By: Kevin Flanagan, Head of Fixed Income Strategy

Key Takeaways

- Following September’s rate cut, markets are pricing in further Federal Reserve easing, driven by perceived labor market weakness.

- 2024’s labor data shows that downward payroll revisions misled markets before a late-year rebound…could 2025 follow a similar trajectory?

- If the labor market is nearing a bottom and job creation surprises to the upside, investors may need to rethink the consensus Fed path.

Up to now, the Federal Reserve and the bond market have been operating under the assumption that the employment setting has been cooling in a somewhat visible fashion. In fact, recent comments from Powell & Co. underscore how the employment aspect of their dual mandate is where the greater risk may lie. No doubt this was the reason behind September’s rate cut and the expectation of another easing move at this month’s FOMC meeting, and even potentially at the December policy making gathering.

That got me thinking. Back in my days on the fixed income trading floor, we would always consider the “other side of the trade.” In this case, it would be what if the labor market already reached its low point and that some better readings could be looming on the horizon?

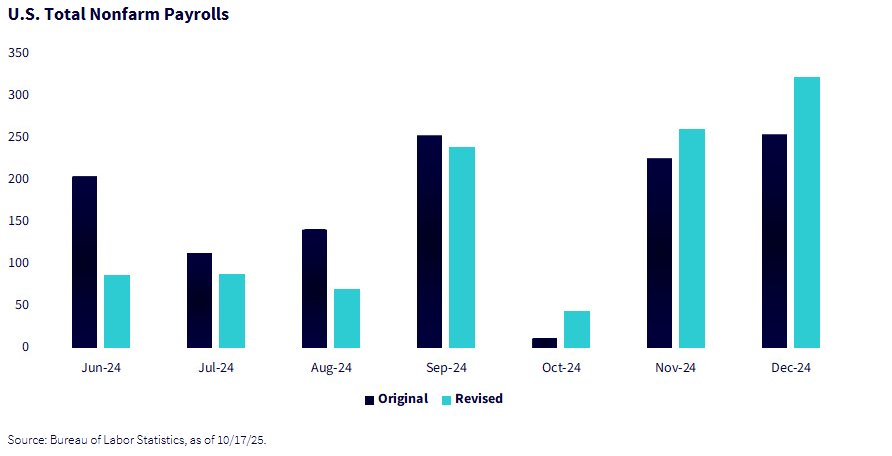

What struck me most were the parallels between what the jobs numbers did last year, as compared to this year’s experience. The downward revisions we saw in summer’s nonfarm payrolls changed the entire perception of labor market conditions, from solid to visible cooling. After a quick glance at the enclosed chart, you might be saying to yourself, this was the 2025 experience, NOT what occurred a year ago. But this chart is for 2024!

As you can see, some noteworthy downward revisions also occurred during the June–August 2024 period. Over this three-month period, the level of new job creation was scaled back by 216,000, which is not too far removed from the 258,000 downward revisions that changed everything this year. As you may recall, last year’s revisions ultimately led to the beginning of the rate cut cycle, and fast-forward to the 2025 experience, the resumption of easing moves at last month’s FOMC meeting.

However, check out what happened in Q4 of last year (the October readings can be discarded due to the negative impacts of both Hurricanes Helene and Milton). Indeed, not only did the November and December payrolls bounce back in a noticeable way, but they were then revised upward.

Conclusion

For the record, I’m not saying that we are going to see the same end result for the final two months of this calendar year. In fact, one could argue that the November 2024 nonfarm payroll number may have been somewhat inflated by the fact that the aforementioned hurricanes were over. However, the “student body right” narrative for the Fed and the bond market is, without a doubt, centered on a weakening employment setting, leading to Fed Funds Futures pricing in three rate cuts for 2026. Hence, what if some version of last year’s payroll phenomenon occurs this year? Now that’s what is called the other side of the trade, for sure.

Originally posted on October 22, 2025 on WisdomTree blog

PHOTO CREDIT: https://www.shutterstock.com/g/Zerbor

VIA SHUTTERSTOCK

DISCLOSURES:

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Alejandro Saltiel, Andrew Okrongly, Behnood Noei, Bradley Krom, Brendan Loftus, Brian Manby, Christopher Gannatti, David Graichen, Hyun Ku Kang, Jeff Weniger, Jeremy Schwartz, Jonathan Steinberg, Joseph Grogan, Joseph Tenaglia, Kara Dombroski, Kevin Flanagan, Lauren Pfendt, Liqian Ren, Lonnie Jacobs, Matt Wagner, Rick Harper, Ryan Krystopowicz, and Vanya Sharma are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

{kind=link}