“It’s difficult to make predictions, especially about the future.”

– Niels Bohr

By: Michael W Arone, CFA, Chief Investment Strategist

Investors excitedly welcomed a much needed rebound in investment performance last year after a challenging 2022. Despite the better results, decisions about how to allocate investment portfolios among stocks, bonds, alternatives, commodities, and cash didn’t get any easier.

Bold predictions for a US recession, economic resurgence in China, value stocks’ leadership, and poor performance from below investment-grade credit (junk bonds and loans) were all proven wrong. Instead, the Magnificent Seven, largely driven by the artificial intelligence (AI) frenzy, accounted for nearly two-thirds of the S&P 500 Index’s surprising 26.3% gain last year.1 This concentration in investment performance made it practically impossible for investors to own enough of the Magnificent Seven in diversified portfolios to beat their benchmarks. Maddening.

The past four years underscore just how difficult it is to make accurate predictions about the future.

But as the Chief Investment Strategist for State Street Global Advisors, I must participate in the annual forecasting foolishness. It’s what you do. This will be my ninth consecutive year of reluctantly forecasting three surprises for investors. I’m a decent 14 for 24 (58%) in my prediction accuracy over eight years. But 24 is far too few observations to determine whether I have any forecasting skill or just dumb luck.

Investment Process Supports Forecasts

Investment outcomes are always highly uncertain.

Thankfully, investors can avoid the pitfalls of prediction by simply focusing on the one thing firmly in their control — a consistent, disciplined, and repeatable investment process. A thoughtful investment approach combined with a little luck provides investors the best opportunity for long-term success.

Practicing what I preach, the consistent application of a simple surprise forecasting formula matters most to my prediction success. So, for the ninth straight year, I’ve identified unloved assets with compelling valuations, where a lot of bad news is already priced in and investor sentiment is decidedly one way.

My three surprises for 2024 are:

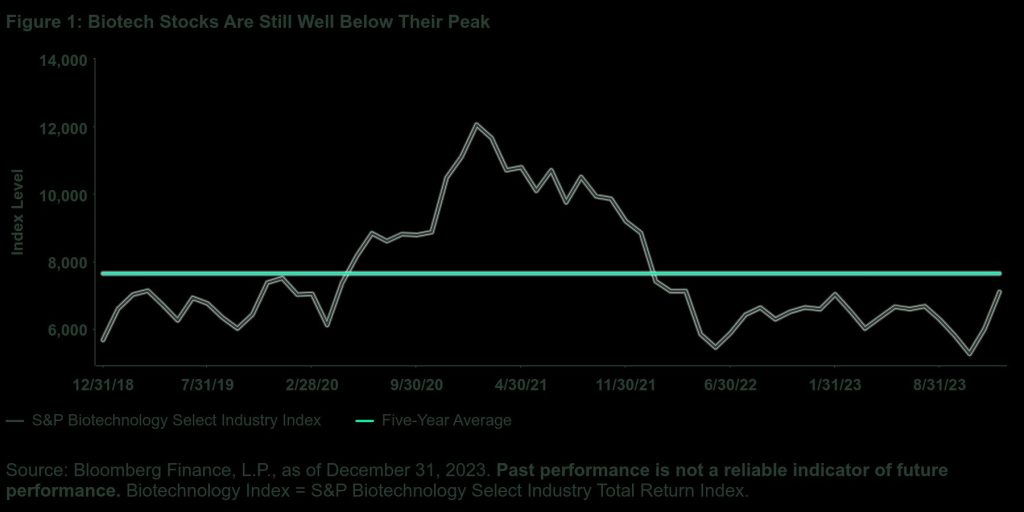

Biotech Beats the S&P 500 Index

The S&P Biotechnology Select Industry Index trailed the S&P 500 Index by 18.5% last year. This poor relative performance led to $3.1 billion in outflows from biotech exchange traded funds (ETFs) in 2023.2

Meanwhile, incredibly long lead times in drug development reveal that biotech companies don’t often realize profits for years, sometimes a decade or more. Consequently, rising interest rates in the past few years have decreased the value of biotech’s future profits, further depressing stock performance.

And while M&A activity has historically been an important driver of biotech returns, the current environment is the worst for M&A since the Global Financial Crisis. Global deal values across all industries halved in the past two years from $5 trillion to $2.5 trillion, according to PwC’s “Global M&A Industry Trends.” Additionally, global deal volumes for all industries fell 17% and megadeals — transactions with a value in excess of $5 billion — declined by 60% from 2021 to 2023.3 This weaker M&A activity has been a headwind for biotech stocks’ performance.

