By: Matthew J Bartolini, CFA, CAIA, Head of SPDR Americas Research and Martin D Dunn, Research Strategist

The fixed income market exhibits traits that can lead to inefficiencies and mispricings, giving active managers the chance to use their expertise to potentially generate higher returns.

Can fixed income investors gain an edge with active management? Explore the reasons why skilled managers may be able to generate alpha in fixed income, and the advantages of the ETF wrapper for actively managed fixed income strategies.

Fixed Income Market Inefficiencies

When ability meets opportunity, portfolio managers can potentially produce excess returns. To better understand this concept, consider the fundamental law of active management.

Developed by Richard Grinold in 1989,1 the “law” assesses a manager’s ability to add value. It suggests the value added by the investment strategy is related to two variables: (1) the manager’s skill in forecasting exceptional returns, and (2) the breadth of the strategy. To represent breadth, analysts typically use the number of securities within a given investment universe. The more breadth a market has, the more opportunities skilled managers have to generate alpha.

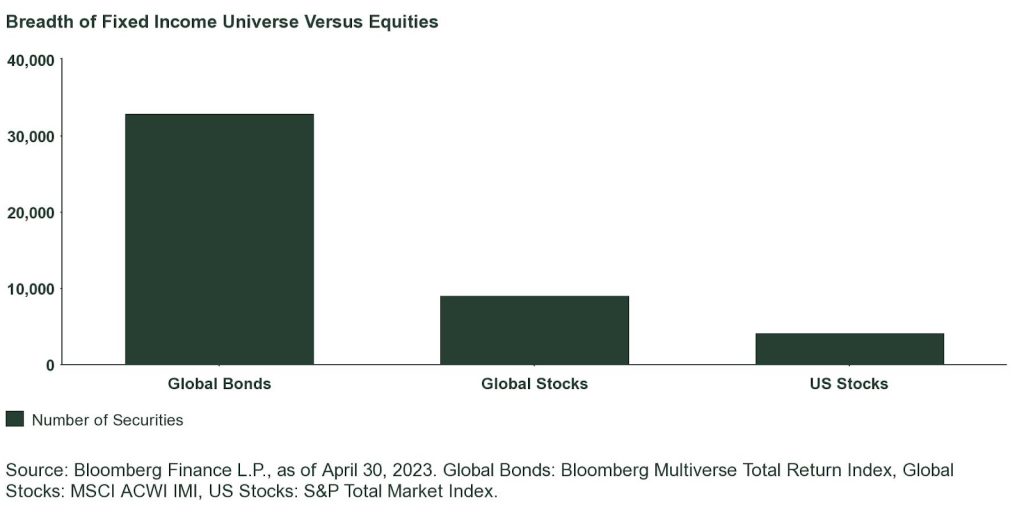

The global fixed income universe is exceptionally deep, diverse, and complex, offering ample breadth for active managers. The sheer number of fixed income securities is enormous, especially when compared to the equity universe. As shown below, an index of global bonds includes nearly 33,000 securities, while a similar index of global stocks has fewer than 10,000 holdings.

Breadth of Fixed Income Universe Versus Equities

Many pockets of the fixed income universe exhibit dimensions of risk that give rise to inefficiencies and mispricing — creating opportunities for active managers to use their skill to generate benchmark-beating returns.

Sources of excess return can be cyclical, arising from deviations from fair value and periodic movements in various markets — for example, mispricing on expected rate movements as a result of Fed policy changes. Or sources of alpha can be tactical, where specific events may cause temporary dislocations — for example, contagion risk fears from a regional banking crisis distorting the fair value of non-related banking firms. Long-term trends may also support structural risk premiums, such as liquidity, carry, and credit.

How Active Managers Can Capitalize on Opportunities

Active managers can exploit systematic and structural inefficiencies in fixed income through different methods, including:

- Security selection

- Cash management

- Sector rotation

- Yield curve positioning

- Position sizing

Managers can make active portfolio decisions using both top-down and bottom-up approaches that incorporate fundamental research and quantitative techniques. Active managers can rotate toward or away from certain risks, such as duration (by increasing or decreasing interest rate sensitivity) and credit quality (by adding or avoiding riskier credits like high yield or emerging market debt).

Treasury holdings are a good example of where increased available breadth can potentially benefit active fixed income approaches. An index-tracking ETF may need to hold the newest, most-liquid Treasury bonds that have recently been added to the benchmark. Meanwhile, an actively managed ETF may have the flexibility to buy off-the-run Treasury securities that offer better relative value.

