The financial-services industry needs to throw out its traditional playbook if it wants to reach Millennials and play a role in helping them realize their investing goals.

The stakes are high for both sides.

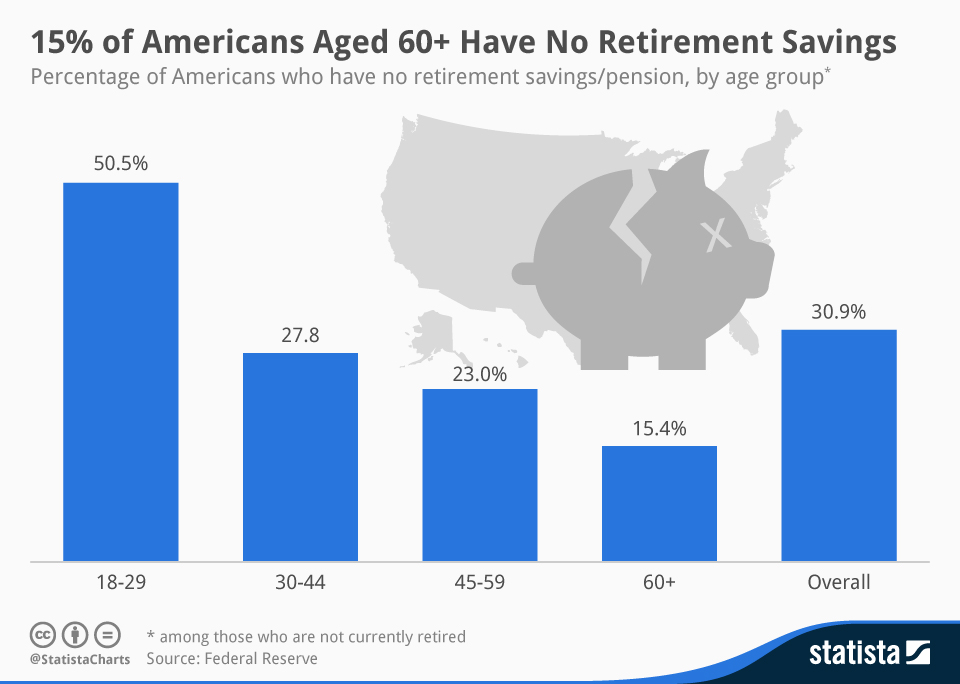

Many Millennials are at risk of falling behind on their financial goals because they haven’t even started investing yet. For example, about half of Americans between the ages of 18 and 29 have zero retirement savings, according to a Federal Reserve survey. Millennials, also known as Generation Y, are generally defined as those in their 20s or early 30s, and they are justifiably wary of the financial industry and the market.

The chart below is from Statista:

For Wall Street, many financial firms that focus on older, wealthier generations such as Baby Boomers are unprepared from the coming general shift. They will have to reshape their services and message to meet the needs of Millennials. To take just one example, traditional marketing and advertising doesn’t really work with many Millennials because they simply shut it out.

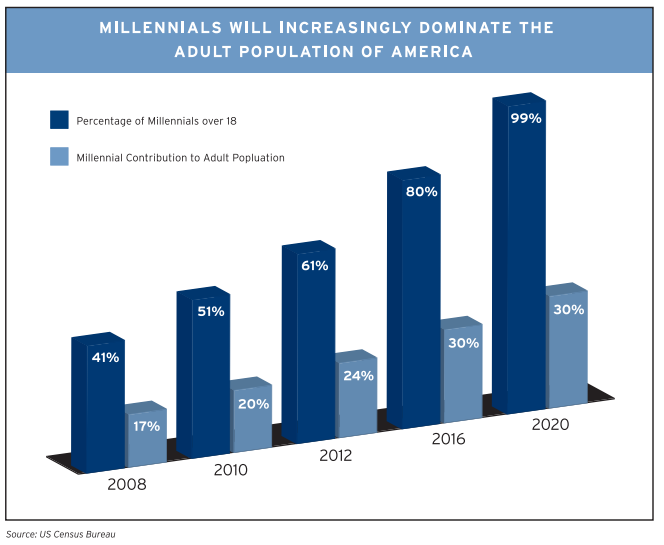

In about five years, more than one of three adult Americans will be Millennials, and by 2025 it is projected that this demographic will comprise as much as three-quarters of the workforce, according to the Brookings Institution.

