By George Milling-Stanley, Chief Gold Strategist, State Street Global Advisors

This post was written with contributions from the SPDR® Gold Strategy Team: Maxwell Gold, CFA, Head of Gold Strategy and Diego Andrade, Senior Gold Strategist.

Back in December, in the pre-COVID-19 era, I offered my thoughts on the likely trading range for the gold price in 2020.1 I developed the customary three hypothetical scenarios — a bear case, a base case, and a bull case — and I outlined what I thought would need to happen for each to develop. The pandemic has brought major changes to just about all aspects of human life, and the gold market has certainly not been immune to the impact of COVID-19. I commented on some of the changes we have seen year to date, including: gold’s behavior during Q1 market volatility,2 as well as the initial impact of COVID-19 on gold demand.3 As we pass the halfway mark of 2020, I have updated my outlook for the remainder of the year across three new scenarios and the factors that seem most likely to drive gold prices.

Remember, these suggested hypothetical prices represent possible trading ranges, not forecasts for year-end prices.

SCENARIO 1: THE BEAR CASE: $1,700 to $1,900.

What needs to happen for the bear scenario? This hypothetical scenario assumes a moderate level of success in reopening economies around the world, which can be expected to reduce investment and perceived “safe-haven”4 demand for gold. Progress is gradual, however, and jewelry demand remains depressed, especially in the emerging markets. With economic recovery on the horizon, EM central banks may slow their move away from US dollar instruments and reduce their purchases of gold for official reserves.

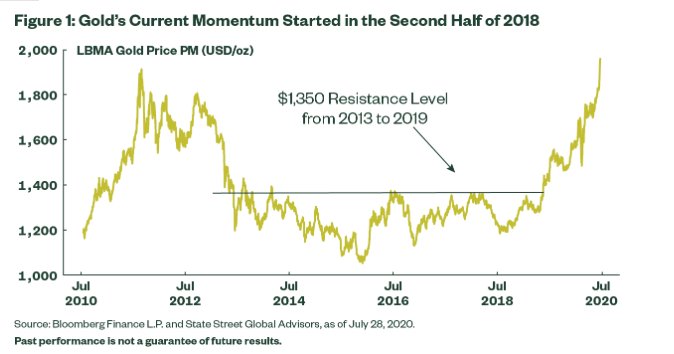

In this case, gold declines from present levels as investment and perceived safe-haven buying fall dramatically, but the downside remains limited to the lower bound of the suggested range due to the potential inflationary impact of the huge stimulus measures taken around the world. In addition, even before the advent of the pandemic, gold had already climbed $250 above the high point of the trading range that had been in place for six years from June 2013 to June 2019. And the concerns that drove that rally, including the threat of escalating trade wars, have not entirely dissipated.

Macroeconomics: US equities move up dramatically on the prospect of a return to something approaching normalcy, and domestic bond yields gradually edge toward positive territory as foreign investors move capital into US equities – a move that may bring a stronger US dollar. The US economy may rally more swiftly than expected, producing a V-shaped recovery.

Geopolitics: There is a possibility that the atmosphere of political divisiveness in the US may recede, with the presidential election proceeding calmly, combined with a new atmosphere of bipartisanship. The US may succeed in extricating itself from all of its entanglements in the Middle East and Afghanistan, the situation on the Korean Peninsula could begin to improve, and the Brexit issue may be resolved quickly, with no damage to the economic situation in the UK, Europe, or the world.

Key drivers: The key drivers of the gold price in this hypothetical Bear Case would be the slow pace of global economic recovery, especially in the emerging world, implying no increase in jewelry demand. Under this scenario, the prospect of a return to a more normal situation could seriously damage perceived safe-haven and investment demand, while a slow recovery could be expected to limit gold jewelry demand, resulting in weak overall global gold demand.

SCENARIO 2: THE BASE CASE: $1,800 to $2,000.

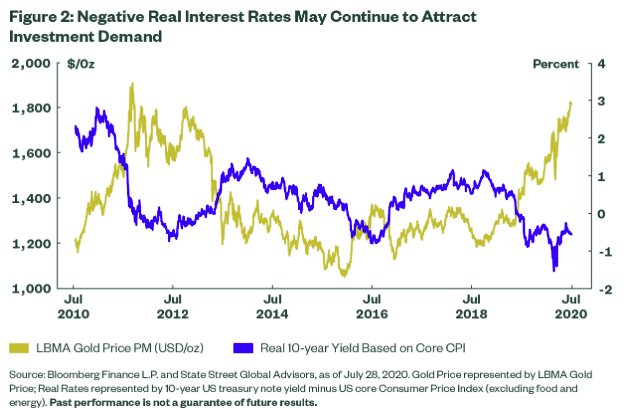

What needs to happen for the base scenario? This hypothetical scenario assumes no improvement in the economic situation in emerging markets, so jewelry demand remains depressed, although there may be some seasonal improvement toward the end of the year. Currencies in the region remain weak, which could potentially be supportive of investment demand. Emerging market central banks may continue to buy gold for their official reserves in quantities accounting for around 10% of total global gold demand, which has been the average over the past decade.5 Globally, jewelry demand remains at H1 depressed levels, but investment demand continues strong and compensates for the lack of growth in jewelry. Real interest rates remain at, or close to, historic lows.

