By Philip Lawlor, head of Global Investment Research

Booming commodity prices and the surprisingly robust US CPI reading for April have cranked up market anxieties that the Federal Reserve might be forced to change guidance on QE tapering sooner rather than later. The inflation wild card is likely to keep markets volatile in the months ahead.

US inflation heats up

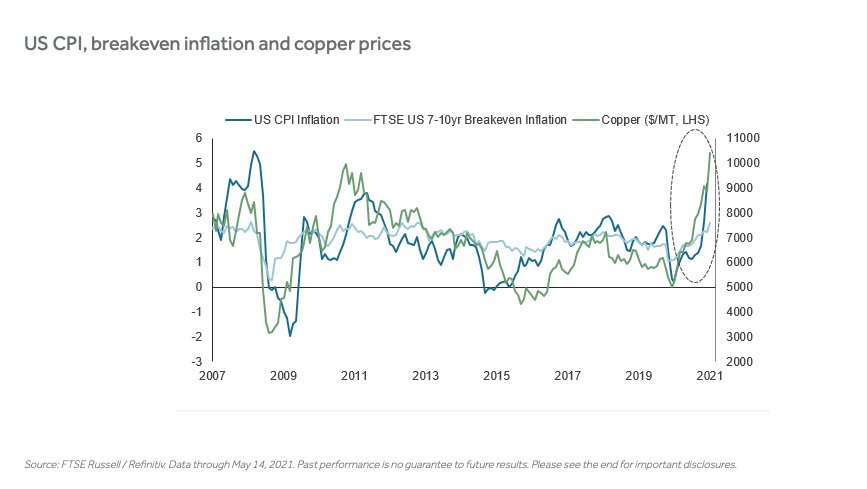

The quickening pace of the US reopening has already prompted a rash of upgrades to 2021 GDP forecasts, including those of the Fed (from 4.2% at year-end 2020 to 6.5% currently). While market-implied inflation expectations have risen globally, they are at decade highs for the US, as shown below. The year-on-year surge in April CPI (the strongest since 2008) and surging commodity prices have all added fuel to the inflation-fear fires.

What the Fed is watching

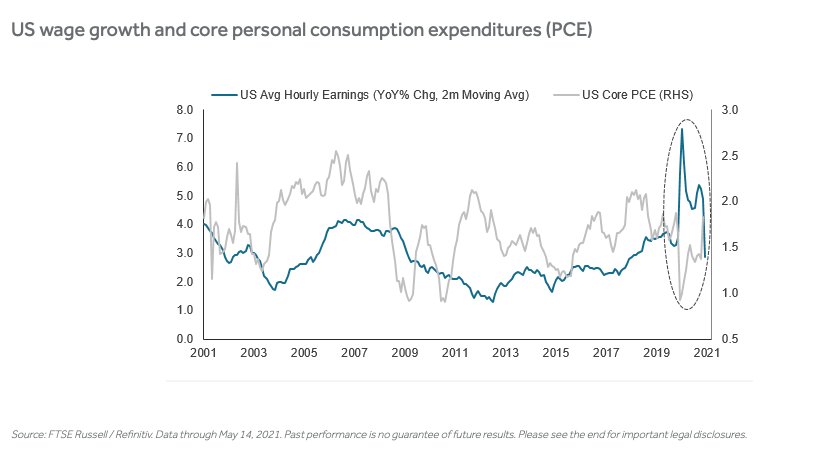

But the Fed is showing no signs of budging from its current stance. Officials have been adamant in their commitment to the new, more patient policy framework, which puts a keener focus on achieving employment goals than previous regimes. They also continue to expect reopening price pressures to level off as shipping and supply pathways clear and demand normalizes. The Fed’s preferred metric – core personal consumption expenditures (PCE) – is still below target and historically low, while the April figures for jobs and wage growth were also more muted than expected.

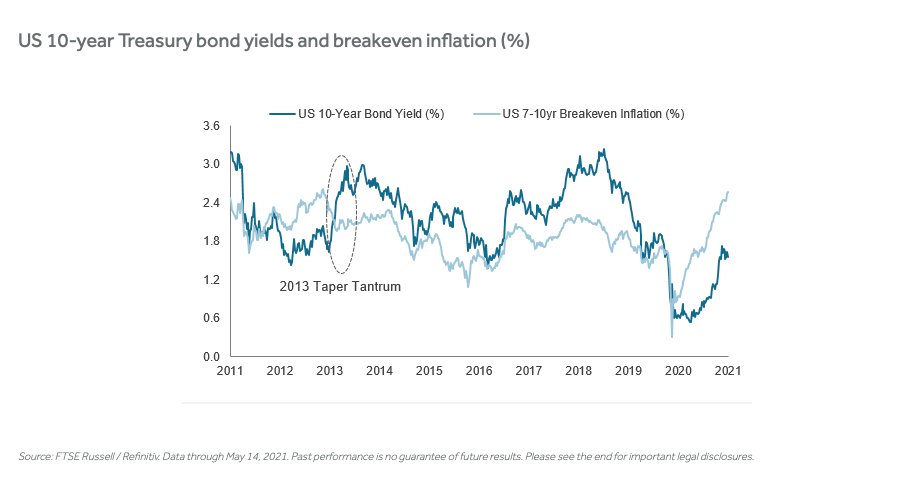

But financial markets continue to test the Fed’s dovish policy resolve. The US bond market has already undergone a jarring repricing of inflation risk this year, which catapulted the 10-year Treasury yield more than 80 basis points to a high of 1.73% in mid-March.

