By: Yale Bock, Y H & C Investments

June was a remarkable month in the Middle East. With the bombing of the large nuclear facilities in Iran, Israel and the United States forced a cease fire with the world’s leading sponsor of terrorism. The implications for the future are potentially enormous. First, there is a chance the region could see a sustained period of peace for a long time. It is possible many Arab countries, specifically Sunni based, will line up to join the Abraham accords and want to have a multi country agreement with Israel. One thing we do know is Iran has militarily been neutered. Whether the current regime stays in power remains to be seen, but certainly they are dramatically weakened and potentially vulnerable to a quick change of leadership. Time will tell on that front and things could go haywire at any moment, so the world is most certainly paying attention.

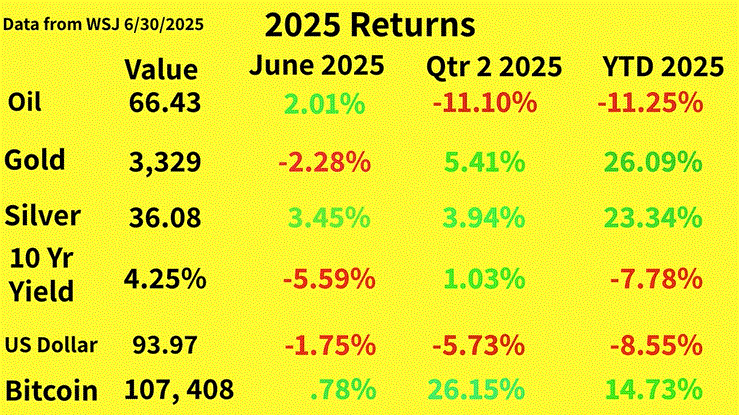

Source: Return figures come from the June 30, 2025, edition of the Wall St. Journal.

Economically, the major implication is in the energy markets. Taking a regional conflict off the table means any war premium in the price of oil may disappear. Lower energy prices are a good thing for many countries and for the global economy. Relatedly, with the investment world agog in the growth possibilities of artificial intelligence, a little second order thinking is needed. If AI is going to become the be all and end all of everything with use cases in every industry, the demands on the electrical grid will be enormous. Utilities are currently afforded a premium in the markets because of this projected demand. In order for it to happen, the utility industry needs the power generation capabilities from some input. Guess what those inputs probably are? Natural gas and coal, and maybe some nuclear. The most obvious one is natural gas. What entities produce a great deal of natural gas? Yes, you guessed right, the largest oil companies. It very well could be the biggest beneficiary of the AI boom are the big bad energy companies. Hope I got you thinking!

Elsewhere, the 32 NATO countries agreed to increase defense spending of up to 5% of GDP by 2035. President Trump and the position of the United States played a large part in pressuring the leaders of NATO to understand why this is important. Here in North America, there remains continuing disagreement between Canada and the United States about trade and tax policy. The most recent spat involves a digital tax levied by Canada in the technology arena (it appears Canada caved tonight). The rest of the globe seems to be lining up to strike agreements with the Trump Administration, and by the end of the summer one gets the sense the trade situation should mostly be settled.

On the domestic front, the big, beautiful bill looks as if it will pass through the Senate by July 4. Reconciliation waits for a final product that President Trump will undoubtedly be very happy to sign. Two areas of the bill I am paying particularly close attention to are the Medicaid piece and the alternative energy tax credit eliminations. The Medicaid portion is important because the Democrats will probably attack Republicans as being heartless monsters for taking away Medicaid from grandma while doling out tax cuts to the rich and blowing up the national deficit (as if the Democratic party was devoted to the religion of fiscal prudence). With the alternative energy tax credits, those segments of the market have been crushed, and some believe the long-term prospects are still quite attractive.

Originally posted on July 1, 2025 on Y H & C Investments blog/ newsletter

PHOTO CREDIT: https://www.shutterstock.com/g/Rokas+Tenys

VIA SHUTTERSTOCK

DISCLOSURES:

Y H & C Investments may have positions in companies mentioned in this newsletter. Nothing in the newsletter should be taken as an offer to buy or sell individual securities. It is the responsibility of each investor to research the investments mentioned so they can decide on the appropriateness and suitability of the investments consistent with their risk tolerance, risk constraints, and return objectives.

Past performance is no guarantee of future results, and all investments involve the risk of loss, including loss of principal and a reduction in earnings.

{kind=link}

{kind=link}