By:

Michael W Arone, CFA, Chief Investment Strategist

Matthew J. Bartolini CFA, CAIA, Head of SPDR Americas Research

Anqi Dong CFA, CAIA, Senior Research Strategist

Explore how to strengthen portfolios amid uncertainty with multi-asset strategies, real assets, and gold to navigate inflation, volatility, and policy shifts.

Today’s macro forecasts — for slower growth, above target inflation, uncertain monetary policy, higher unemployment, and less global cooperation — have ratcheted up the stress on traditional portfolios.

That’s because most portfolio allocations had been made for a macro environment of rising growth, stable inflation, accommodative monetary policy, low unemployment, and global cooperation — the complete opposite of today’s.

The pivot to our new economic reality came quickly and without clarity, driven by the Trump administration’s evolving trade policy. And the increase in short-term volatility will likely continue as trade deal details are yet to be finalized.

In this environment where uncertainty is the only certainty, building resilient portfolios for a wide range of possible outcomes means diversifying differently with:

- Multi-asset allocation strategies across assets, geographies, and economic vulnerabilities.

- Multi-sector real assets across inflation sensitive markets, beyond inflation-linked bonds and commodities.

- Gold for its historically low correlations to traditional assets and history of resilience in times of market stress.1

- Ultra-short government bonds to help mitigate cross-asset drawdowns.

Past Positioning No Match for an Uncertain Future

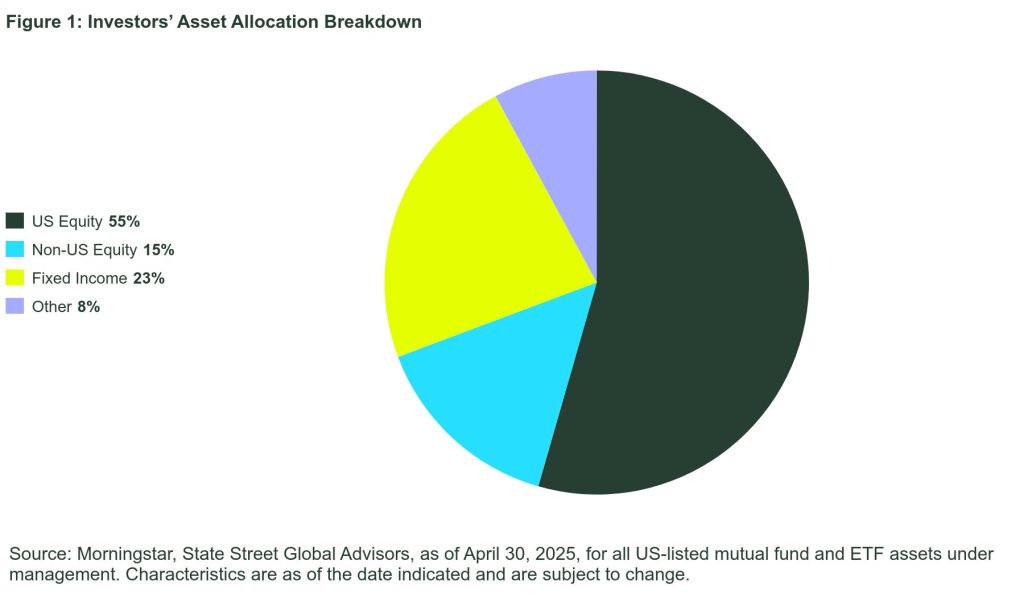

Currently, mutual fund and ETF assets are 70% concentrated in equities — with 55% in US equities (Figure 1). In recent years, this bet on equities has paid off. Equities have beaten bonds over the past decade-plus, and US equities have outperformed non-US markets in 13 out of the past full 15 calendar years.2

But the economic and fundamental foundations supporting that equity performance are shakier now. And US equities trade at a 26% premium to their long-term NTM P/E average — essentially one standard deviation above the median.3

This valuation headwind comes despite sizable growth revisions. Global earnings growth for 2025 has declined by 200 basis points compared to a US earnings growth decline of 529 basis points.4

Wide-ranging Forecasts, Negative Trends

There is a risk that the current concentration in expensively priced assets could be compounded by a wide range of possible outcomes for the economy. Text analysis from Federal Reserve policymakers’ speeches and interviews shows a trend of broader disagreement on the outlook on the economy and central bank policy. State Street Global Markets’ central bank voter disagreement barometer for the Fed has nearly doubled since the start of the year.

