Matthew J. Bartolini, CFA, Head of SPDR Americas Research, State Street Global Advisors

As investors scour the landscape for return-generating opportunities, being able to spot trends is a significant advantage. However, it’s not enough to simply spot overarching market shifts or dynamics.

True opportunity lies in using specialized, industry-specific knowledge to capitalize on market events, macro trends, and other changes.

As we enter the final quarter of 2019, we see three opportunities where we believe investors can benefit from tactical positioning in sector-based strategies.

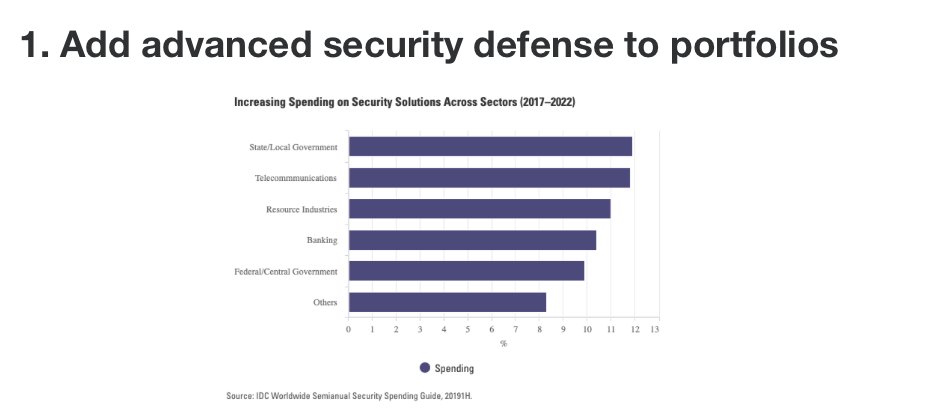

As businesses have become more dependent on the digital economy and the internet for their day-to-day operations and long-term growth, cyberattacks and data fraud or theft are now two of the top five risks CEOs are most likely to face.1

Global spending on information security is projected to grow at a compound annual growth rate of 9.2% between 2018 and 2022, reaching $133.8 billion.2

The nature of warfare and border security threats has also evolved, driving the increase in government spending on militarized AI and unmanned and autonomous capabilities to protect national security. Worldwide spending on militarized artificial intelligence (AI) is projected to rise to $118 billion by 2023.3

Firms specializing on the cutting edge of security in cyberspace and geospace may benefit from the increasing demand for security services and technology. Relative to a traditional aerospace and defense exposure, which is 100% allocated to industrial firms, the SPDR® S&P Kensho Future Security ETF (FITE) is 37% allocated to Software & Services firms and 18% allocated to technology hardware, better harnessing future developments in national and enterprise security.4

2. Capture the potential rebound in housing markets

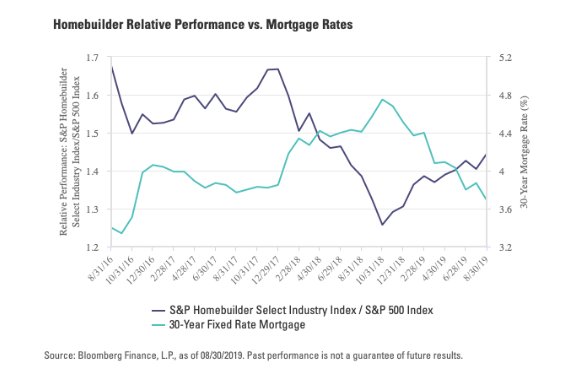

Last year, homebuilders underperformed the broad market by nearly 30% as rising interest rates dampened the demand of homebuyers. However, headwinds are turning into tailwinds this year. Falling 30-year mortgage rates and the Federal Reserve’s dovish monetary stance have boosted housing activity and homebuilder sentiment and lifted homebuilder stocks, as shown in the chart below.

The total of new and existing home sales has rebounded from the bottom since January and exceeded the previous peak in June 2017.5 Homebuilder sentiment, as measured by the NAHB/Wells Fargo Housing Market Index, picked up for the sixth straight month.6 These positive industry trends helped homebuilders deliver upbeat earnings results in Q2 and drove positive estimate revisions for 2019 and 2020.7

A strong labor market, rising wages, and favorable demographic changes are likely to continue supporting housing demand and homebuilders’ earnings growth. The homebuilders’ comeback may still have legs, as the industry is trading within the bottom quartile over the past 10 years based on trailing and forward price-to-earnings.8

To position for the decline in home-financing cost and supportive housing trends, investors can consider an allocation to SPDR® S&P® Homebuilders ETF (XHB).

3. Make a value play with a defensive nature

Health Care has been the worst-performing sector in 2019, as regulatory pressures related to drug pricing, insurance, and the opioid crisis have increased as the election draws nearer. This has weighed down the sector’s valuations to the lowest level since 2016 and made it the least expensive sector in the S&P 500® Index.9

Click here to read the entire article, which first appeared on October 31 on the SPDR blog.

Photo Credit: Chris Urbanowicz via Flickr Creative Commons

This material is from State Street Global Advisors and is being posted with State Street Global Advisors’ permission. The views expressed in this material are solely those of the author and/or State Street Global Advisors and Interactive Advisors is not endorsing or recommending any investment or trading discussed in the material. The opinions expressed may differ from those with different investment philosophies. This material is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed or relied on as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation to buy, sell or hold such security. This material does not and is not intended to take into account the particular financial conditions, strategies, tax status, investment horizon, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}