Macroeconomics: The US dollar may remain steady even in the face of a rising deficit, and the Fed stays on hold with rates close to zero. Perceived safe-haven appeal continues to provide support for the US dollar in the short term. Global bond yields could remain predominantly negative. US equities may continue to stabilize after the violent gyrations during the first quarter of the year, with no significant moves in either direction. The gradual reopening of the economy may continue to be patchy across the US, but most of the country manages to avoid a second wave of infections, and there is no need for an additional round of nationwide lockdowns. Economic recovery in the US assumes more of a U-shape.

Geopolitics: There are incipient signs of a less partisan tone in US politics, and the November presidential election proves no more contentious than most people expected. The tenor of discourse among Senate and House incumbents and new lawmakers may become more about seeking unity than division, with promises by both sides of the political aisle to take steps toward working together after the election. This scenario envisages some signs that the US may be able to reduce its involvement in the Middle East and Afghanistan. The issue of Brexit may gradually be resolved without significant weakness in European economies, and no major adverse impact on the global economy.

Key drivers: The key drivers of the gold price in this hypothetical Base Case would be the absence of economic recovery in the emerging world, a less partisan tone in US politics, and no significant changes in US financial market conditions.

SCENARIO 3: THE BULL CASE: $2,000 to $2,200. What needs to happen for the bull scenario? This hypothetical scenario assumes a swift and successful economic reopening in emerging markets, triggering a strong rebound in jewelry demand in the region, but continued difficulties in reopening in the industrialized world, with the result that perceived safe-haven and investment demand would remain strong. Debt levels in the US have risen dramatically as the Treasury and the Fed have sought to mitigate the impact of the pandemic, so the US dollar may weaken further. This, coupled with growing concerns about the potential for inflation as a result of the unconventional measures, could provide ongoing support for investment and perceived safe-haven demand in the US. In the face of growing uncertainty about the outlook for the US dollar, emerging market central banks may increase their purchases of gold for official reserves.

Macroeconomics: The US dollar has already begun to lose momentum, as its yield advantage over the G-10 countries has shrunk from a high of 2% in mid-March to zero following the emergency rate cuts that dropped the Fed funds rate to a range of 0.00 to 0.25. Further dollar weakness may be possible, as the Fed chair promises to do “whatever it takes for as long as it takes” to help the US markets. Equities in the US may move higher, but investors could remain cautious and risk-averse in the face of negative real rates and steeply rising debt levels.

Geopolitics: The November elections in the US may become uglier and more contentious, and there remains the possibility of continued gridlock in Washington. Geopolitical tensions continue to escalate all over the world, and there is already talk of a new cold war, this time between the US and China. COVID-19 has delayed attempts to extricate the US from military engagement in the Middle East and elsewhere, and it may prove impossible to disengage in the foreseeable future. Brexit may turn out to have damaging implications not just for the UK and Europe, but also for the global economy.

Key drivers: The key drivers of the gold price in this hypothetical Bull Case would be continued strong investment demand, combined with a recovery in jewelry. Emerging market central banks may accelerate their purchases of gold for official reserves.

To read the rest of this outlook on gold, please go here.

Photo Credit: Susanne Nilsson via Flick Creative Commons

Footnotes

1 Gold Nuggets: The 2020 Outlook

2 Gold Nuggets: Upending Conventional Wisdom

3 Gold Nuggets: COVID-19 Changes the Landscape of Gold Demand

4 Assets may be considered “safe havens” based on investor perception that an asset’s value will hold steady or climb even as the value of other investments drops during times of economic stress. Perceived safe-haven assets are not guaranteed to maintain value at any time.

5 Source: World Gold Council Gold Demand Trends Q2 2020, as of July 30, 2020.

Disclosure

Commodity funds may be subject to greater volatility than investments in traditional securities. Investments in commodities may be affected by overall market movements, changes in interest rates, and other factors, such as weather, disease, embargoes, and international economic and political developments.This material is for your private information. The views expressed are the views of the SPDR® Gold Strategy Team and are subject to change based on market and other conditions. The opinions expressed may differ from those with different investment philosophies. Investing involves risk including the risk of loss of principal.

Certain of the information contained in this presentation is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. SPDR Gold Strategy Team believes that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions