By: Kevin Flanagan, Head of fixed Income Strategy

Heading into October, the U.S. bond market was arguably already experiencing its worst year on record. Then, this month’s sell-off kicked in, bringing Treasury (UST) yields to levels not seen since 2007–08.

Think about that for a minute (perhaps even longer)…we’re talking about a period spanning roughly 15 years. In other words, there is a whole generation of investors who have never experienced UST yields at these elevated levels.

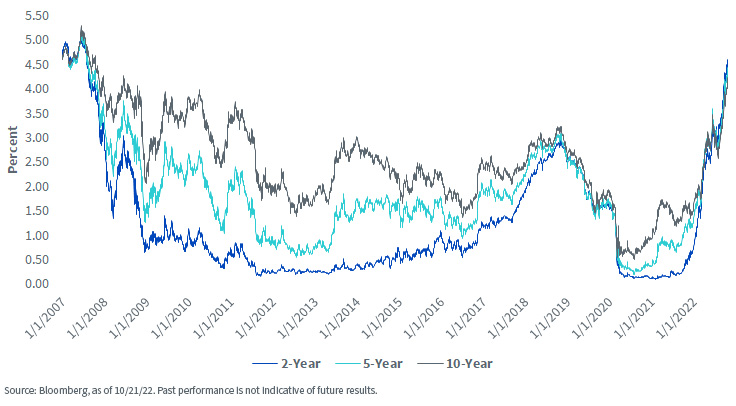

Let’s break it down a little bit. As I’ve noted in prior blogs, there has basically been no place to hide in the Treasury market this year. The only exception has been Treasury floating rate notes (FRNS), but more on that later. The rise in yields has been across the maturity spectrum, with the closely followed 2-, 5- and 10-year notes all experiencing surging yields thus far in 2022.

U.S. Treasury Yields

As of this writing, ‘4%’ handles in terms of yield are now widespread along the fixed coupon curve. As recently as early this year, those UST 2-, 5- and 10-year yields were trading from as low as 0.75% to about 1.65%. Unfortunately, the Fed’s use of ‘zero-interest rate policy,’ or ZIRP, following the financial crisis, and again to offset the adverse effects of the COVID lockdown in 2020, created an environment where investors had become quite accustomed to historically low rates, going so far as to think this was the ‘new normal.’

For us more ‘seasoned’ bond market veterans, this was always a conundrum of sorts. We remembered quite vividly where bond market yields resided before ZIRP, and always wondered when the ‘good ole days’ would return. Well, here they are! I argue that the historically low yield levels that were registered for the last 10 to 15 years were not normal, and that what investors are experiencing now is a better representation of where Treasury yields should probably be in the new era of inflation and the Fed’s attendant monetary policy response.

Conclusion

So, is there more to come? In other words, can UST yields continue rising from here? Let’s put the answer in the context of future Fed policy. Last week, Fed Funds Futures touched the 5% threshold as the terminal rate for the trading range by June of next year. If this level does come to fruition, we believe that Treasury yields will more than likely continue to rise, especially along the front end of the curve, as yields need to adjust to this potentially higher Fed Funds Rate.

This is where UST FRNs come into play, as this vehicle is designed to ‘float’ higher with the Fed, due to the resetting mechanism being tied to the weekly UST 3-month t-bill auction.

Looking ahead, these higher Treasury yields, both currently and in 2023, are creating a scenario in fixed income that investors have not been presented with for a decade and a half. As a result, opportunity could be knocking on the door for bond investors in 2023.

A version of this article was originally posted on October 26th, 2022 on the WisdomTree Blog.

PHOTO CREDIT: https://www.shutterstock.com/g/bpperry

Via SHUTTERSTOCK

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. The issuance of floating rate notes by the U.S. Treasury is new and the amount of supply will be limited. Fixed income securities will normally decline in value as interest rates rise.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa. This effect is usually more pronounced for longer-term securities.) Fixed income securities also carry inflation risk, liquidity risk, call risk, and credit and default risks for both issuers and counterparties. Unlike individual bonds, most bond funds do not have a maturity date, so holding them until maturity to avoid losses caused by price volatility is not possible. Any fixed income security sold or redeemed prior to maturity may be subject to loss.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

{kind=link}