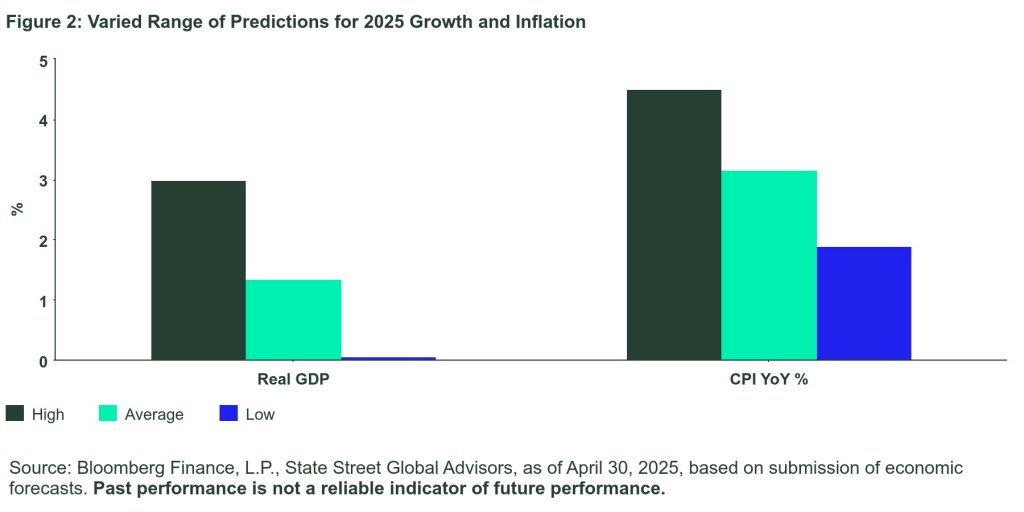

Interestingly, evolving fiscal and monetary policy also means economic data forecasts aren’t following a normal distribution. In fact, the data are more widely spread out and less concentrated around an average — or consensus (Figure 2).

Despite the lack of agreement on the economic outlook, forecast averages are trending negatively toward:

- Lower GDP: While economists’ forecasts for 2025 real GDP are between 0.3% to 3%, the average of 1.3% is lower than the growth rate of 2.8% in 2024, the 2.9% in 2023, and 2.5% in 20225— and it’s half of the long-term average GDP growth rate of 2.6%.6

- Higher Inflation: With forecasts ranging from 1.9% to 4.5%, economists expect average inflation to be 3.2% by the end of 2025. That’s up from 2.3% today.7

- Still Restrictive Fed Funds Rates: Consensus forecasts range from 4.50% to 3.25%, putting the central policy rate ending 2025 at 4% — above the 40-year long-term average of 3.5% and the rate of inflation.8

- Higher Unemployment: On unemployment there is consensus — the average rate of 4.4% forecasts a weaker labor market. Only one outlier forecast called for the unemployment rate (3.9%) to be lower than today’s 4% by the end of the year.9

Higher inflation and higher unemployment, in particular, create real challenges for the consumer. In fact, forecasted rates for inflation and unemployment by year end would bring the Misery Index (inflation plus unemployment rates) to its highest non-recession-inflicted reading since 2006.10

