by Elena Philipova, director of sustainable finance at the London Stock Exchange Group (LSEG)

Asset managers can contribute most to a sustainable economy by sticking to a policy of steadily reducing their portfolios’ carbon emissions.

Climate change urgency

The November 2021 climate change summit in Glasgow (COP26) brought home the urgency of addressing global warming.

COP26 participants said that limiting warming to 1.5°C by 2050 requires rapid, deep and sustained reductions in global greenhouse gas emissions.

These include a cut in CO2 emissions of 45 percent by 2030 relative to the 2010 level, and to net-zero by mid-century.

The COP26 alarm bells are sounding even louder six months on from the Glasgow conference.

Researchers at the UK’s Met Office said this month that there’s now around a fifty-fifty chance that the world will warm by more than 1.5C in the next five years.

And it’s almost certain that 2022-2026 will see a new record warmest year, they say.

Asset owners, asset managers and greenwashing concerns

Asset managers have a big say in our response to this alarming forecast.

Via the investment products they develop and distribute, they help direct long-term savings towards more sustainable businesses and activities.

Asset managers also sit downstream from the institutional owners of large savings pools, who are becoming increasingly vocal about their climate change objectives.

The Net Zero Asset Owners Alliance (NZAOA), which controls an aggregate $10.4trn in assets, has recently said it wants to work more closely with asset managers, saying it wants to make sure both groups’ stewardship activities and public messaging are aligned.

Does this statement hint at a previous lack of focus in the asset management community? Possibly.

Undoubtedly, some asset managers have in the past struggled to define and label their environmental, social and governance-focused (ESG) investment products.

This derives from the fact that, when it comes to sustainable investing, there are no industry-wide definitions, standards and transparency requirements.

Getting the design of ESG products wrong is not just a matter of a lack of impact. It carries severe reputational—and even financial—risks for the firms concerned.

Around half of UK financial advisers surveyed late last year said that asset managers should face fines for so-called “greenwashing”—providing misleading information about their green credentials to bolster their reputation and increase fund sales.

Don’t overcomplicate climate change

Asset managers can best address these concerns by sticking to their decarbonisation goals. It’s not necessary to overcomplicate climate change, as financial markets have perhaps tended to do in the past.

And the most effective way to measure investors’ impact on the climate and their progress towards a net zero goal is to track their portfolio emissions.

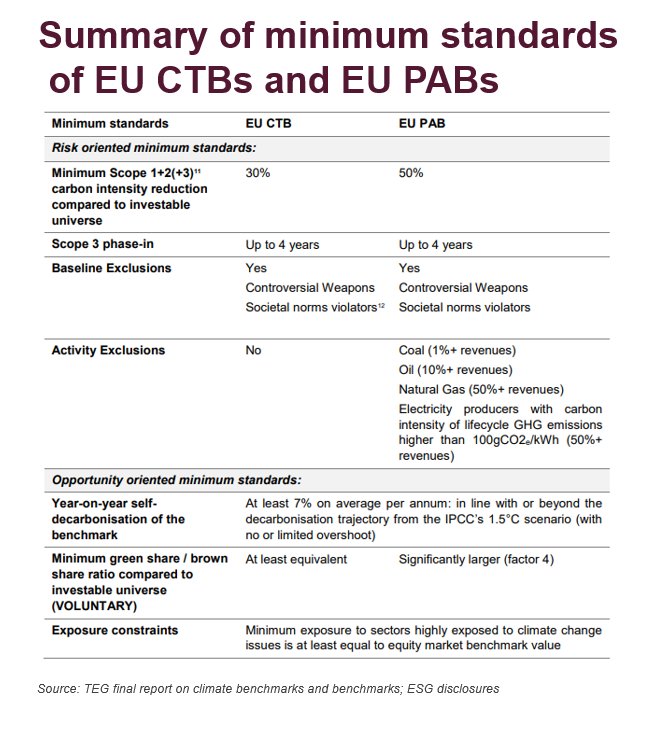

Regulations are already pushing asset managers in this direction. For example, climate benchmarks are playing an increasingly important role in policymaking.

In 2020, the European Commission set out minimum standards for the so-called Paris-Aligned and Climate Transition benchmarks.

Paris-Aligned benchmarks set a goal of a 50 percent reduction in carbon emissions, with a minimum year-on-year decarbonisation rate of 7 percent. Climate Transition benchmarks decarbonise at the same pace but with a lower eventual emissions reduction target.

FTSE Russell has developed a Paris-aligned version of its flagship FTSE All-World index, which excludes companies producing high emissions or involved in controversial activities, as well as boosting green revenues and incentivising better corporate management.

