Macro Strategist, Model

Key Takeaways

- The current focus of the FOMC is on achieving the inflation mandate rather than the employment mandate.

- The FOMC is more concerned about the risk of inflation than the state of the labor market.

- Unemployment remains low and is not a major concern for the FOMC unless it rises substantially further.

The Federal Open Market Committee is always data-dependent. But the dependency is not always the same. There are times when inflation matters more than the labor market, and times when the situation is reversed. Every regime is unique. There is never a perfect corollary to a previous experience. This time is not different.

This time, it is a confidence game. One where the FOMC needs to be incrementally more confident about the trajectory of inflation. There is less—arguably, much less—focus on the state of the labor market. And that makes sense. The full employment mandate is not under the same pressure as the stable prices. When confronted with a tilted risk outlook, the FOMC reacts to it. And, in the current monetary policy regime, ties it to data.

It is that data that matters. When the FOMC tells you what will cause it to move policy rates, it should not be ignored. It should be embraced. That makes the question relevant to every single data point, “Does this alter the FOMC’s inflation confidence?”

The short answer is, “Maybe?” The longer answer is, “Maybe.” It is all about confidence, and there is less confidence in achieving the inflation mandate than accomplishing the employment mandate.

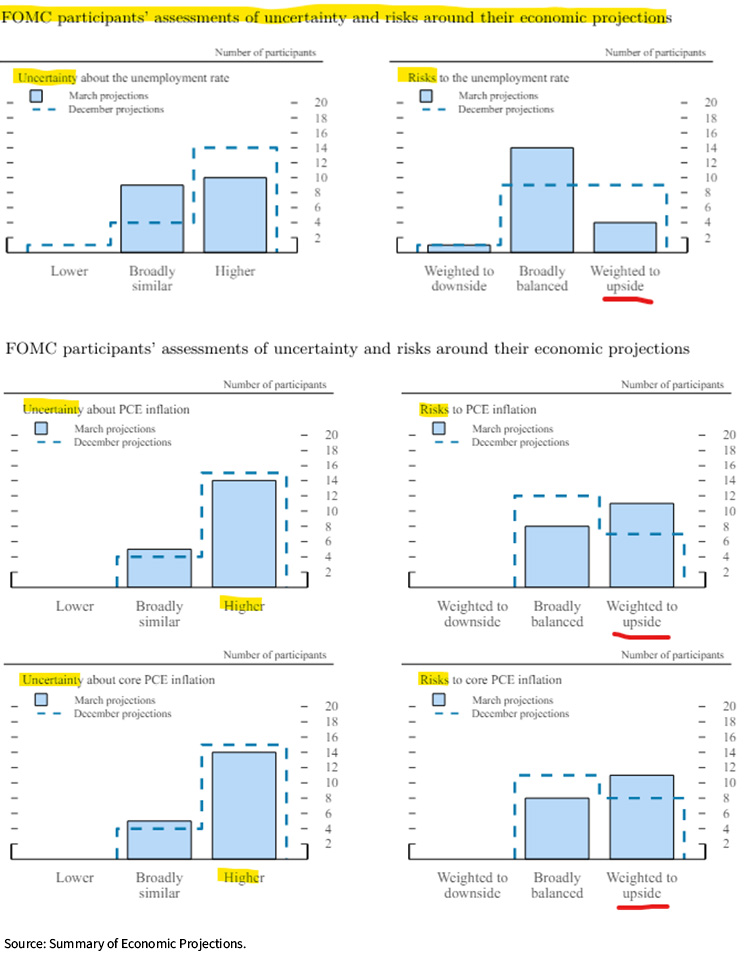

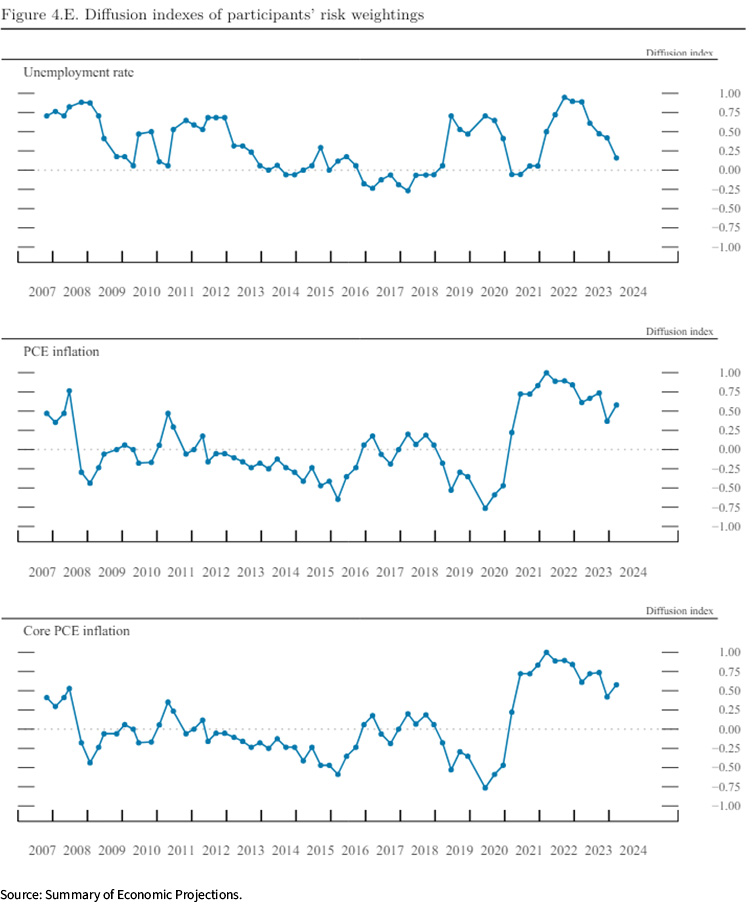

There is a reason for the outsized attention being paid to the inflation side of the mandate. There is more uncertainty and risk to the upside, according to the FOMC. The members of the policy setting committee are simply not concerned about the employment side. That creates a “tilt” in the policy framework toward inflation data and away from employment data.

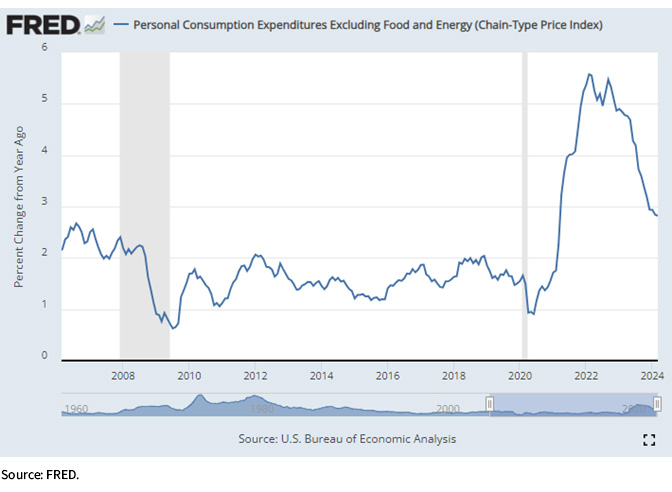