Soft Data Conflicts With Hard Data

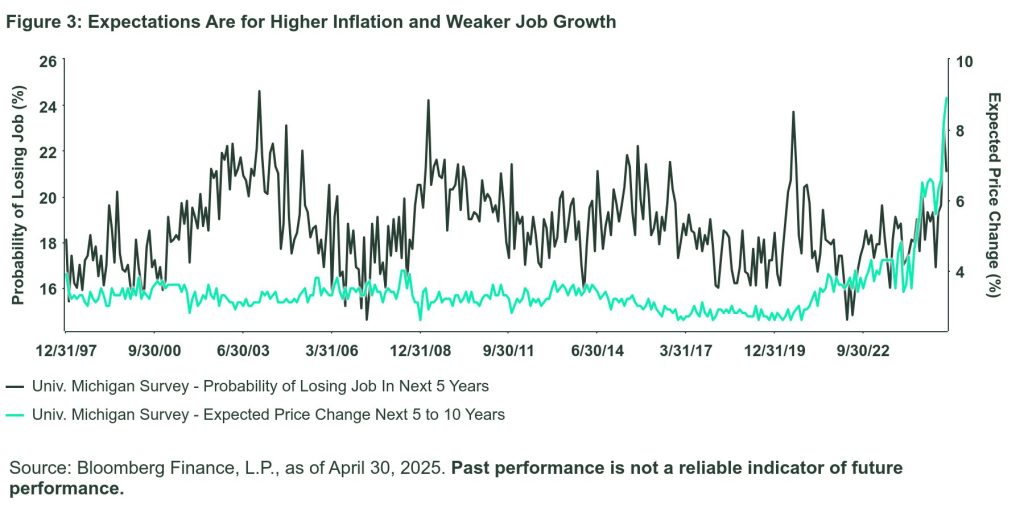

Soft data from a variety of surveys affirm this weak outlook. The University of Michigan Consumer Sentiment Index survey shows consumers’ expectations for higher prices and weaker job growth over the next five years (Figure 3).

Manufacturers are also repricing their expectations amid the raft of uncertainty. The Institute of Supply Management’s manufacturing index declined to 48 (readings below 50 indicate a contraction).11 Measures of production, orders, and employment all showed contraction. And despite the fall in energy costs, materials prices have soared to their highest level since 2022 when post-COVID supply chain shocks caused problems.12

CEO confidence also fell to its lowest level since 2012.13 And the mention of ‘headwinds’ during prepared remarks within earnings transcripts has increased each quarter for the last three.14

There is some positive soft data to offset the gloomy surveys. The AAII Investor Sentiment Survey bullish readings have bounced off their lows, while bearish readings have fallen.15

But the overall negativity of soft data has yet to show up in the hard data. Q1 earnings were better than expected around the world and positive growth is still forecast for all of 2025.16

These contradictions in the soft and hard data underscore how uncertain this environment is. While the hard data almost always lags the soft, today it’s anyone’s guess whether the hard data eventually will be better than expected, worse than expected, or as expected.

Impact of Mercantilist Policy

The Trump administration’s Liberation Day tariff surprise sparked a trade war and global slowdown. In the past, other tariffs also have sought to protect national security and champion high-value, strategic industries — though they tended to be enacted through subsidies and legislative acts, not mercantilist policies. Think of the CHIPS Act and semiconductors. Through this lens, the administration’s trade policy wasn’t the catalyst of shifts in growth, inflation, sentiment, and global cooperation — it just accelerated them.

While markets have rebounded from April lows, tariff uncertainty — whether they’ll be lower than first proposed, delayed further, or include additional levies to sectors — continues to impact sentiment. And it may be more difficult for the ‘big, beautiful tax bill’ to provide relief now that Moody’s has downgraded the US credit rating.

