By:

Mark Barnes PhD, Head of Global Investment

Indhu Raghavan CFA, Manager – Global Investment

Currency risks in unhedged global equity portfolios can be material to returns. As historical relationships between equities and currencies such as that between US equities and the US dollar can change quickly, investors may need to revisit hedging decisions periodically.

- Currency risks in unhedged global equity portfolios can be material to returns, outcomes we have seen during January-April 2025 for unhedged US equity allocations

- Given the dominance of US assets in benchmark equity and fixed income portfolios, the impact of relative US dollar moves on portfolio returns can be large

- As historical relationships such as that between US equities and the US dollar can change quickly, it may be necessary to revisit hedging decisions periodically

Amidst all the challenges global equity investors have faced in 2025 thus far, US dollar weakness is a critical, and somewhat unexpected, one. US equities posted steep losses year-to-date (YTD) through April 2025, as we highlight in the May 2025 Performance Insights reports. To some extent, those losses have been the result of a downbeat outlook on US equities. But US equity losses have been exacerbated for non-US investors by unfavorable currency moves. This insight focuses on the impact of relative currency moves on equity returns and underscores the need to focus on currency risk embedded within unhedged global equity portfolios.

The dollar conundrum

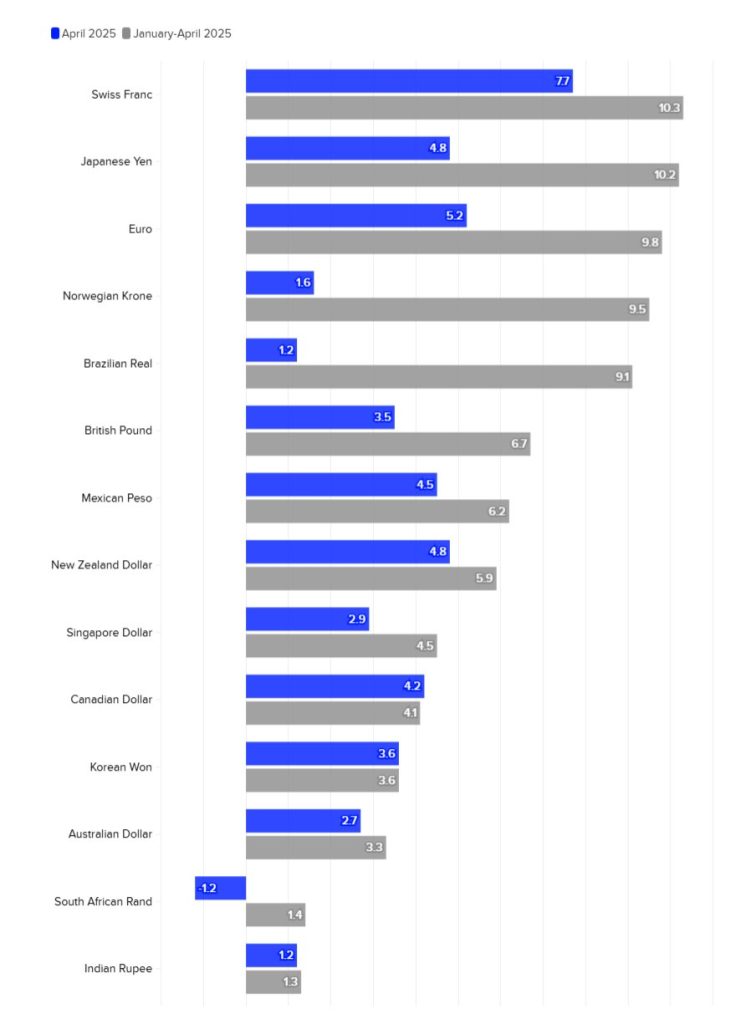

The US dollar’s performance YTD has been unexpected. The anticipated tariff policies of the new US administration were expected to put upward pressure on the dollar with tariff imposition dampening US imports and the relative demand for foreign currencies. In fact, we saw a preview of this right after the US presidential elections in 2024 when the dollar surged during November and December. However, YTD through April 2025 the opposite happened, when most global currencies strengthened relative to the dollar (Exhibit 1).

A further puzzle is that during times of market stress the US dollar tends to be one of the safe-haven assets that investors flock toward. Again, the opposite happened during the recent market turmoil. In April, which was a particularly volatile month for global equities, other haven currencies such as the Swiss franc and Japanese yen strengthened (versus the US dollar and other global currencies), but the dollar weakened broadly.