Finally, windfall profits from the development and distribution of COVID-19 vaccines produced a challenging comparable year-over-year earnings environment for several biotech stocks. This resulted in disappointing biotech earnings in 2023.

All of this biotech bad news creates an unloved investment opportunity with a compelling valuation, ripe for an upside performance surprise. Expectations for Federal Reserve rate cuts and falling interest rates should boost the value of biotech’s future earnings.

Improved market conditions, pent-up supply and demand for deals, and pressing strategic needs for companies to transform their business models will result in an increase in M&A activity, according to PwC. Large pharmaceutical companies pursuing midsize biotech targets to fill drug pipeline gaps, strong investor interest around diabetes and weight loss GLP-1 drugs, and a continued focus on precision medicine also are likely to fuel M&A activity this year.4

And comparable year-over-year earnings from biotech companies should get easier in 2024. Perhaps biotech companies will exceed modest analyst earnings expectations this year, further supporting the stocks.

For my first surprise, I predict that the S&P Biotechnology Select Industry Index will outperform the S&P 500 Index in 2024.

Real Estate Rebounds

Current investor psychology has made real estate investing synonymous with commercial real estate challenges. This is a mistake.

The Dow Jones US Select REIT Index underperformed the S&P 500 Index by 12.3% last year.5 Higher interest rates, overblown commercial real estate fears, and poor relative performance have resulted in continued outflows from real estate ETFs.

Investors’ anxiety about the post-pandemic outlook for commercial real estate has wrongfully infected all of real estate investing. But a quick review of the Nareit website reveals there are four types of REITs — equity, mortgage, public non-listed, and private. Further examination indicates that there are 14 REIT sectors, from residential to data centers and practically everything in-between. In fact, office REITs make up less than 6% of the Dow Jones US Select REIT Index.

There are plenty of real estate opportunities for investors beyond the landmines in commercial real estate investing.

Lagging performance and fund outflows have created a compelling valuation opportunity in an unloved asset where a lot of bad news is already priced in and investor sentiment is decidedly one way. In addition, expectations for declining interest rates, solid pricing power, strong growth in funds from operations (FFOs), attractive relative valuations, and tempting dividend yields set up REITs nicely for a possible upside surprise this year.

For my second surprise, I predict that the Dow Jones US Select REIT Index will outperform at least 65% of the 11 S&P sectors in 2024.

Figure 2: REIT Performance Still Trailing the S&P 500

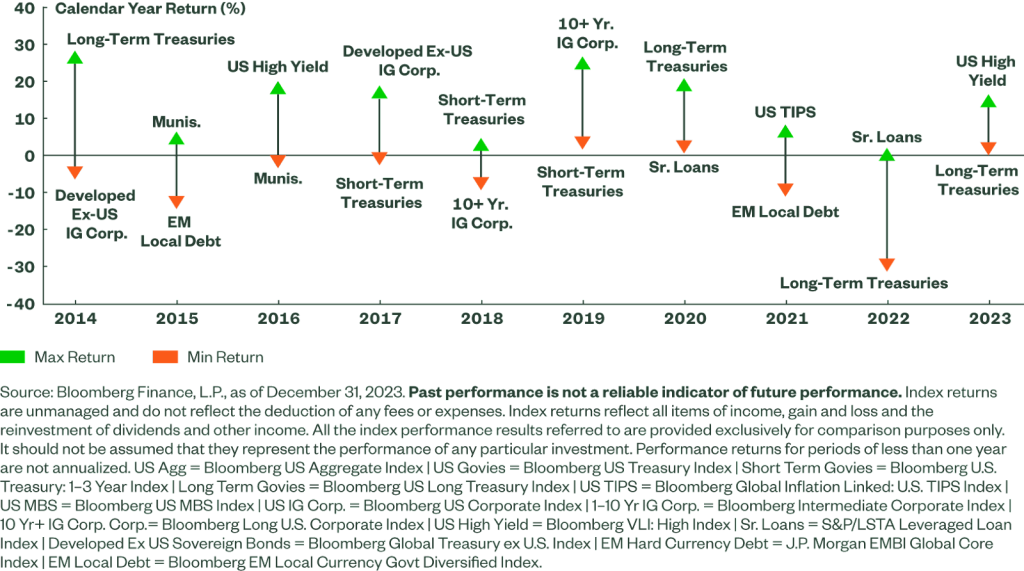

High Yield Repeats as Top Bond Performer

High yield bonds defied the odds and the faulty recession predictions last year by returning 13.5%, beating the Bloomberg US Aggregate Bond Index by nearly 8% in the process.6 Despite the substantial outperformance, high yield ETFs suffered outflows for most of the year, until some aggressive performance chasing in November and December.