Summary of minimum standards of EU CTBs and EU PABs

Source: TEG final report on climate benchmarks and benchmarks; ESG disclosures

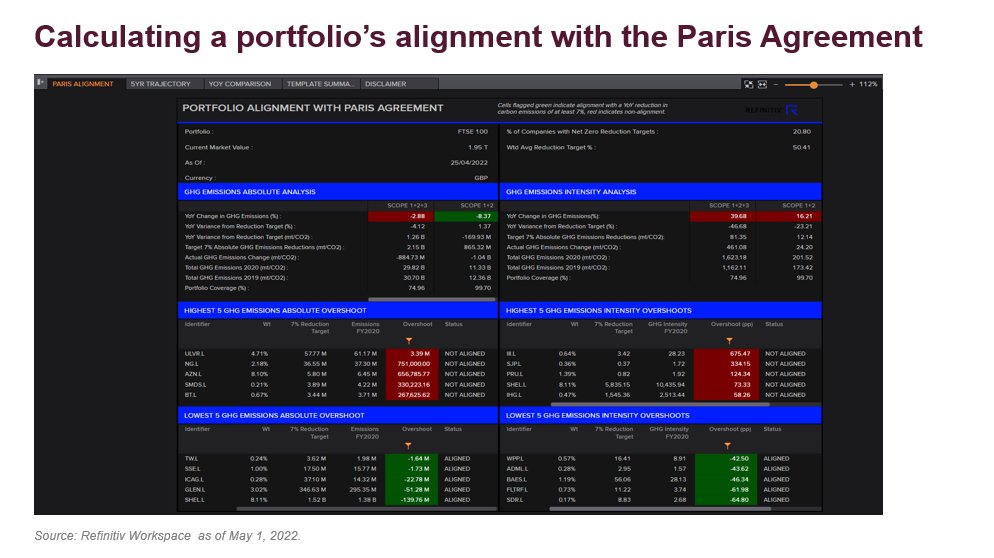

Asset managers can also now access more sophisticated portfolio decarbonisation tools.

For example, the Carbon Footprint template, available in Refinitiv Eikon’s Portfolio Analytics app, helps asset managers calculate the carbon exposure of a portfolio and to report the associated data.

The template offers a weighted view of carbon emission exposures, allowing investors to quickly identify which companies in the portfolio have the greatest intensity of carbon emissions—both reported and estimated.

We need step-by-step change

In addressing climate change, long-term goals are important. But just as we can individually make small contributions to sustainability by modifying our consumption patterns, reducing our use of plastics and recycling what we can, a step-by-step change that will have the most effect in the battle with global warming.

This is particularly true, given that there’s recently been disagreement about science-based climate change targets and the methodologies used to reach them. Unfortunately, using the language of commitments to show we’re making a difference can also be used as an excuse to delay action.

So let’s stick to evidence-based methods. And taking actions today, with an impact on the existing real economy, is what we should all be trying to do.

This post first appeared on May 23rd, 2022 on the FTSE Russell Blog

PHOTO CREDIT: https://www.shutterstock.com/g/Sepp+photography

Via SHUTTERSTOCK

© 2022 London Stock Exchange Group plc and its applicable group undertakings (the “LSE Group”). The LSE Group includes (1) FTSE International Limited (“FTSE”), (2) Frank Russell Company (“Russell”), (3) FTSE Global Debt Capital Markets Inc. and FTSE Global Debt Capital Markets Limited (together, “FTSE Canada”), (4) FTSE Fixed Income Europe Limited (“FTSE FI Europe”), (5) FTSE Fixed Income LLC (“FTSE FI”), (6) The Yield Book Inc (“YB”) and (7) Beyond Ratings S.A.S. (“BR”). All rights reserved.

FTSE Russell® is a trading name of FTSE, Russell, FTSE Canada, FTSE FI, FTSE FI Europe, YB and BR. “FTSE®”, “Russell®”, “FTSE Russell®”, “FTSE4Good®”, “ICB®”, “The Yield Book®”, “Beyond Ratings®” and all other trademarks and service marks used herein (whether registered or unregistered) are trademarks and/or service marks owned or licensed by the applicable member of the LSE Group or their respective licensors and are owned, or used under license, by FTSE, Russell, FTSE Canada, FTSE FI, FTSE FI Europe, YB or BR. FTSE International Limited is authorized and regulated by the Financial Conduct Authority as a benchmark administrator.

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products, including but not limited to indexes, data and analytics, or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put. Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance.

No responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any error (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analyzing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of the LSE Group is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing in this document should be taken as constituting financial or investment advice. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any representation regarding the advisability of investing in any asset or whether such investment creates any legal or compliance risks for the investor. A decision to invest in any such asset should not be made in reliance on any information herein. Indexes cannot be invested in directly. Inclusion of an asset in an index is not a recommendation to buy, sell or hold that asset nor confirmation that any particular investor may lawfully buy, sell or hold the asset or an index containing the asset. The general information contained in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index inception date is back-tested performance. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. However, back-tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index.

This document may contain forward-looking assessments. These are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. No member of the LSE Group nor their licensors assume any duty to and do not undertake to update forward-looking assessments.

No part of this information may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permission of the applicable member of the LSE Group. Use and distribution of the LSE Group data requires a license from FTSE, Russell, FTSE Canada, FTSE FI, FTSE FI Europe, YB, BR and/or their respective licensors. The FTSE All-Share Paris-aligned (PAB) Index is designed to support investors seeking to integrate climate risks and opportunities into their portfolios and align them with the climate goals of the Paris Agreement. You cannot invest directly in an index.