By: Chris Carpentier, CFA, FRM, Senior Investment Strategist

US inflation is expected to settle in the upper 2% range through 2026, a level historically linked to strong corporate profits and healthy equity market returns, creating a favorable economic backdrop.

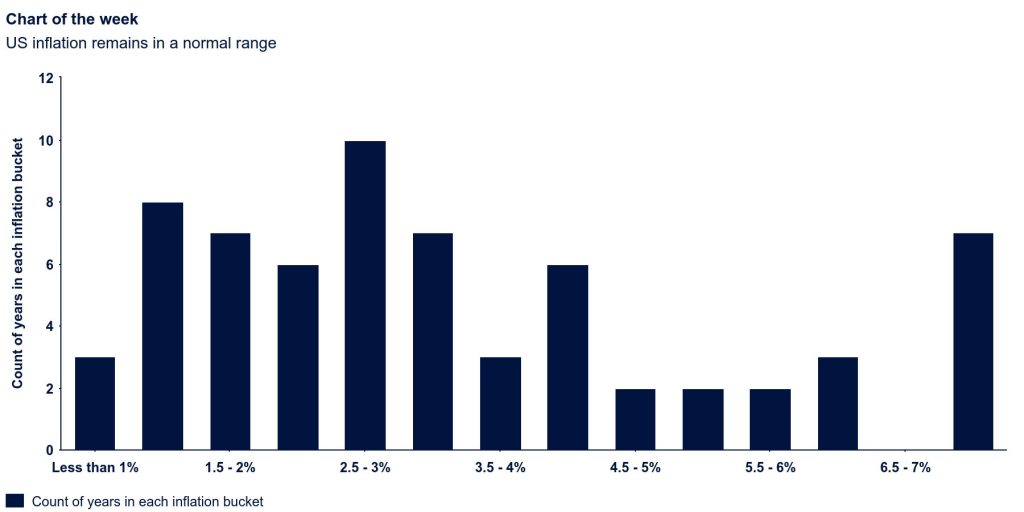

The final stretch to 2% inflation has long been considered the hardest. After ending 2024 at 3%, CPI is projected to settle in the upper 2% range through 2026. Historically, this level sits at the center of the inflation distribution over the past 66 years—an area that reflects economic normalcy rather than stress. Before the 2022 inflation spike, the US was inflation-starved, with the last reading above 2.5% occurring in 2011. In reality, inflation in the upper 2% range is historically quite normal.

Upper 2% inflation: A forgotten sweet spot for corporate profits

As we move through 2025 and look ahead to 2026, consensus expectations suggest inflation will hover in the upper 2% range. While headlines often frame inflation as a risk factor, history tells a more nuanced story: moderate inflation has often coincided with strong corporate profitability and healthy equity market returns. Yet, this relationship is frequently overlooked in today’s discourse, which tends to focus on extremes—either the specter of runaway prices or the drag of deflation.