Expectations for a recession in 2023 made investors wary of taking on too much below investment-grade credit risk in fixed income allocations. When it became clear that the soft landing outcome was possible, the high yield performance chase was on in earnest.

Yet, there remains a healthy dose of investor skepticism regarding the performance prospects for a repeat in high yield bonds this year. Most investors still express a preference for rates over spreads in fixed income allocations. Said plainly, investors expect interest rates to fall this year, rapidly pushing up the prices and total returns of longer maturity bonds. And, they anticipate that the total return from falling interest rates on bonds will surpass the total return from the narrowing of credit spreads.

So far, interest rate volatility has remained unexpectedly high in early 2024; 10-year Treasury yields have increased from the lows reached at the end of December, putting downward pressure on longer maturity bonds. Confusion about the future path of monetary policy combined with the poor fiscal position of the US could keep interest rate volatility elevated this year.

With the soft landing seemingly within our grasp, yields close to 8%, high interest coverage ratios, reasonably low default rates, and robust corporate profitability make high yield bonds an attractive total return option within fixed income allocations.

For my third surprise, I predict that high yield bonds will again be one of the top-performing fixed income sectors in 2024.

Figure 3: Top- and Bottom- Performing Fixed Income Sectors Vary by Calendar Year

There Is Neither Happiness Nor Misery in the World

Last year produced a strange emotional contradiction for investors. On the one hand, they were elated by the rebound in investment performance. On the other hand, they were irritated by all of the inaccurate predictions, surprise outcomes, and asset allocation challenges.

For my part, I shared in both investors’ elation and irritation. Toward the end of summer 2022, I became bullish on stocks and eventually my enthusiasm was rewarded with the rally that began on October 12, 2022 and continues to this day. But hardly any of the size, style, sectors, industries, and stocks that I thought would lead the markets higher have led.

And, for the first time in eight years, I failed to accurately predict a single surprise in 2023, going 0 for 3. I predicted that Financials would outperform the market last year. After a rough first quarter, the sector did produce a respectable 12% return for the year but sizably underperformed the S&P 500 Index by roughly 14%.7 I also forecast that European stocks would beat US stocks. This prediction was closer but still no cigar! The STOXX Europe Total Market Index returned nearly 20% but still trailed the S&P 500 Index by more than 6%.8 Finally, I predicted that a diversified portfolio of real assets would outpace the 60/40 portfolio and that didn’t happen either.

Many of 2024’s Wall Street forecasts are already off to a shaky start. A few may be proven right. Most will be proven wrong. Investors shouldn’t let incorrect forecasts and unexpected outcomes discourage them. It’s to be expected. Investment results are always random, especially in today’s environment where the range of outcomes is wider than normal.

What investors can control and count on is that a consistent, disciplined and repeatable investment process provides them with the best opportunity for long-term success. Here’s to being pleasantly surprised again in 2024!

Get more of Michael Arone’s Uncommon Sense, unconventional perspectives to help you think beyond the consensus.

This post first appeared on January 31st, 2024 on the SSGA blog

PHOTO CREDIT:https://www.shutterstock.com/g/ESB+Professional

Via SHUTTERSTOCK

Footnotes

1 Bloomberg Finance, L.P., January 29, 2024.

2 FactSet, December 31, 2023.

3 Brian Levy, Global M&A Industry Trends, PwC, January 23, 2024.

4 Brian Levy, Global M&A Industry Trends, PwC, January 23, 2024.

5 Bloomberg Finance, L.P., December 31, 2023.

6 Bloomberg Finance, L.P., December 31, 2023.

7 Bloomberg Finance, L.P., December 31, 2023.

8 Bloomberg Finance, L.P., December 31, 2023.

Disclosure:

Important Risk Information

Marketing Communication

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

The views expressed in this material are the views of Michael Arone through the period ended January 29, 2024 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward looking statements.

Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Investing involves risk including the risk of loss of principal.

Past performance is not a reliable indicator of future performance.

All material has been obtained from sources believed to be reliable. There is no representation or warranty as to the accuracy of the information and State Street shall have no liability for decisions based on such information.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without State Street Global Advisors’ express written consent.