By:

Samuel Rines, Micro Strategist

Jeff Weniger CFA, Head of Equity Strategy

Key Takeaways

- In Q2 2025, companies like Pepsi and P&G showed that the era of aggressive price hikes covering for volume declines, known as “Price over Volume” (PoV), is waning as elasticity and consumer resistance grow amid new tariffs.

- Despite strong brands still wielding some pricing power, the easy PoV gains of 2021–2023 are over, with inflation fatigue and tariff-induced cost pressures shifting the balance of power back to the consumer.

- WisdomTree’s U.S. equity mandates, with their higher-than-benchmark profit margins, may offer investors a buffer in a PoV 2.0 world, where defending margins while regaining volume is key to outperformance.

“Price over Volume” (PoV) had its Princess Bride moment. In the cult classic movie, the characters take their friend’s dead body to a quirky healer. “It just so happens that your friend here is only mostly dead. There’s a big difference between mostly dead and all dead. Mostly dead is slightly alive.”

“Mostly dead” is what happened to Price over Volume, especially among consumer goods companies. In recent years, many drove revenue growth predominantly by raising prices, with minimal concern for slight volume declines.

Now, amid tariff fears, earnings season raised the question: Is it still a PoV World? Or are volume pressures finally starting to bite? The answer, it seems, is a bit of both: pricing power remains a growth lever, but volumes are showing strain. The new tariff regime is set to test the limits of pricing power further. Companies are still managing to push through price gains, but elasticity is no longer negligible. And tariffs threaten to raise input costs, squeezing margins.

We checked in on our U.S. equity mandates. Every one of them has higher net profit margins than their respective Morningstar benchmarks (figure 1 here). If the Price over Volume world is over, or simply dented, our holdings would seemingly have an extra buffer because of their thick profit margins.

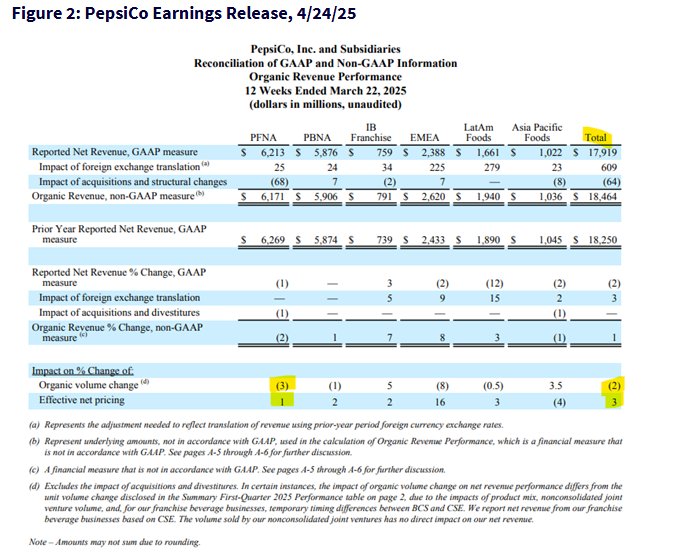

Pepsi provides a cool PoV case study. A few years ago, the company was a clear front-runner in its ability to ratchet up prices without sacrificing volumes. That has changed. Notably, the company’s snack segment (PepsiCo Foods North America—“PFNA”) saw volume fall 3% in its latest earnings report. Pricing? That was only up 1%.

Granted, pricing power has not evaporated—consumers are still paying up for Doritos and soda, with total volume declines of 2% offset by a 3% jump in prices (figure 2). But that does not make for an overly inspiring PoV narrative.