Similarly, a passively run portfolio may need to track a market-capitalization-weighted credit index that gives more weight to issuers with large amounts of outstanding debt. But an actively managed strategy can examine the debt load of the company and determine if it is reasonable based on underlying fundamentals and cash flows. So they have more discretion over what debt they buy from a specific company (i.e., target a specific spot in the credit curve) — and possibly have the freedom to invest across a broader opportunity set. The impact is even greater when moving into more non-traditional (e.g., loans) or securitized portions (e.g., agency and non-agency MBS) of the bond market.

Active core and core-plus strategies are a timely example. These strategies usually blend traditional and non-traditional fixed income asset classes to pursue the highest possible return over a full market cycle. Through active sector allocation and security selection, these strategies may offer better protection against interest rate risk and credit risk than benchmark-linked core or aggregate bond strategies.

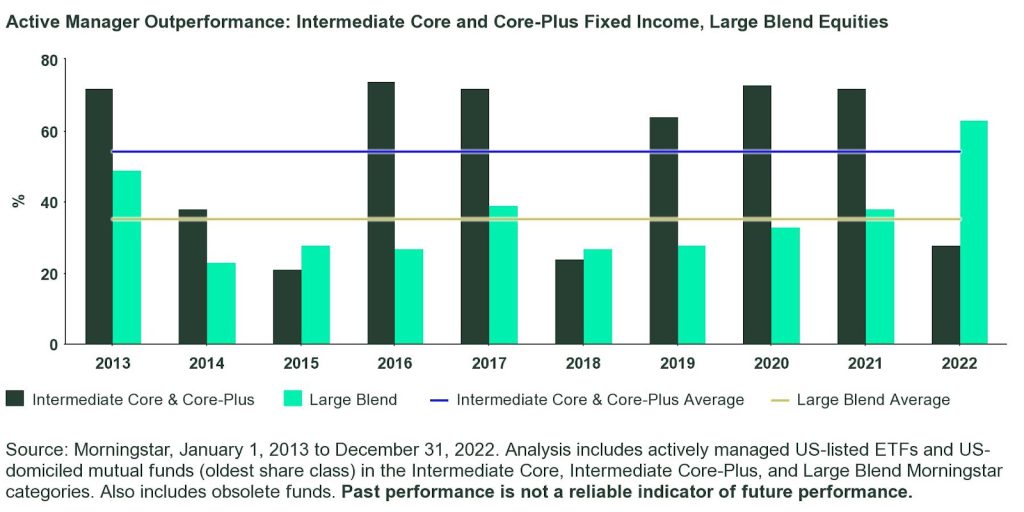

Historically, the majority of active intermediate core and core-plus strategies have produced above-benchmark returns. As shown below, over the past decade, an average of 54% of active intermediate core and core-plus fixed income managers outperform their benchmark. When looking at active large blend equity strategies, the core category for equities, only 35% outperformed on average. In our view, this gap illustrates the outsized opportunity for skilled managers to generate alpha for the core of fixed income portfolios.

Active Manager Outperformance: Intermediate Core and Core-Plus Fixed Income, Large Blend Equities

Growth of Actively Managed Fixed Income ETFs

For fixed income investors who want to go active, strategies are available in a variety of wrappers, including ETFs. Active fixed income ETFs were initially limited to ultra-short bond strategies. But today, a wide variety of strategies exist.

