(Monthly Cash Review USD – July 2025)

By: William A.Goldthwait, Portfolio Strategist

Amid the noise, August presents a tactical opportunity—if fiscal hurdles clear. With yields shifting, investors may eye short-term moves with cautious optimism.

US Treasury yields sold off in May, and it looked like they might hold those levels until market data and commentary from the US Federal Reserve (Fed) pulled yields lower, dropping about 20 basis points (bp) by the end of the month. Fed funds futures also followed suit, ending June 20 bp lower. Rates volatility was the name of the game as markets tried to separate meaningful signals from the usual noise. Spoiler alert: There was a lot of noise.

But one message came through loud and clear: The Fed is warming up to the idea of a rate cut. The probability of a 25 bp cut in September surged from 60% at the start of June to nearly 94% by month-end. Some Fed officials are starting to sound like they are on board. Christopher Waller said, “I think we’re in a position that we could do this as early as July.” Michelle Bowman supported a rate cut “as soon as July,” although the Chair Jerome Powell was of the opinion that “there is time to wait for more clarity,” and was supported by Susan Collins and Mary C. Daly. They seem to say, “We’re not cutting yet, but we’re definitely thinking about it.”

Cash on deck

Commercial paper yields mirrored the Treasury rally, and the demand for short-term credit remained strong. With cash balances still ballooning, investors were eager to put money to work. Credit spreads, however, did not budge (Bloomberg 1-3-year A+ option-adjusted spreads), which keeps us cautious on corporate credit.

Meanwhile, the Fed’s Reverse Repo Program (RRP) continues to act like a sponge, soaking up excess liquidity. At quarter-end, RRP usage hit $460 billion—up from $400 billion in Q1 and just shy of the $473 billion peak in December 2024. We expect this to drop sharply once the debt ceiling is raised and US T-Bill supply is unleashed—fingers crossed that Congress passes the Big Beautiful Bill (BBB) soon.

August advantage

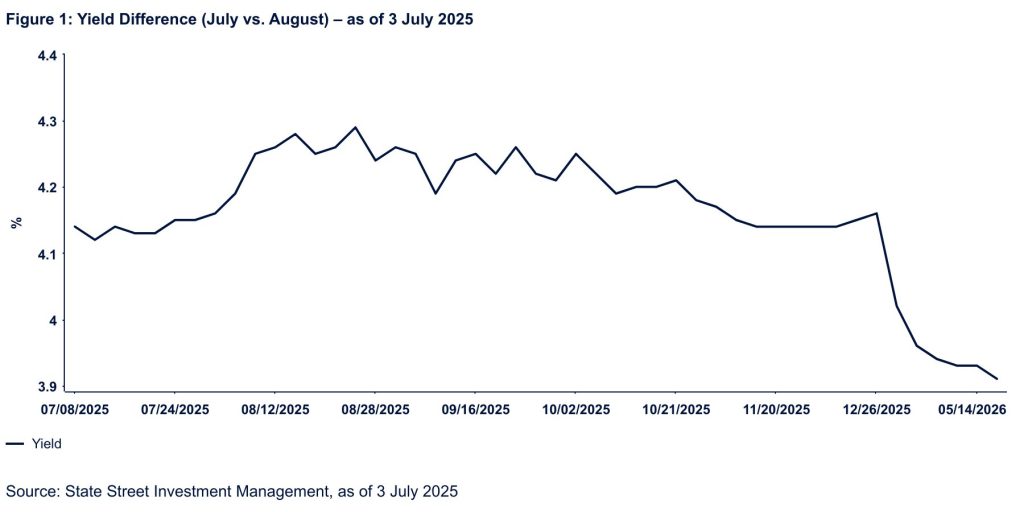

Speaking of T-Bills, we have seen some strange behavior in the short end of the curve. A few weeks ago, a 2-month T-Bill auction tailed by 7 bp, and that kicked off a repricing of the August and September T-Bill curves. Why? There were two reasons:

- Debt ceiling drama: Investors are worried the US Treasury might run out of cash. At the time of writing, US Treasury’s checking account sits at $304 billion. That might sound like a lot, but as anyone who has been to Vegas knows, that can disappear fast. Estimates suggest the Treasury could run dry by August or September.

- Incoming supply tsunami: Once the debt ceiling is lifted, we are expecting $500–700 billion in new T-Bill issuance to refill the US Treasury’s checking account. That is a lot of paper, and is likely to push money market yields higher.

The result? A kink in the T-Bill curve. At the time of this writing there is a 10- to 15-bp spread between the July and August bills—an unusually wide gap. And with a Fed meeting scheduled for 30 July, those yields should be closer than 11 bp. The yield difference has been wider on an intraday basis, reflecting the uneasy feeling in the market. The 28 August bill before the curve slopes downward again.

So, where is the opportunity? If you believe the debt ceiling drama will pass without issue, we think there is value in those August bills. This situation is similar to June 2023, when increased T-Bill supply post the debt-ceiling-raise caused yields to rise. The risk, of course, is that the deficit hawks may delay action and cause chaos in the bill market. That is not our base case, but certainly something to be aware of. But as always, time (and Congress) will tell.

Originally posted on July 9, 2025 on State Street Investment Management blog

PHOTO CREDIT: https://www.shutterstock.com/g/Zhao+jian+kang

VIA SHUTTERSTOCK

DISCLOSURES

State Street Global Advisors (SSGA) is now State Street Investment Management. Please go to statestreet.com/investment-management for more information.

Marketing Communication

State Street Global Advisors Worldwide Entities

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without State Street Global Advisors’ express written consent.

Investing involves risk including the risk of loss of principal.

The views expressed in this material are the views of William Goldthwait through July 07, 2025 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

The value of the debt securities may increase or decrease as a result of the following: market fluctuations, increases in interest rates, inability of issuers to repay principal and interest or illiquidity in the debt securities markets; the risk of low rates of return due to reinvestment of securities during periods of falling interest rates or repayment by issuers with higher coupon or interest rates; and/or the risk of low income due to falling interest rates. To the extent that interest rates rise, certain underlying obligations may be paid off substantially slower than originally anticipated and the value of those securities may fall sharply. This may result in a reduction in income from debt securities income.

All information is from State Street Global Advisors unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Past performance is not a reliable indicator of future performance.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

These investments may have difficulty in liquidating an investment position without taking a significant discount from current market value, which can be a significant problem with certain lightly traded securities..

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator” who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

© 2025 State Street Corporation – All Rights Reserved

{kind=link}

{kind=link}