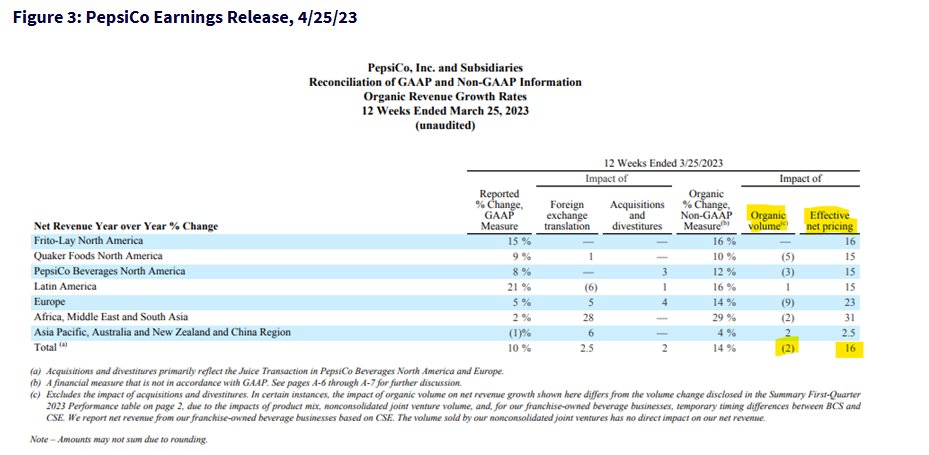

The era of double-digit price jumps is clearly over; this quarter’s low-single-digit pricing increase is a far cry from the peak PoV era. Not long ago—during the same quarter in 2023—Pepsi also reported a 2% decline in volume amid price increases of 16% (figure 3). That was the golden age of PoV. To re-reference The Princess Bride, Pepsi’s PoV thesis is mostly dead. Yes, price hikes are still covering for volume weakness, but the game has changed.

Though Pepsi does not instill much confidence in the return of PoV, Procter & Gamble gives the concept a twist. The company’s explicit statement is that price hikes are a tool to offset tariff pressures. Like Pepsi, P&G also faces the issue of competition from the post-COVID-19 boom in private labels, so the company is far from an example of PoV being alive and well. Instead, it’s an example of the emerging trend of companies threatening to return to PoV. It looks like some firms may start to take a blade to operating costs to maintain margins. If there is a hint of life for PoV, it is because tariffs are lighting a fire under companies to revive the “mostly dead” patient.

The play is clear, at least to us: raise prices, then blame it on import duties.

Figure 4: P&G Earnings Call, 4/24/25

Andre Schulten

Chief Financial Officer

Good morning, Andrea. Yes, the $1 billion to $1.5 billion before tax is the impact that we are estimating based on what we know today. That means the tariff rates that have been announced and enacted both in the U.S. and in all other markets in response to the U.S. tariffs. Exactly as you say, that’s about 3% of cost of goods sold, about 140 to 180 basis points margin impact. The point — this is not an average discussion, though, right? Because the impact is on certain SKUs, on certain brands and certain category country combinations.

So when we average this out across the globe, the numbers that you quote are correct. But if you look at certain market category combinations, the numbers in terms of pricing are way more significant that we would have to take net of what we believe we can deliver in productivity and other mitigating factors. So that’s exactly the work that the teams are doing now. And that’s why we keep all of the tools on the table. We will start with productivity. We will look at sourcing changes and formulation changes, which typically take longer. We will look at pricing with innovation, and we will look at straight pricing. All of those elements are on the table, and we’re working through them right now.

Tariffs act as a supply chain shock, but we have been here before.

Into late 2025 and perhaps 2026, the combination of still-robust consumer health and the lingering inflationary mindset from the COVID-19 supply chain muck-up might make it relatively easy for companies to pass through some tariff-related inflation. But price-sensitive shoppers will switch to off-price or discounted items if markups get out of control.

The tug-of-war between a still-healthy job market (which supports spending) and inflation exhaustion (which limits consumers’ willingness to spend) creates a mixed picture for the success of PoV going forward. For now, staples companies are betting that their products are sufficiently nondiscretionary to avoid a volume collapse. Again, Price over Volume is only mostly dead.

At the moment, the 2021–2023 PoV theme is not surging back. That dynamic, pushing prices aggressively and in turn bolstering revenues and margins with only moderate hits to product volumes, is over. But this does appear to be an era of PoV 2.0. There will be attempts to push prices up, but those will prove problematic for volumes. The easy gains are gone.

The PoV thesis isn’t completely dead— pricing power always matters for strong brands—but it’s no longer a blank check. The balance of power is tilting back toward the consumer, slowly but surely. Whether it’s snacks and sodas, the message is consistent: future earnings will depend on winning back volume growth (or at least keeping volumes flat) while defending margins from both inflation and tariffs. Striking that balance will determine who thrives in the mostly dead PoV landscape. Companies that can maintain pricing discipline and entice customers with value will emerge on solid ground. Those who misjudge the new regime risk learning the hard way that volume, in the end, does matter after all.

Originally posted on May 29, 2025 on WisdomTree blog

PHOTO CREDIT: https://www.shutterstock.com/g/iLixe48

VIA SHUTTERSTOCK

DISCLOSURES

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

{kind=link}

{kind=link}