This dynamic is confusing. Prior to the current inflationary episode, the employment mandate was the “risk.” That is no longer the case. It is difficult to stress the importance of this development. In the wake of the global financial crisis, core PCE (the FOMC’s preferred gauge of inflation) consistently ran below the 2% target. At the time, the debate was about getting inflation higher, not lower.

That paradigm is no longer relevant. It is now all about accomplishing the mission of an inflation return to 2%. This is consistent with the long-term message from the FOMC, too. At the annual gathering of central bank officials in Jackson Hole, Powell gave a speech about the commitment to tackling the inflation problem, warning there could be pain ahead.

The pain has not materialized. Unemployment remains sub-4%, and the FOMC is unlikely to be concerned about unemployment unless it rises substantially further. How can we know this? The FOMC releases its “longer-run” view of the unemployment rate. Currently, unemployment sits at 3.9%. That is the bottom of the range for the Committee’s outlook this year (3.9%–4.1%). The longer-run range the FOMC would be happy with is 3.8% to 4.3%.

The inflation concentration is not something that needs to be implied. The FOMC is being rather open and blunt about it. Unemployment is not an issue, but inflation is. The “dual mandate” is now a single mandate.

Eventually, this will shift back to a more balanced mandate. But that will take persistently better news on inflation and negative news on the labor market. Much as one piece of positive news on inflation is not going to provide the FOMC with enough confidence to cut rates, one piece of negative employment news is not going to cause the FOMC to panic either. The single mandate is here. There is no reason to fight it.

This post first appeared on May 23rd, 2024 on the WisdomTree blog

PHOTO CREDIT: https://www.shutterstock.com/g/rozbyshaka

Via SHUTTERSTOCK

Disclosures:

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see the prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

{kind=link}

{kind=link}