Source: FTSE Russell/LSEG. Data as of 30 April 2025. Past performance is no guarantee of future results.

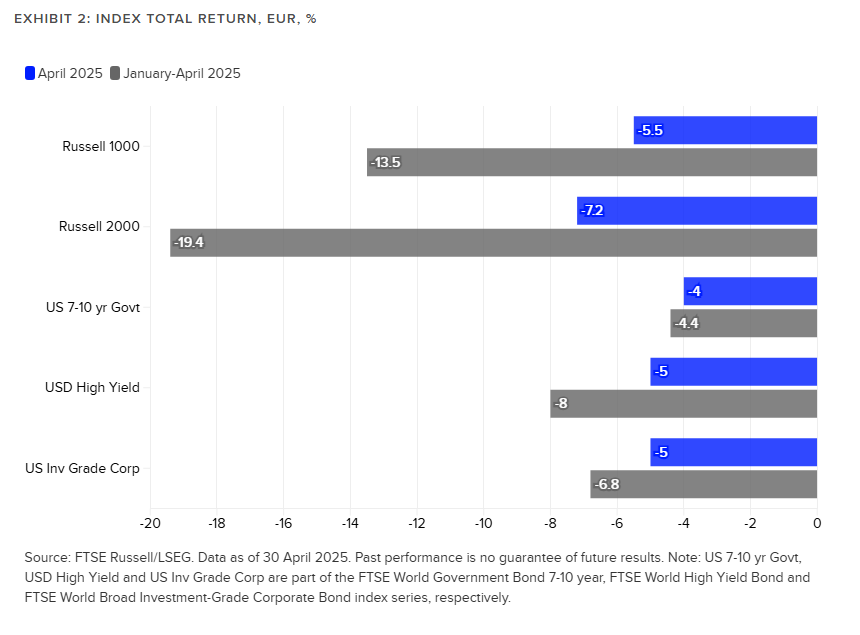

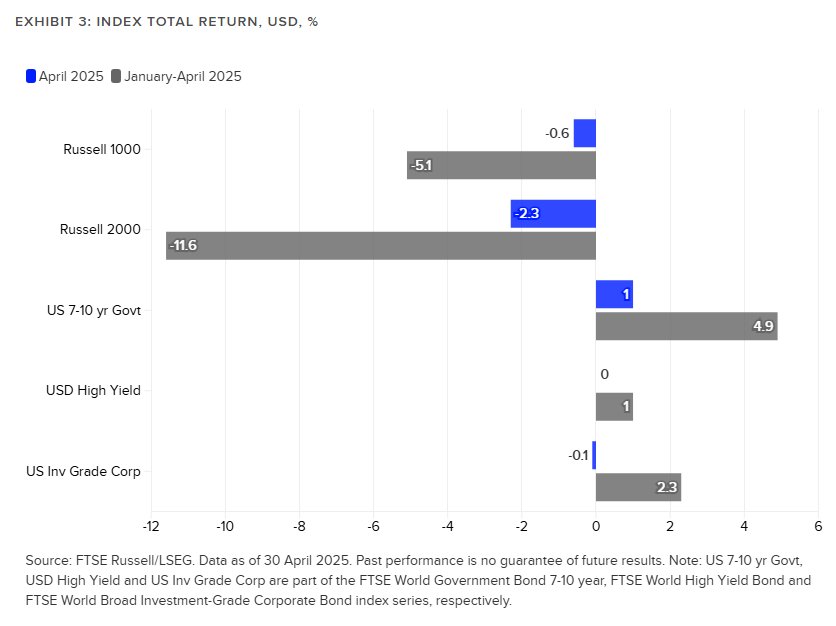

These unexpected moves in the US dollar’s value pose a challenge for global equity investors who do not hedge currency exposures in their equity portfolio. Let’s take the example of a hypothetical unhedged Euro-based investor. This investor experienced steep losses on their US equity allocation this year. The Russell 1000 and Russell 2000 indices returned -13.5% and -19.4% YTD through April 2025 in Euro terms when unhedged (Exhibit 2). However, if this Euro-based investor had hedged their US dollar exposure, thereby removing or reducing the impact of currency moves on their US equity returns, those losses would have been lower. The Russell 1000 and Russell 2000 indices returned -5.1% and -11.6% YTD through April 2025 in USD terms (Exhibit 3). This is equivalent to a hedged return, not accounting for hedging and other costs. The difference between unhedged and hedged returns stemmed from the US dollar’s losses YTD relative to the Euro.