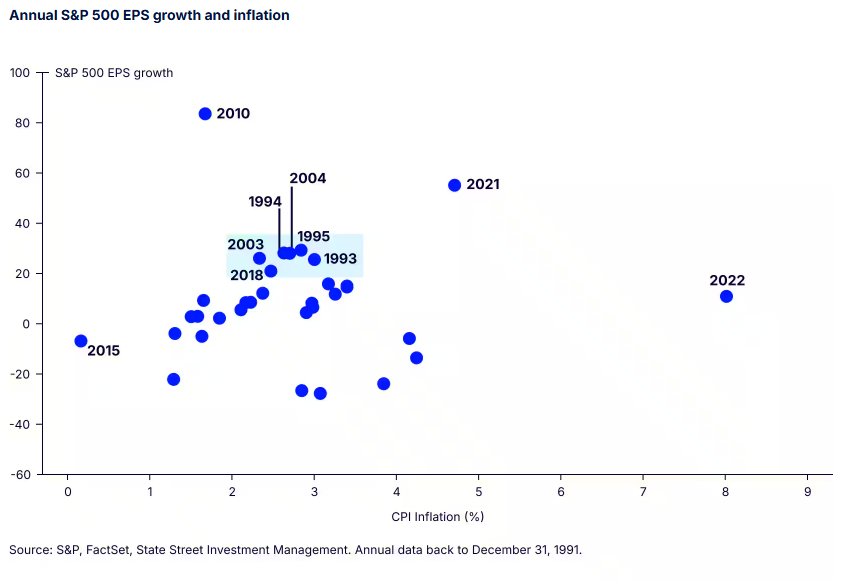

Inflation in the 2–3% corridor can be a constructive backdrop for U.S. equities. The chart above is almost 35 years’ worth of annual CPI Inflation along with the corresponding S&P 500 earnings growth. The main observation is that there is a nice clustering of > 20% earnings growth years in the 2-3% inflation bucket, which isn’t really seen in the other inflation areas. In essence, modest inflation acts as an enabler for economic activity. It allows companies to pass through incremental cost increases, expand revenues in nominal terms, and maintain or even improve operating leverage—particularly if productivity gains or scale efficiencies offset rising wages and materials costs.

Why upper 2% inflation is constructive

The Federal Reserve’s long-standing target of 2% inflation reflects a level consistent with price stability and sustainable growth. When inflation runs slightly above that—say, in the 2.5–3% range—it often signals robust demand without tipping into overheating. For corporates, this environment offers a couple of advantages:

- Pricing Flexibility: Firms can raise prices modestly without triggering consumer backlash, preserving margins even as input costs rise gradually.

- Nominal Earnings Growth: Revenue lines expand in nominal terms, which matters for equity valuations tied to earnings per share.

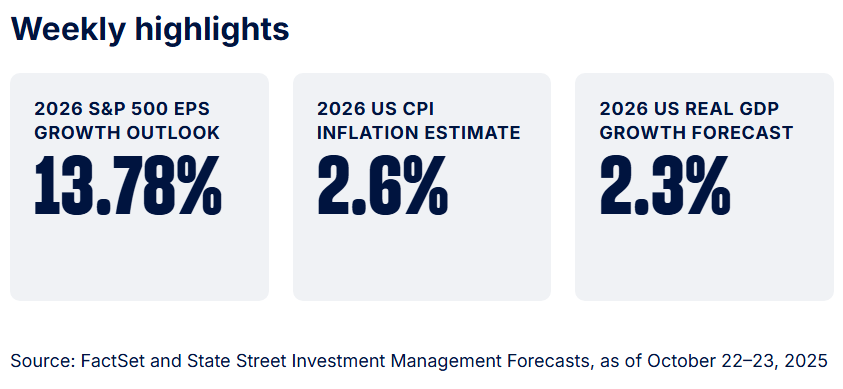

The link between inflation and earnings is not linear; it depends on the source of inflation and the corporate sector’s ability to manage costs. Demand-pull inflation, driven by strong consumer demand,supports both volume and pricing, while cost-push inflation from supply shocks can compress margins ifpass-through lags. The post-pandemic surge in inflation illustrated this dynamic, as profit margins initially spiked but later normalized when input costs surged. Looking Ahead, we believe real GDP growth in 2026 will be above trend, around 2.3%. Policy measures—such as lower taxes for both corporations and individuals, higher consumer tax refunds looking to be spent, along with some other kickers of the OBBB like increased capex spending due to immediate expensing forcorporations—should sustain demand for goods and services. In our view, inflation is likely to remain tame and not materially spike further, creating a favorable backdrop for profitability and margins.

Originally posted on October 27, 2025 on State Street Investment Management blog

PHOTO CREDIT: https://www.shutterstock.com/g/dancer

VIA SHUTTERSTOCK

DISCLOSURES:

State Street Global Advisors Worldwide Entities

State Street Global Advisors (SSGA) is now State Street Investment Management. Please go to statestreet.com/investment-management for more information.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the applicable regional regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator”) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

The views expressed in this material are the views of Chris Carpentier through the period ended October 23,2025 and are subject to change based on market and other conditions. and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Investing involves risk including the risk of loss of principal.

Investing involves risk including the risk of loss of principal.

Past performance is not a reliable indicator of future performance.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Currency Risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

Generally, among asset classes, stocks are more volatile than bonds or short-term instruments. Government bonds and corporate bonds generally have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. U.S. Treasury Bills maintain a stable value if held to maturity, but returns are generally only slightly above the inflation rate.