By Maxwell Gold, CFA, Head of Gold Strategy

This post was written with contributions from the SPDR Gold Strategy Team: George Milling-Stanley, Chief Gold Strategist, and Diego Andrade, Senior Gold Strategist.

Tremendous effort has been put forth by global monetary and fiscal policymakers to help stabilize markets and economies during the COVID-19 crisis. The playbook for this crisis appears remarkably similar to the one that was used during the 2008 financial crisis – with staggering amounts of debt, liquidity, and deficit spending being deployed. Simultaneously, gold has experienced an impressive rise in price – and investment demand – despite its recently weaker jewelry demand.1

Making sense of the initial COVID-Related impact on gold

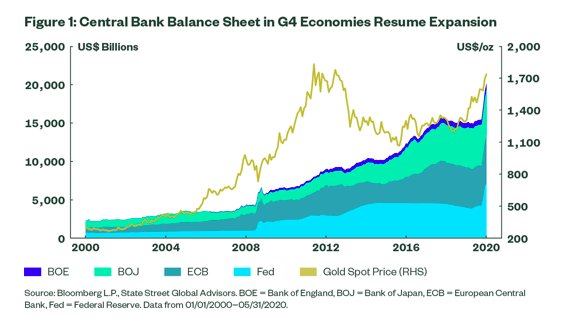

Gold’s price movement and the catalyst behind rising investor interest in gold was initially driven by the extreme market volatility in Q1,2 illustrating gold’s historical “flight-to-safety” advances during absolute market dislocations. Since then, investor focus has turned to the potential longer-term consequences of these monetary and fiscal decisions. At a high level, many of these actions may stand to benefit the outlook for gold. While gold has broadly tracked rising central bank balance sheet levels over the past two decades, gold investors should focus on the impact these debt levels may have alongside rising deficits and low rate policies on the US dollar (USD), and in turn the potential advantage for gold.

One of the most notable actions taken by central banks has been the significant expansion of their balance sheets through debt and other asset purchases to spur market liquidity. G4 central banks alone have seen a 31% year–to-date increase of their balance sheets to $20 trillion as of May 31, 2020.

The long arm of inflation: The US dollar and gold

Many have called for the return of inflation as a result of these rising debt levels and increase of “money printing” by central bankers. But sparking inflation through accommodative monetary policies has proven to be a true Sisyphus-like dilemma for policymakers in the past, as they’ve unsuccessfully tried to push the inflation boulder uphill over the past decade – primarily due to a drop in the velocity of money. Additionally, with the continued structural deflationary headwinds of aging global demographics, rising impact of technology, and the now inevitable deleveraging cycle, inflation in the form of traditional price measures will likely remain tame.

Instead, inflation may emerge in the form of currency devaluation, particularly with the US dollar, as a result of continued accommodative policies. A weaker dollar is inherently an inflationary action because it reduces the purchasing power of US consumers and investors. Monetary and fiscal policies geared toward a weaker dollar could greatly aid in reducing debt burdens through this inflationary effect – with a weaker dollar supporting growth through exports and reducing nominal values of debt outstanding.

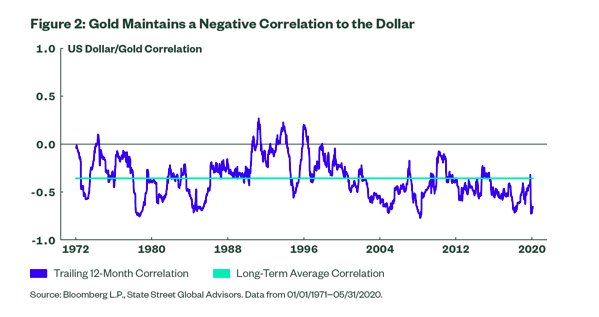

This environment could prove powerful for gold – which may provide the role of a store of value by keeping up with broad price fluctuations in conjunction with weakening currencies. An outlook for a weaker USD environment is a good sign for gold which holds an average correlation of -0.36 to the USD since 1971 and a current 12-month correlation of -0.65 (as of May 31, 2020). But it is not always a straight line with gold and the USD. Gold and the USD have also exhibited brief periods of synchronization and even positive correlations in the short run. This can typically occur during outlook extremes – with gold and the dollar being sought with flight-to-quality motives during extreme downturns. Positive correlation has also been supported during periods when higher cyclical demand for gold jewelry and technology rose with extreme increases in real GDP alongside rising demand for dollars to invest.