Financial firms and advisers will have to rethink their approach to work with Millennials, who will soon be hitting their peak earning years.

Here are a few ways that Millennials are different from older cohorts:

- They’re extremely conservative as investors: Millennials are the most fiscally conservative generation since the Great Depression, according to a UBS survey. This makes sense because they’ve seen their parents get hit with two major bear markets the past 15 years. They tend to avoid the stock market and hold a higher percentage of cash than older investors. They’ve also witnessed the effects of the housing boom and bust.

- They’re very skeptical: The financial crisis has also made them understandably suspicious of Wall Street and potential conflicts of interest. Millennials require a high level of trust before they give their money to a bank or financial adviser. They verify — using information on the Internet, social media and from personal connections.

- They defy stereotypes: They may be seen as coddled and spoiled, but it turns out they care a lot about their financial futures and don’t want to repeat their parents’ mistakes. They’re tech savvy and highly educated as a group. They want to have control over their finances, so they’re more likely to be self-directed investors. They want to be comfortable, but they don’t want their lives to be dominated by money, which is often secondary to pursuits such as traveling, family, staying healthy, friends and volunteer work.

- They have financial challenges: In many ways, it’s not easy to be a Millennial. College tuitions have skyrocketed in recent years, and many graduates are saddled with high levels of student debt. The Class of 2014 is the most indebted ever. Rents and home prices are creeping higher while wages have mostly stagnated. Also, more Baby Boomers are staying in the workforce and delaying retirement after the financial crisis, making it harder for younger investors to find jobs. These are all reasons why Millennials are hitting major milestones later in life such as getting married, buying a house and having children.

- They tune out marketing and advertising: Perhaps more than any other generation, Millennials understand how marketing and advertising work, and they’re adept at ignoring it or even finding ways to turn it off completely. They don’t click on banner ads or open mass emails.

So, firms that “get it” with Millennials understand their unique habits and concerns. They communicate in language and mediums that resonate with Millennials, and show how their services are different and/or better.

Here are the ways Wall Street needs to change if it wants to be relevant to Millennials:

- What works with Baby Boomers doesn’t work with Millennials: You can’t market to Millennials in the same way as retirees, but this goes beyond just the message and investments. With social media, the financial-services industry is still doing what it always has — just faster and louder. As mentioned earlier, Millennials are keenly aware of when they’re being advertised or marketed to, and they resent it. Wall Street can’t talk down to Millennials. In some ways, Wall Street has to turn its traditional marketing strategy on its head to reach Millennials.

- Social media engagement: Social media is where Millennials get a lot of their information and learn about brands. According to recent study, 77% of Millennials own a smartphone and they spend nearly 15 hours a week texting, talking and on social media. However, companies need to engage followers on social media, not just talk AT them with links to their own blog posts and products. It needs to be a two-way street, with shares to other Facebook accounts and retweets to other Twitter handles. It’s important to educate followers, and be a part of the daily discussion with analysis of relevant, timely topics. Be helpful. And it helps to focus on a specific theme or niche, rather than trying to be all things to everyone. The reality is that Wall Street’s approach to social media is probably backfiring for a lot of financial-services firms. Millennials just see these companies the same way they see Grandpa trying to “do Facebook.”

- Personalize it: Millennials are leading the backlash against conglomerates — the huge companies with big marketing budgets and aggressive sales tactics. Some Millennials are gravitating to companies that take more of a personalized, Mom-and-Pop approach. Many are willing to pay a little extra to “feel good” about the companies they buy from and deal with.

- Beyond marketing: Millennials as a group do more research than anyone else, BEFORE they even begin the decision process of buying a product or service. They’re very good at using the Internet and social media to find what they want. If a company has a bad product, customer experience or corporate culture — Millennials will see right through it. And then they’ll tell all their friends on social media. No amount of slick marketing can fix a broken corporate culture.

“With advances in technology, the Internet, and mobility, the Millennials have had instant access to better and more information like no other generation before them,” says real estate marketing executive Sean Blankenship. “This has driven an intuitive ability to detect when brands are fake, not truthful, or inauthentic.”

The upside for financial firms is that they can build long-lasting relationships with Millennials if they earn their trust. If a company hits it out of the park with Millennials, they’ll probably stay loyal because they’re so wary of Wall Street. They just see a lot of “junk” out there in the investment world, so it’s up to the financial-services industry to work hard to change that perception.

{kind=link}