It’s been a real horse race between US large- and small-cap stock index performance in 2019, with both posting strong double-digit gains year-to-date (+16.2% for the Russell 1000 Index and +17.2% for the Russell 2000 Index as of May 10).

And according to our new insight, each is benefitting from its own unique macroeconomic drivers.

Alec Young, managing director, Global Markets Research, FTSE Russell:

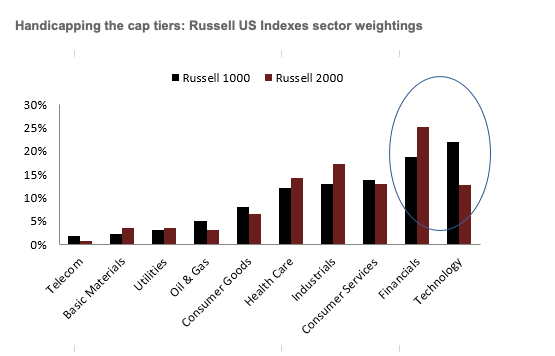

“The more domestic, small-cap Russell 2000 Index has been shielded from seemingly endless US–China trade worries because of its relatively small 21% foreign sales footprint (vs. 32% for the large cap Russell 1000 Index.)But large-cap stocks are enjoying advantages of their own. The Russell 1000 Index has a much higher exposure to technology than its small cap counterpart, a major advantage given technology’s strong year to date outperformance relative to other sectors. In addition, the large cap index is far less exposed to financials and health care, which have both underperformed in 2019.”

Photo Credit: Colin Knowles via Flickr Creative Commons

This article first appeared on the FTSE Russell blog on May 13.

© 2019 London Stock Exchange Group plc and its applicable group undertakings (the “LSE Group”).

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell indexes or research or the fitness or suitability of the FTSE Russell indexes or research for any particular purpose to which they might be put. Any representation of historical data accessible through FTSE Russell indexes or research is provided for information purposes only and is not a reliable indicator of future performance. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing contained in this document or accessible through FTSE Russell Indexes, including statistical data and industry reports, should be taken as constituting financial or investment advice or a financial promotion.

Views expressed by Alec Young of FTSE Russell are as of May 13th and subject to change. These views do not necessarily reflect the opinion of FTSE Russell or the LSE Group.