Exhibits 3 and 2 also show that US fixed income exposures would have flipped from gains to losses for an unhedged Euro-based investor.

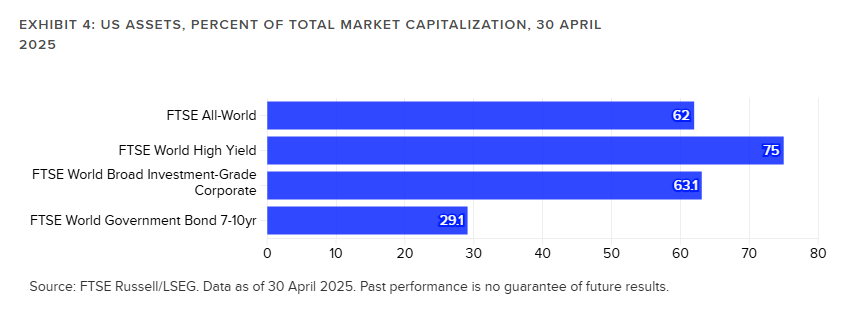

The impact on unhedged global portfolios of changes in the dollar’s relative value can be significant. US equities constituted over 60% of an equity portfolio that tracked the FTSE All-World global equity benchmark as of April 30, 2025 (Exhibit 4). In addition, many portfolios are overweight US equities given the US’s outperformance of other regional equities over the last decade and the promise of AI which has fueled the US tech rally over the last two years. Similarly, global credit is also dominated by US high yield and investment grade credit. Hedging is a way to reduce portfolio risk by eliminating the currency risk and taking on equity or fixed income risk alone.

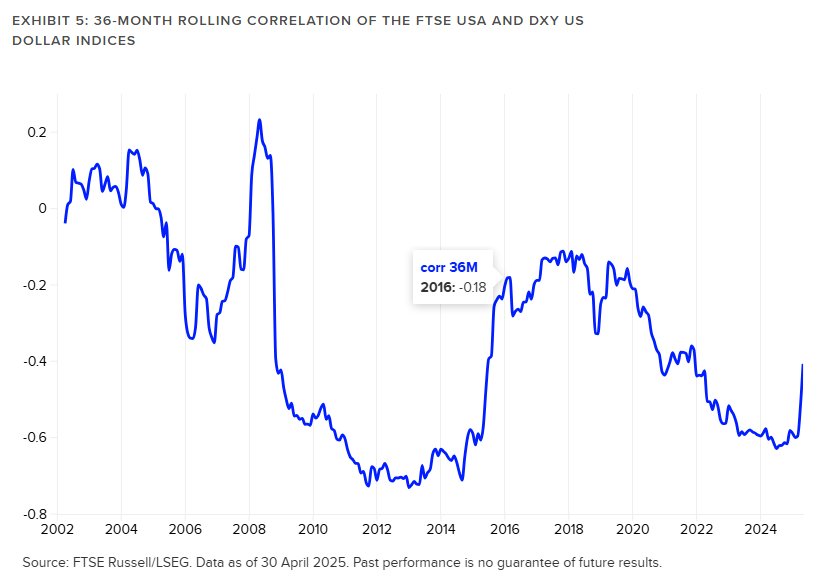

Historically speaking, the US dollar has provided a natural hedge (to some degree) to US equity exposure. Exhibit 5 illustrates how. It shows the rolling 36-month correlation between the FTSE USA index and the DXY US dollar index. For the most part, over the last 20 years, this relationship has been negative, i.e. generally speaking, when US equities have fallen the US dollar has risen in value to some degree.

