By: Jose Torres, Interactive Brokers’ Senior Economist

Investors are indecisive today at the start of a holiday-shortened week featuring the return to one-day stock settlement, otherwise known as T+1. Meanwhile, market participants are digesting an upside beat on consumer confidence while listening to Fed speakers talk about growth, the balance sheet, inflation and rate prospects.

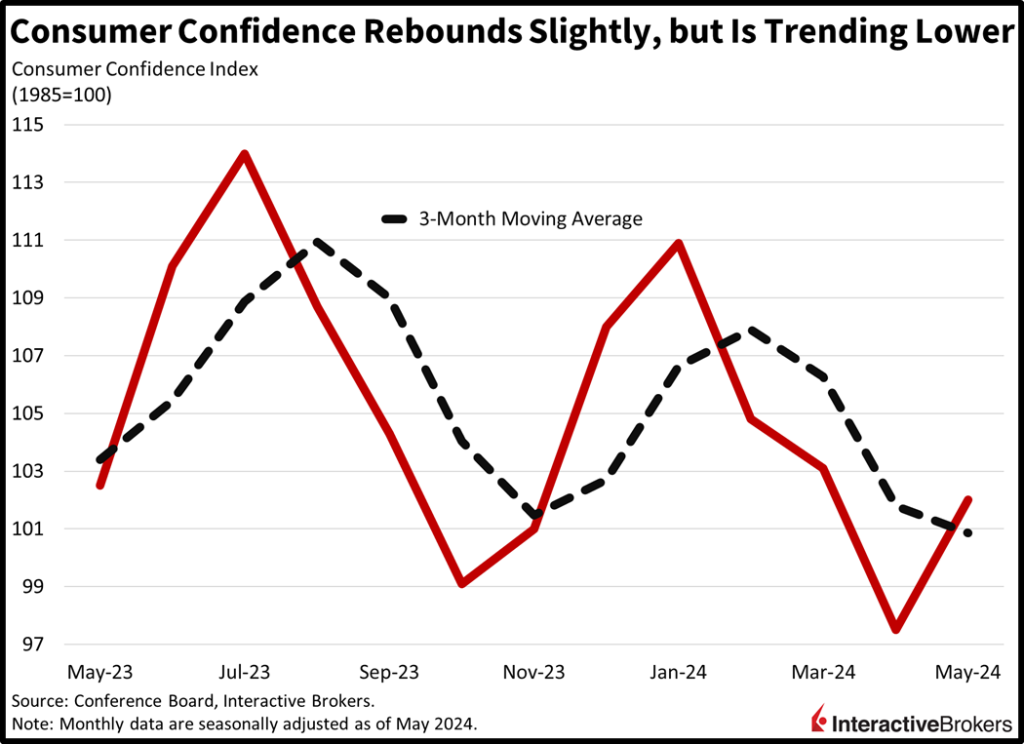

Consumer Sentiment Brightens

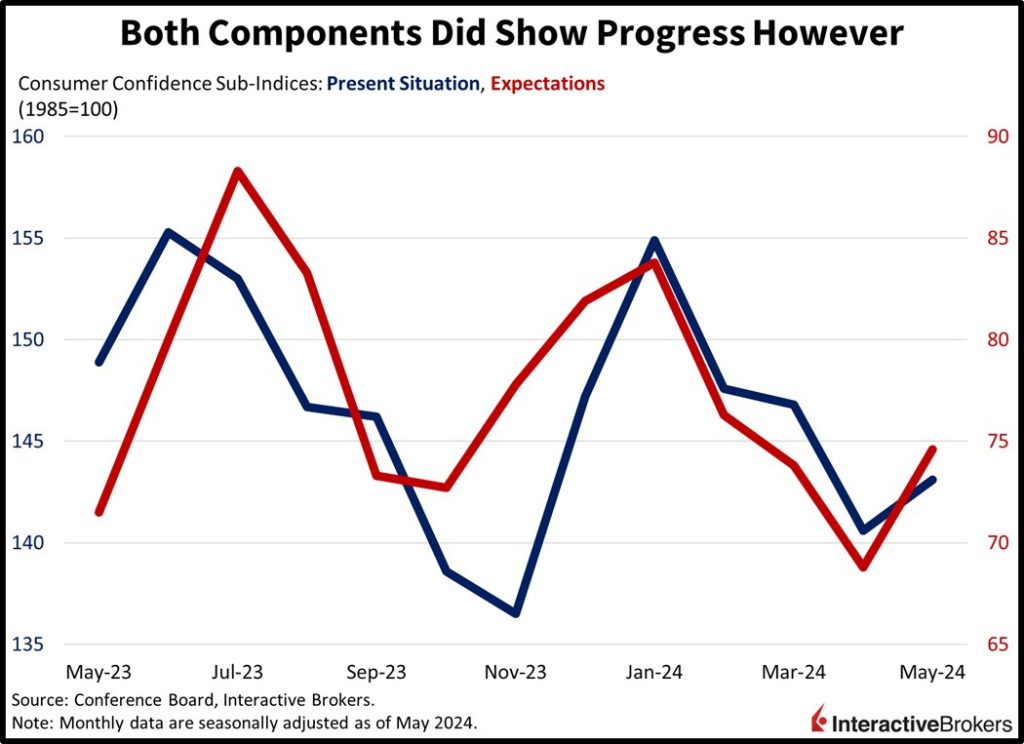

Consumer moods improved this month on the back of stock market optimism following three consecutive months of declines. May’s Conference Board Consumer Confidence index rose to 102, arriving well ahead of the 95.9 median estimate and last month’s 97. Both the Present Situation and Expectations components contributed to the uptick, increasing from 140.6 and 68.8 to 143.1 and 74.6, respectively. Households were content with tight labor conditions as well as future prospects concerning business possibilities, employment and income. Folks were concerned about lofty prices, however, especially for nutrition, while maintaining pessimistic outlooks for disinflation and rates as a result. Plans for big-ticket purchases remained depressed with elevated prices, steep borrowing costs and reduced credit availability weighing on ordering activity. Finally, Americans called the odds for recession likely while CEOs were more sanguine, sustaining odds of roughly 35%.

