It has been a tough year for investors in real estate investment trusts (REITs). The market’s obsession about when the U.S. Federal Reserve might start tapering its level of monthly bond purchases has hit the value of REITs, which some investors and analysts believe are very sensitive to interest rates.

But is that really supported by the data? A case can be made that REITs often do perform well in times of rising interest rates. What’s more, other factors—property market fundamentals, economic growth and strong liquidity—can often trump adverse movements in interest rates.

There’s no denying that REIT exchange traded funds such as the Vanguard REIT Index (VNQ) and the SPDR Dow Jones REIT (RWR) have been hammered since May when the Fed first hinted that it may start to dial back on its $85 billion in monthly bond prices, which could place upward pressure on rates.

In theory, higher rates are bad for REITs because debt-servicing costs rise on properties and there’s less free cash to invest. In October, John Gerard Lewis, who runs the Covestor Stable High Yield portfolio, sold off all of his holdings of mortgage real estate investment trusts (mREITs). As he explained at the time:

In light of the Fed’s mid-summer suggestion that its bond-buying program could start to wind down in September, a certain amount of volatility was removed from the portfolio by selling all holdings of mortgage real estate investment trusts (mREITs). The mREIT allocation had been particularly damaged by the rise in rates and the Fed’s indication that tapering of its bond buying would soon occur.

Goldman Sachs recently issued a sell rating on two big agency mortgage REITs, Annaly Capital Management (NLY) and American Capital Agency Corp. (AGNC). “While agency mortgage REITs have already significantly underperformed the market this year… we think investors and sell-side analysts have been slow to realize the downside potential,” according to the Goldman report which was excerpted by Michael Aneiro at Barron’s.

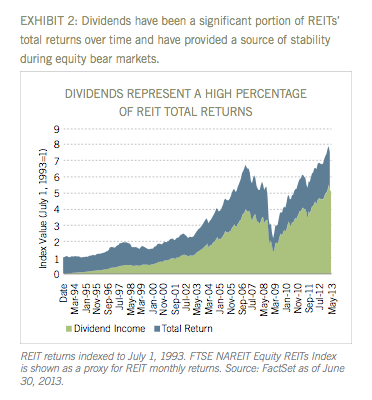

So why would anyone go near REITs in 2014? This year aside, REITs do have a decent long-term track record of performance. Publicly traded equity REITs, over a three decade stretch through March 28, 2013, outperformed the S&P 500 (SPX), Dow Jones Industrials (DJIA) and NASDAQ Composite (NDX), according to data compiled by the National Association of Real Estate Investment Trusts.

In September, Fidelity Investments sent a research note to clients pointing out the diversification benefits of REITs in an investment portfolio and suggesting investors think about more exposure to “commercial property through REIT stocks, particularly in multi-asset-class portfolios.”

Why? During the past 20 years, an allocation to REIT stocks would have boosted the risk-adjusted returns of a portfolio including U.S. stocks and investment-grade bonds, according to Fidelity. Of course, REITs sold off hard with U.S. stocks and many other asset classes during the financial crisis.

Finally, Morningstar analyst Abby Woodham in a recent report analyzed past periods in which interest rates rose and the performance of this asset class. Aside from interest rates, REITs are tied to the overall health of the property market and U.S. economy.

Between June 2004 and August 2006, as the Fed raised rates, REITs advanced 65% vs. 21% for the S&P 500. “Higher rates were offset by the surging housing market and broad gains in the equity market at large,” wrote Woodham.

Photo Credit: ykanazawa1999

{kind=link}