By: Simona M Mocuta (Chief Economist), Elliot Hentov, Ph.D. (Head of Macro Policy Research), Vladimir Gorshkov, CFA (Macro Policy Strategist), Amy Le, CFA (Investment Strategist) and Venkata Vamsea Krishna Bhimavarapu (Economist)

As global macro trends of slowdown and disinflation persist, recent developments validate forecasts of substantial rate cuts. With the US Fed initiating its easing cycle, we anticipate clearer policy direction as elections approach in November.

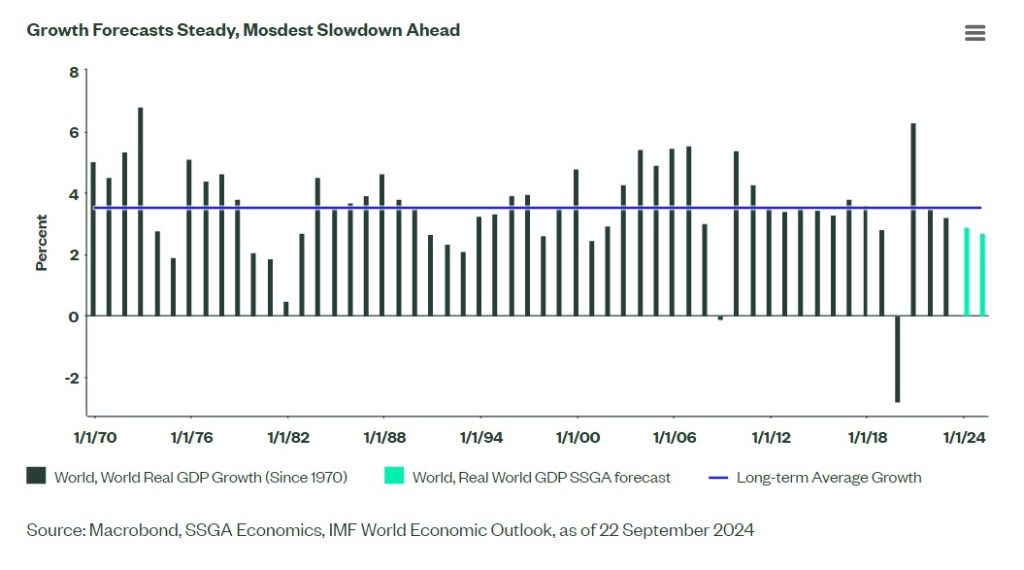

For more than a year, we’ve been discussing two main global macro trends: slowdown and disinflation. We also argued that as those trends took visible hold, the next chapter in the global macro narrative would involve broad and substantial rate cuts. This was to be an exercise of calibrating policy rates lower in light of improving inflation dynamics, rather than any sort of panic-driven rush to cut rates to prevent a recession.

Several months ago, the US appeared to temporarily depart from the broad trend of disinflation and rate cuts. However, as we wrote in our June update “US inflationary pressures are increasingly narrow and, given the normalizing labor market and anchored inflation expectations, the disinflation process is set to resume.” We also forecast that “the Fed will joins the easing cycle later in the year and quickens it in 2025. The “different speeds, same direction” mantra we applied to global disinflation in 2023 applies to global policy easing in 2024-25.” It is good to see those views validated by recent developments as the Fed kickstarted its own easing cycle with a 50 basis point rate cut in September.

For the second quarter in a row, global forecasts are almost unchanged. This may seem at odds with considerable market volatility—we indeed experienced a fairly acute volatility episode in early August—but that simply speaks to lack of conviction on timing given contradictory data than on the direction of travel per se. If we are to count any surprises in the intervening period, we’d probably point to the steady retreat in oil prices, which has helped offset concerns around rising shipping costs. It also seems to consolidate perceptions of weak demand out of China. We have not changed our China growth forecasts, but we were already below consensus both for this year and next and remain so.

Elections remain a key source of uncertainty. With the US heading to the polls in early November, we should have a better sense of policy direction in our next update.

This post first appeared on September 23rd, 2024 on the State Street Global Advisors blog

PHOTO CREDIT: https://www.shutterstock.com/g/normaals

VIA SHUTTERSTOCK

DISCLOSURES:

State Street Global Advisors Worldwide Entities

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the applicable regional regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator”) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

The views expressed in this material are the views of SSGA Economics Team through the period ended September 20, 2024 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

{kind=link}