By: William A. Goldthwait, Portfolio Strategist

Fed cuts rates to 3.75–4%, will end QT on December 1 and shift to T-Bills. Powell signals cautious, data-driven decisions amid inflation, labor changes, and shutdown concerns.

The Federal Reserve delivered its second consecutive rate cut, trimming the federal funds rate by 25 basis points to a range of 3.75%–4.00% at the October meeting. Powell framed the move as a risk-management step rather than a signal of aggressive easing, citing softer labor conditions and still-elevated inflation. Importantly, he stressed that a December cut is “not a foregone conclusion,” a phrase that sent markets scrambling to recalibrate expectations. Treasury yields jumped and equities wavered as traders realized the Fed is not on autopilot. In short, the Fed is inching toward neutral territory but keeping its options open—because when you’re driving in the fog, you don’t hit the gas.

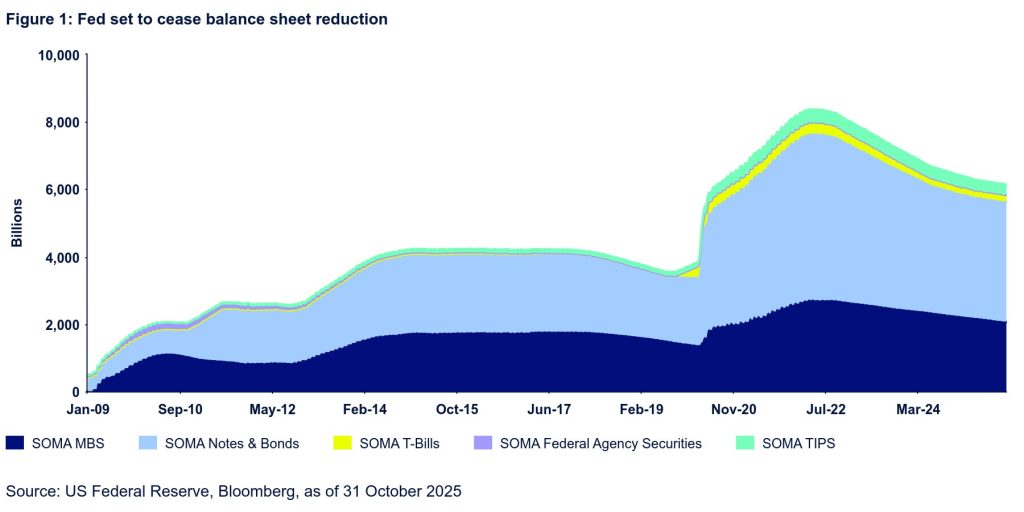

Balance sheet policy also took center stage, with Powell announcing the end of Quantitative Tightening (QT) on December 1. The Fed’s balance sheet is now roughly $2.2 trillion smaller than its peak, and now stands at $6.1 trillion. The Fed will stop letting US Treasuries roll off and now allow the MBS that pays down to be reinvested into US T-Bills, shifting the SOMA portfolio toward a more traditional composition. This pivot is designed to stabilize reserve levels and reduce funding stress, which had begun to surface in recent weeks. Powell emphasized that these changes were anticipated and align with long-term goals, but the timing underscores the Fed’s desire to maintain liquidity as uncertainty lingers. Think of it as the Fed swapping out its old workout routine for something less strenuous—still healthy, just less intense.

On the economic front, Powell painted a picture of moderate expansion, supported by resilient consumer spending, even as the government shutdown drags on and clouds visibility. Analysts estimate the shutdown is shaving about 0.2% off GDP per week, though Powell expects activity to rebound once Washington reopens. Meanwhile, inflation remains a mixed bag: goods prices are rising thanks to tariffs, housing services inflation is cooling, and services ex-housing are moving sideways. Strip out tariff effects, and core PCE sits near 2.3%–2.4%, which Powell calls “pretty good.” Of course, consumers don’t care about tariff-adjusted math—they just see higher prices and wonder why their grocery bill feels like a luxury item.

The labor market story is equally nuanced. Powell highlighted two forces at play: a drop in labor supply, partly due to lower immigration, and softer demand for workers. Despite headlines about layoffs, aggregate data like job openings and initial claims remain stable, suggesting no sharp deterioration yet. Powell doesn’t see weakness accelerating, but he acknowledged stress among lower-income consumers and certain sectors. In other words, the job market isn’t falling off a cliff, but it’s definitely not climbing any mountains either.

Adding a geopolitical twist, recent headlines about a tariff truce with China offer a glimmer of hope for easing goods inflation. While details remain fluid, any reduction in tariff pressure could help Powell’s narrative that underlying inflation is near target. Still, the Fed isn’t banking on diplomacy to do its job—policy remains data-dependent, and Powell’s tone suggests caution will dominate until the fog clears. Combine that with the prolonged shutdown, and you have a central bank navigating uncertainty with one eye on inflation and the other on employment risks.

Markets, for their part, are learning to live with ambiguity. Stocks faded and Treasury yields climbed after Powell downplayed the odds of a December cut, reminding investors that monetary policy is more debate club than autopilot. Futures still price in some chance of easing, but the bar is higher now, and incoming private labor data will be critical. For now, Powell’s message is clear: the Fed is well-positioned to respond, but don’t expect a straight line to lower rates. If you’re looking for certainty, astrology might be your best bet.

Originally posted on 5 November, 2025 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/WernerLerooy

VIS SHUTTERSTOCK

DISCLOSURES:

State Street Global Advisors (SSGA) is now State Street Investment Management. Please go to statestreet.com/investment-management for more information.

Marketing Communication

State Street Global Advisors Worldwide Entities

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without State Street Global Advisors’ express written consent.

Investing involves risk including the risk of loss of principal.

The views expressed in this material are the views of William Goldthwait through November 3, 2025 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

The value of the debt securities may increase or decrease as a result of the following: market fluctuations, increases in interest rates, inability of issuers to repay principal and interest or illiquidity in the debt securities markets; the risk of low rates of return due to reinvestment of securities during periods of falling interest rates or repayment by issuers with higher coupon or interest rates; and/or the risk of low income due to falling interest rates. To the extent that interest rates rise, certain underlying obligations may be paid off substantially slower than originally anticipated and the value of those securities may fall sharply. This may result in a reduction in income from debt securities income.

All information is from State Street Global Advisors unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Past performance is not a reliable indicator of future performance.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

These investments may have difficulty in liquidating an investment position without taking a significant discount from current market value, which can be a significant problem with certain lightly traded securities.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator” who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

© 2025 State Street Corporation – All Rights Reserved

{kind=link}

{kind=link}