What’s bad for the US dollar may be good for gold

Heading into 2H 2020, a significant jump in volatility – or severe risk-off sentiment – could see USD support in the short term. But there are several reasons to expect the USD remains softer over the medium to longer term – an outcome that potentially supports continued gold demand and price outlook.

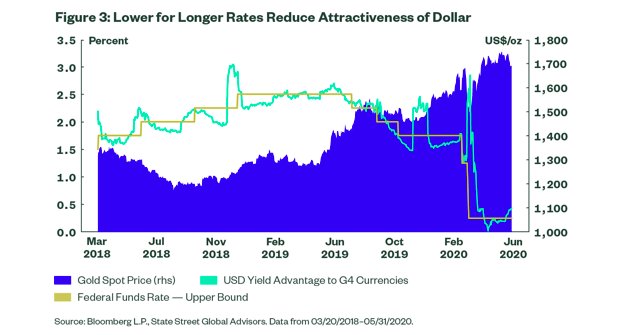

The gold price continues to receive support from “lower-for-longer” interest rates in the US. In March, the Fed did not waste time cutting its reference Fed funds rate by 150 basis points to near zero – a level not seen since 2015. This drop in its key benchmark rate greatly reduced the relative attractiveness of the USD to other major currencies globally while further lowering gold’s opportunity cost.3 With US rates likely to remain suppressed due to the trifecta of rising debt levels, rising unemployment, and recession fears – the yield advantage of the USD may languish, thereby lowering demand and activity from a carry trade perspective.

Recent US fiscal deficit spending ($2.2 trillion to date with the potential for more to come) may create a second headwind for the dollar’s outlook in the medium term. The US budget deficit is estimated to be 9% of gross domestic product (GDP), the largest it’s been since 2010.4 Dealing with an elevated deficit will weigh on the economic outlook as the US spends more to service its outstanding debt, potentially reducing real GDP. Lower growth, in turn, fuels the case to maintain lower rates, resulting in a headwind for USD prospects (based on interest rate differentials) and providing further tailwinds for gold.

The COVID reset: What gold may gain from the bending walls of the dollar

When evaluating the USD on a relative valuation basis, the currency may appear overvalued. Applying an intrinsic measure to the value of the US dollar (USD in gold terms, or “how much gold can $1 purchase”) to a more nominal measure (USD in other currency terms, or the trade-weighted dollar5 ) highlights a clear bifurcation.

To read the rest of this round table interview that first appeared on the SPDR blog on June 19, please click here.

Photo Credit: K.Hurley via Flickr Creative Commons

Footnotes

1 Gold Nuggets: COVID-19 Changes the Landscape of Gold Demand

2 Gold Nuggets: Upending Conventional Wisdom

3 Gold’s Opportunity Cost Becomes Opportunity Benefit

4 Source: Bloomberg L.P., Data as of June 9, 2020.

5 Trade-weighted broad dollar index: A weighted average of the foreign exchange value of the U.S. dollar against the currencies of a broad group of major U.S. trading partners, a subset of advanced foreign economies, and a subset of emerging market economies respectively–using weights based only on trade in goods.

6 Mean reversion is a theory used in finance that suggests that asset prices and historical returns eventually will revert to the long-run mean or average level of the entire dataset

Disclosure

Commodity funds may be subject to greater volatility than investments in traditional securities. Investments in commodities may be affected by overall market movements, changes in interest rates, and other factors, such as weather, disease, embargoes, and international economic and political developments.

This material is for your private information. The views expressed are the views the SPDR® Gold Strategy Team and are subject to change based on market and other conditions. The opinions expressed may differ from those with different investment philosophies.

This material is for informational purposes only and does not constitute investment or tax advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information.