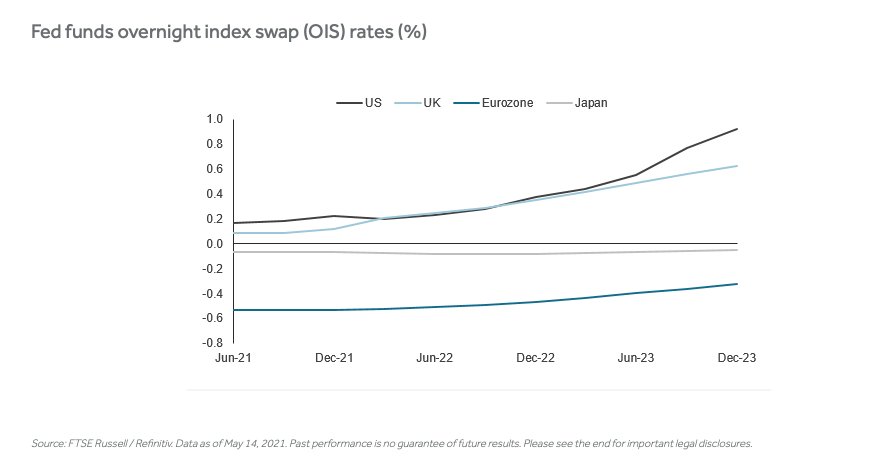

Futures markets foresee the Fed and Bank of England making their first rate hikes in mid-2022 ‒ well ahead of other central banks and their own official timelines ‒ and a steeper trajectory for US rates thereafter.

Will the Jackson Hole summit bring answers?

Base effects, pandemic-induced supply disruptions and a long history of false dawns are muddying the long-term inflation outlook. It may be months before a clear picture of the underlying inflation trend emerges. That said, however, the sequence and timing of Fed moves following the 2013 Taper Tantrum may offer some perspective.

The 2013 Taper Tantrum was triggered by the mere hint of an approaching Fed policy shift. The Fed did not begin winding down its asset purchases until late 2014, and the first rate hike was in December 2015. As shown below, long Treasury yields and inflation breakevens fell steadily over that 30-month period before climbing again with the official tightening regime.

Whether the leap in inflation proves temporary or longer lasting (i.e., hot enough to force a shift in Fed guidance) is likely to remain a heated debate for months to come, amplifying the focus on US jobs, wages and inflation releases. More clarity could come this August, when the world’s central bankers meet at their annual Jackson Hole symposium, an occasion that officials often use to make important pronouncements about policy and shifts in thinking.

This post first appeared on May 19 on the FTSE Russell blog.

Photo Credit: Paul VanDerWerf via Flickr Creative Commons

© 2021 London Stock Exchange Group plc and its applicable group undertakings (the “LSE Group”). The LSE Group includes (1) FTSE International Limited (“FTSE”), (2) Frank Russell Company (“Russell”), (3) FTSE Global Debt Capital Markets Inc. and FTSE Global Debt Capital Markets Limited (together, “FTSE Canada”), (4) MTSNext Limited (“MTSNext”), (5) Mergent, Inc. (“Mergent”), (6) FTSE Fixed Income LLC (“FTSE FI”), (7) The Yield Book Inc (“YB”) and (8) Beyond Ratings S.A.S. (“BR”). All rights reserved.

FTSE Russell® is a trading name of FTSE, Russell, FTSE Canada, MTSNext, Mergent, FTSE FI, YB and BR. “FTSE®”, “Russell®”, “FTSE Russell®”, “MTS®”, “FTSE4Good®”, “ICB®”, “Mergent®”, “The Yield Book®”, “Beyond Ratings®” and all other trademarks and service marks used herein (whether registered or unregistered) are trademarks and/or service marks owned or licensed by the applicable member of the LSE Group or their respective licensors and are owned, or used under licence, by FTSE, Russell, MTSNext, FTSE Canada, Mergent, FTSE FI, YB or BR. FTSE International Limited is authorised and regulated by the Financial Conduct Authority as a benchmark administrator.

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products, including but not limited to indexes, data and analytics, or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put. Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance.

No responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any error (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analysing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of the LSE Group is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing contained in this document or accessible through FTSE Russell Indexes, including statistical data and industry reports, should be taken as constituting financial or investment advice or a financial promotion.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index inception date is back-tested performance. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. However, back- tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index.

This publication may contain forward-looking assessments. These are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. No member of the LSE Group nor their licensors assume any duty to and do not undertake to update forward-looking assessments.

No part of this information may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permission of the applicable member of the LSE Group. Use and distribution of the LSE Group data requires a licence from FTSE, Russell, FTSE Canada, MTSNext, Mergent, FTSE FI, YB and/or their respective licensors.