Kashkari Maintains Hawkish Stance

In a CNBC interview today, Minneapolis Federal Reserve President Neel Kashkari shared a hawkish view on fighting inflation. While Fed members, broadly speaking, want more data pointing to a sustainable decline in price pressures before cutting, Kashkari said he thinks “many more months of positive inflation data” are needed before monetary policy should be eased. He also said he hasn’t ruled out raising if inflation doesn’t improve. Kashkari is a non-voting Fed member but provides input during policy discussions. He will become a voting member in 2026. In April, the year-over -year (y/y) inflation rate was 3.4%. Kashkari said the Fed may eventually increase its current 2% target inflation rate, but doing so now would be inappropriate.

Also today, Fed Governor Michelle Bowman, during a conference in Tokyo, said she thinks the Fed’s decision earlier this month to slow its reduction in the size of its balance sheet was premature. The Fed should have either kept the previous rate or made a smaller reduction in the pace at which it is contracting the balance sheet. Bowman says the banking system has adequate reserves, so the Fed can reduce the balance sheet at a faster pace. Advocates for maintaining the current pace point to 2019 when the Fed slashed its balance sheet too quickly, causing the repo market to freeze and interest rates to hit 9%. The Fed had to inject emergency funding back into the banking system to restore liquidity. During the same conference, Federal Reserve Bank of Cleveland President Loretta Mester said the Fed needs to evaluate its methods for communicating its views on how changes in the economy could impact monetary policy. By expanding discussions regarding potential risks, the Fed could protect its credibility if it unexpectedly needs to shift its monetary policy. She added that the current post-meeting public statement provided by the Fed is too short, causing investors to place too much emphasis on individual words. Additionally, the Fed should consider providing scenario analysis, which would explain potential reactions to different changes in economic indicators. The Fed is likely to assess its communications as part of a five-year review expected to start at the end of this year.

Markets Return to T+1 Trading

Investors are watching to see how the transition to one-day trade settlement or T+1 starts today. It is the first time in 100 years since T+1 has occurred. The prior practice, handled manually, was terminated when volumes grew, making it impractical. With the implementation today, investors will get faster settlement but have less time to correct trading errors. Additionally, it creates challenges for cash settlement with cross-border trading. Over the long term, T+1 is expected to improve liquidity, but in the short term, it may create an increase in failed trades. With this in mind, the Securities Industry and Financial Markets Association have created the T+1 Command Center to identify and respond to problems.

Tech and Growth Rally

Technology shares are dominating the tape today with limited bullish action occurring outside of growth. Indeed, the Nasdaq Composite Index is the only gainer out of the major equity benchmarks; it’s up 0.2%. Meanwhile, the S&P 500 and Russell 2000 baskets are near the flatline while the Dow Jones Industrial Average is down a meaningful 0.4%. Sectoral breadth is negative with four out of eleven sectors trading north, led by energy, technology and utilities: they’re up 0.8%, 0.5% and 0.2%. Piloting the laggards are the health care, financials and consumer staples, which are losing 1.2%, 0.9% and 0.9%. We’re witnessing some bifurcated action across the yield curve as the short-end moves slightly lower while longer-dated maturities shift higher. The 2- and 10-year Treasury maturities are changing hands at 4.93% and 4.49%, 2 basis points lower for the former but higher for the latter. The greenback is slightly lighter and down relative to most of its counterparts, including the euro, pound sterling, franc, and Aussie dollar. The US currency is gaining versus the Canadian dollar and the yen. Energy stocks are benefitting from an increase in the price of crude oil, with WTI up 1.2%, or $0.97 to $79.49 per barrel. The commodity is being relieved by the expectation that the OPEC+ cartel will maintain supply limits at its meeting this Sunday amidst forecasters that hope the unofficial beginning of the summer season will bring many Americans to the highways and the skies. Silver, gold and copper are also trading higher by 0.8%, 0.5% and 0.4%.

Recent Price Softness Likely to Reverse

Market players are quite tranquil as they review today’s data and Fed speak, with rate prospects not moving much. Indeed, fed funds futures point to just one cut this year, with September offering coin-flip odds. Much of the path will be influenced by incoming labor and price data, with strength extending our journey across the monetary policy bridge while weakness will bring the scissors closer to home. We’re expecting May inflation data to offer a reprieve due to cratering oil prices, but core segments will remain sticky, a result of rising services and goods costs. In conclusion, the positivity of May price pressures could just be one month, as loose financial conditions, exuberance in markets and geopolitical uncertainty turn inflation the other way in June.

Visit Traders’ Academy to Learn More About Consumer Confidence and Other Economic Indicators

This post first appeared on May 28th 2024, Traders’ Insight Blog

PHOTO CREDIT: https://www.shutterstock.com/g/eamesBot

Via SHUTTERSTOCK

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}

{kind=link}