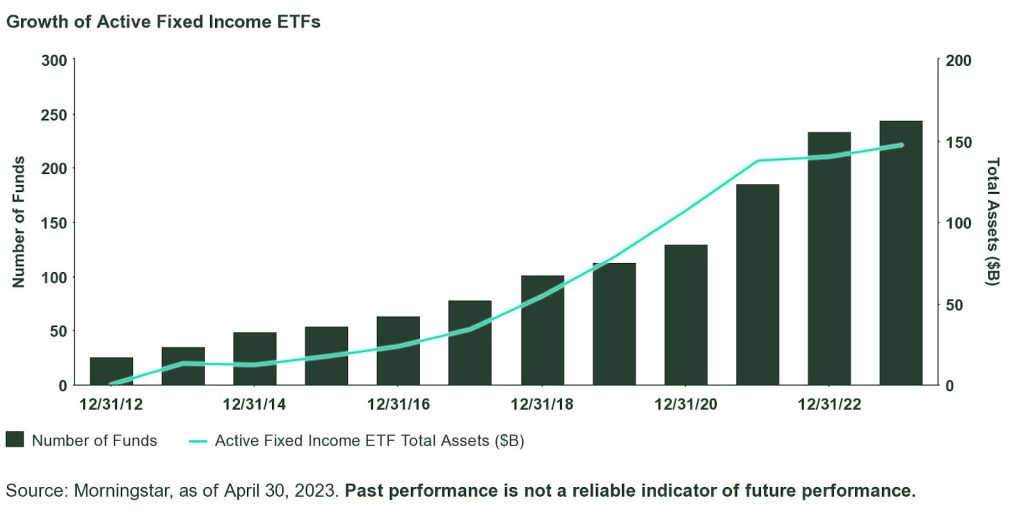

As shown below, active fixed income ETFs had total assets of $9.6 billion across 12 Morningstar categories at year-end 2012. Active fixed income ETFs have grown to more than $147 billion in assets spanning 27 different categories.2 As these funds mature and 5-year track records become more plentiful, a key barrier to entry (strategy due diligence) will be removed for many investors.

Growth of Active Fixed Income ETFs

Why Active Fixed Income ETFs?

For active fixed income investors, ETFs offer multiple benefits when compared to mutual funds, including:

- Transparency: Traditional active ETFs adhere to prior-day holdings disclosure, making them fully transparent. Mutual funds commonly disclose their full portfolio holdings on a monthly or quarterly basis, usually published with a lag. The transparency of traditional active ETFs provides fixed income investors with greater clarity for due diligence and monitoring.

- Flexibility: ETFs offer intra-day trading as shares are bought and sold on exchanges at market prices throughout trading hours. Mutual fund investors, on the other hand, must buy and redeem shares at day-end net asset value. Active fixed income strategies in ETF wrappers offer investors more flexibility and greater support for different trading styles and habits.

- Tax efficiency: Whenever a redemption occurs, mutual funds must sell securities to raise cash, creating capital gains distributions for investors still holding the fund. ETFs operate differently: An ETF redemption triggers an in-kind exchange process that usually does not cause a taxable event for investors still in the fund. In recent years, an average of 27% of active fixed income mutual funds distributed capital gains, compared to just 18% of active fixed income ETFs.3

- Ease of access: ETFs have no minimum investment requirement (though they are subject to brokerage rules, costs, and fees). An investor can purchase as few as one ETF share or as many as preferred. While some mutual funds don’t have investment minimums, many may require investment minimums of $2,500 or more.

- Lower expense ratios: Both ETFs and mutual funds have an expense ratio, which includes management fees and the fund’s total annual operating expenses. Historically, active fixed income ETFs have had a lower gross average expense ratio of 0.49% while active fixed income mutual funds have had a higher gross average expense ratio of 0.83%.4

Active ETFs, like other active mandates in other wrappers, do have risks and may underperform their stated objective. As a result, it is important to follow a thorough due diligence process to assess whether an investment is right for your portfolio and is suitable for your risk tolerance – as well as if the strategy is delivering on its objective over an identifiable time period.

Originally Posted August 7th 2023, State Street Global Advisors

PHOTO CREDIT: https://www.shutterstock.com/g/SWKStock

Via SHUTTERSTOCK

Footnotes

1 Grinold, Richard C. 1989. “The Fundamental Law of Active Management.” The Journal of Portfolio Management, vol. 15, no 3. (Spring): 30-38.

2 Morningstar, as of April 30, 2023.

3 Morningstar, from December 31, 2016 to December 31, 2022. Calculations by SPDR Americas Research. Oldest share class of funds used.

4 Morningstar, as of May 25, 2023.

Disclosure

This communication is not intended to be an investment recommendation or investment advice and should not be relied upon as such.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

The views expressed in this material are the views of the SPDR ETF Strategy and Research team through the period ended July 26, 2023 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Investing involves risk including the risk of loss of principal.

Diversification does not ensure a profit or guarantee against loss.

Frequent trading of ETFs could significantly increase commissions and other costs such that they may offset any savings from low fees or costs.

Actively managed funds do not seek to replicate the performance of a specified index. An actively managed fund may underperform its benchmarks. An investment in the fund is not appropriate for all investors and is not intended to be a complete investment program. Investing in the fund involves risks, including the risk that investors may receive little or no return on the investment or that investors may lose part or even all of the investment.

Bonds generally present less short-term risk and volatility than stocks but contain interest rate risk (as interest rates rise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Investing in high yield fixed income securities, otherwise known as “junk bonds”, is considered speculative and involves greater risk of loss of principal and interest than investing in investment grade fixed income securities. These Lower-quality debt securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

{kind=link}