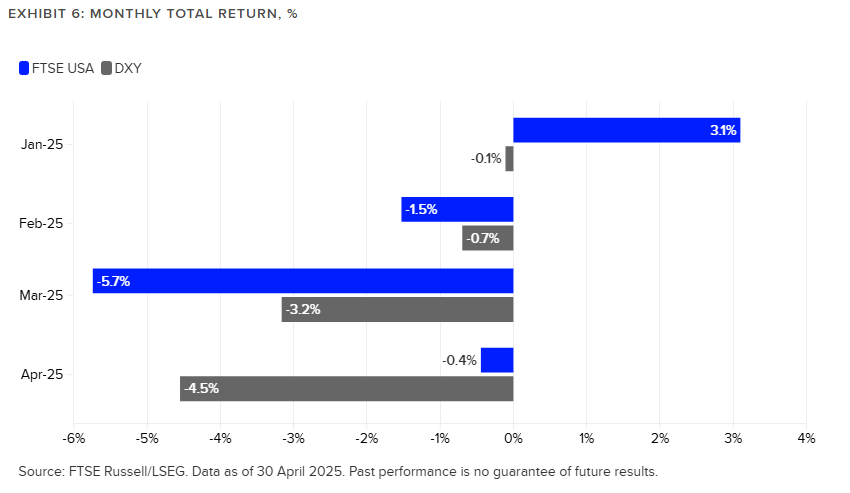

This relationship has seen sharp changes in the past, such as during the 2007-08 Global Financial Crisis when the correlation rose sharply (as asset correlations tend to do during crises) and then fell deeper into negative territory, potentially buffering some of the US equity losses at the time for global investors. Since the end of 2024, we have observed the 36-month correlation spiking. In fact, during February – April 2025, the direction of returns on both assets was the same (Exhibit 6).

Conclusion

There have been many explanations posited for why investors are shunning US equities and the dollar at the same time. That discussion is beyond the scope of this article. But the bottom line is that currency risk can be material, and hedging decisions, i.e. to hedge or not to hedge and to what extent, can make a real difference to return the outcomes. At a time when markets are witnessing sharp shifts in historic relationships, such as that between the US dollar and US equities in 2025 thus far, it is worth revisiting those decisions.

Originally posted on May 15, 2025 on FTSE Russell blog

PHOTO CREDIT: https://www.shutterstock.com/g/violetkaipa

VIA SHUTTERSTOCK

DISCLOSURES

The content of this publication is provided by London Stock Exchange Group plc, its applicable group undertakings and/or its affiliates or licensors (the “LSE Group” or “We”) exclusively.

Neither We nor our affiliates guarantee the accuracy of or endorse the views or opinions given by any third party content provider, advertiser, sponsor or other user. We may link to, reference, or promote websites, applications and/or services from third parties. You agree that We are not responsible for, and do not control such non-LSE Group websites, applications or services.

The content of this publication is for informational purposes only. All information and data contained in this publication is obtained by LSE Group from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data are provided “as is” without warranty of any kind. You understand and agree that this publication does not, and does not seek to, constitute advice of any nature. You may not rely upon the content of this document under any circumstances and should seek your own independent legal, tax or investment advice or opinion regarding the suitability, value or profitability of any particular security, portfolio or investment strategy. Neither We nor our affiliates shall be liable for any errors, inaccuracies or delays in the publication or any other content, or for any actions taken by you in reliance thereon. You expressly agree that your use of the publication and its content is at your sole risk.

To the fullest extent permitted by applicable law, LSE Group, expressly disclaims any representation or warranties, express or implied, including, without limitation, any representations or warranties of performance, merchantability, fitness for a particular purpose, accuracy, completeness, reliability and non-infringement. LSE Group, its subsidiaries, its affiliates and their respective shareholders, directors, officers employees, agents, advertisers, content providers and licensors (collectively referred to as the “LSE Group Parties”) disclaim all responsibility for any loss, liability or damage of any kind resulting from or related to access, use or the unavailability of the publication (or any part of it); and none of the LSE Group Parties will be liable (jointly or severally) to you for any direct, indirect, consequential, special, incidental, punitive or exemplary damages, howsoever arising, even if any member of the LSE Group Parties are advised in advance of the possibility of such damages or could have foreseen any such damages arising or resulting from the use of, or inability to use, the information contained in the publication. For the avoidance of doubt, the LSE Group Parties shall have no liability for any losses, claims, demands, actions, proceedings, damages, costs or expenses arising out of, or in any way connected with, the information contained in this document.

LSE Group is the owner of various intellectual property rights (“IPR”), including but not limited to, numerous trademarks that are used to identify, advertise, and promote LSE Group products, services and activities. Nothing contained herein should be construed as granting any licence or right to use any of the trademarks or any other LSE Group IPR for any purpose whatsoever without the written permission or applicable licence terms.

{kind=link}