Millennials are often portrayed by the media as carefree, entitled, social-media addicts.

Yet when it comes to investing, these young adults (often classified as people ages 21-36) are actually the most fiscally conservative generation since the Great Depression, according to a report by UBS Wealth Management Americas.

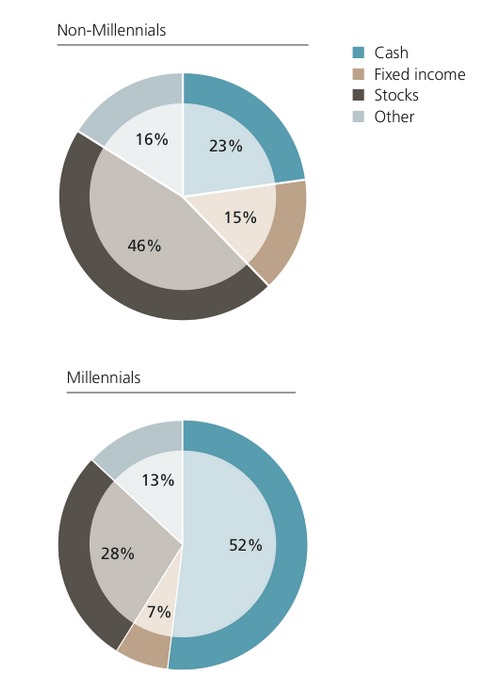

They’re ultra-conservative about stocks and have more than half of their financial assets wrapped up in cash, certificates of deposits and multi-money market funds, UBS data show.

It’s understandable that Millennials are wary of the stock market and investment risk in general after watching their parent’s portfolios get whacked by two crashes over the past 15 years.

However, when it comes to investing in the stock market, time is perhaps investors’ greatest ally. Of course, there will be corrections along the way. But over the long haul, history has shown that investing early and often can be a great way to build wealth, especially with compounding returns. Waiting even 10 years can have a dramatic impact on lifetime returns.

Patrick O’Shaughnessy, a Principal and Portfolio Manager at O’Shaughnessy Asset Management, has a useful post on Millennials’ investing phobia.

On the one hand, the aversion to investing in riskier assets makes sense. After all, Millennials have lived through the tech crash in 2000, the global financial crisis of 2008 and the subsequent Great Recession. The last time you had two big market blowouts in the same decade was the 1930s.

Even so, O’Shaughnessy says young people are missing something essential about risk and a lot of potential wealth. As he points out:

“The problem is that we tend to think of ‘risk’ as a fixed concept—that is, stocks are riskier than cash and bonds…period. But risk can only be accurately assessed in combination with a time horizon.

If you are 25 and saving for retirement, you have at least a 40 year time horizon, which drastically changes what is risky and what is safe. Millennials are making decisions as if they were 60 years old, on the verge of retirement—and it could cost them huge amounts of wealth.”

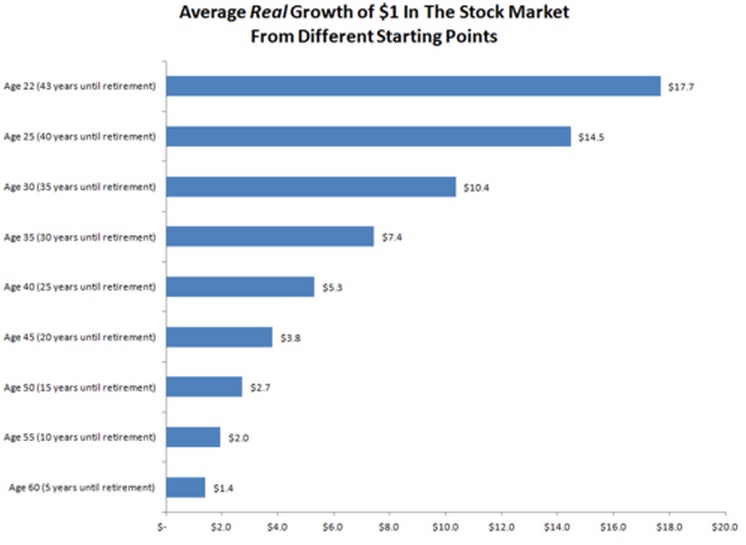

O’Shaughnessy went back to 1920 and calculated the average real growth of stocks and then looked at different time horizons of investing based on age. Not surprisingly, investors who start out in their 20s have time to weather the downturns and come out way ahead of older investing groups.

While Millennials are indeed burdened with student loans and a tougher job market, young adults with jobs are in many ways a generation of “super-savers,” according to a just-released study by Transamerica Center for Retirement Studies.

Most Millennials do not have a financial adviser, but fewer than 10% made their last key financial decision without consulting someone, according to asurvey by TIAA-CREF. They tend to look for input from multiple sources, including online.

“Millennials have seen what happened to their parents, many of whom lost their jobs and savings in the financial crisis—and they are taking steps to avoid a similar outcome,” says Catherine Collinson, president of the Transamerica center told Penelope Wang at Money magazine. “We’re seeing an emerging generation of retirement super savers.”

Millennials lucky enough to have jobs are taking advantage of 401(k) auto enrollment plans, automatic contribution hikes, and target date funds. Some 71% of Millennials who are offered a 401(k) end up joining their plan, according to Transamerica. If that trend holds up as more Millennials enter the workforce, the generation could end up far more thrifty than either Gen X-ers or the Baby Boomers.

Speaking of Gen X-ers (those born between 1966 and 1975) MainStreet.com interviewed Kimberly Clouse, Covestor Advisory Board Chair and founder of Via Global Advisors, about the financial hit this age group took during the financial crisis.

Clouse suggests low cost ETFs and mutual funds for those rebuilding their wealth. Fees, she says, are the one thing investors can control in these uncertain times.

To learn more about how Covestor works, contact our Client Advisers at clientservices@interactiveadvisors.com or 1.866.825.3005. Or you can try Covestor’s services with a free trial account.

DISCLAIMER: The information in this material is not intended to be personalized financial advice and should not be solely relied on for making financial decisions. All investments involve risk, the amount of which may vary significantly. Past performance is no guarantee of future results.