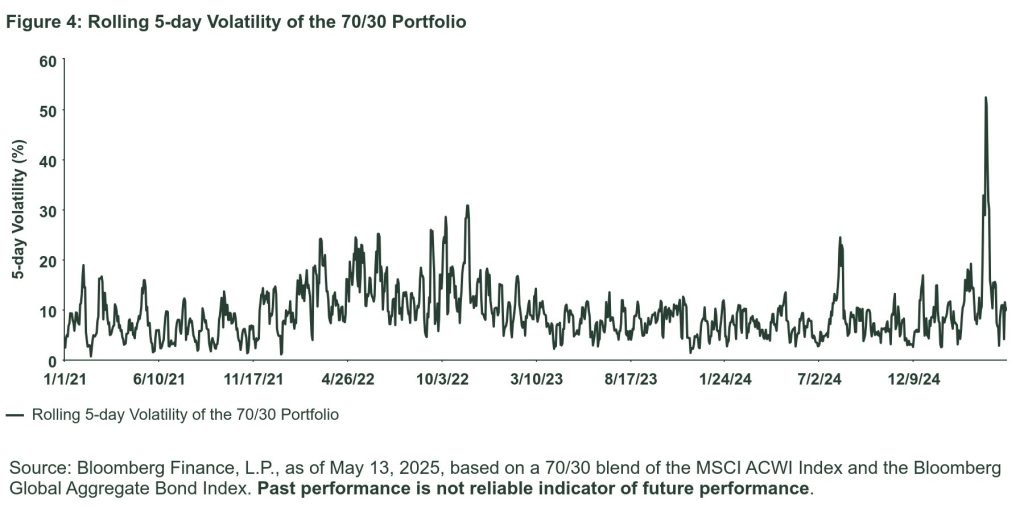

Given the likelihood of higher tariffs on all US trading partners, more coercion to reach national goals, and increased constraints on US monetary policymakers, portfolios positioned for equities to continue as the dominant asset class in a low volatility environment are at risk. In fact, 70/30 portfolios with a rising growth bias saw sizable spikes of volatility this spring (Figure 4).

How to Build Portfolio Resilience Amid Uncertainty

Step one to strengthening portfolios to withstand the current volatility is adding a global multi-asset strategy allocated across economic environments, assets, and geographies to help:

- Diversify away from focusing only on rising growth/falling inflation assets.

- Extend the asset allocation mix beyond stocks and nominal bonds.

- Reduce the US equity bias at a time when US assets have more to lose than gain from the shift toward more mercantilist polices and away from global cooperation.

Next, consider real assets like gold, inflation-linked bonds, commodities, infrastructure, natural resources, and real estate. Added individually or grouped together as part of a multi-sector real return strategy, real assets may help hedge inflation volatility amid the wide, but upward-biased, range of outcomes.

Given that equity volatility tends to rise more quickly in response to stock prices falling than it falls in response to stock prices rising, gold could help mitigate equity volatility jump risk in the event of a fiscal or monetary policy mistake.

Finally, ultra-short government bonds can help safeguard portfolios from a cross-asset widening of risk premiums in the event of the unexpected, from a liquidity shock to a profound policy mistake.

Originally posted on June 2, 2025 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/tadamichi

VIA SHUTTERSTOCK

FOOTNOTES AND SOURCES

1 Bloomberg Finance, L.P., as of May 13, 2025, from data from 1994 to 2025 using monthly frequencies. Gold = Gold Spot versus MSCI ACWI Index and Bloomberg US Aggregate Bond Index.

2 Bloomberg Finance, L.P., as of May 13, 2025, based on returns for the MSCI ACWI Index and the Bloomberg Global Aggregate Bond Index, as well as returns on the S&P 500 Index versus the MSCI World Ex-US Index.

3 Bloomberg Finance, L.P., as of May 13, 2025, based on the S&P 500 Index next-twelve-month-earnings-ratio compared to the 40-year average ratio.

4 Bloomberg Finance, L.P., as of May 13, 2025, based on the S&P 500 Index and MSCI ACWI Index 2025 earnings-per-share growth estimates.

5 Bloomberg Finance, L.P., as of May 13, 2025.

6 Bloomberg Finance, L.P., as of May 13, 2025, based on the 50-year average.

7 Bloomberg Finance, L.P., as of May 13, 2025, based on economist forecasts.

8 Bloomberg Finance, L.P., as of May 13, 2025, based on economist forecasts.

9 Bloomberg Finance, L.P., as of May 13, 2025, based on economist forecasts.

10 State Street Global Advisors, Bloomberg Finance, L.P., as of May 13, 2025, based on economist forecasts.

11 Bloomberg Finance, L.P., as of May 13, 2025.

12 Bloomberg Finance, L.P., as of May 13, 2025.

13 Bloomberg Finance, L.P., as of May 13, 2025.

14 Bloomberg Finance, L.P., as of May 13, 2025, based on earnings transcripts of firms in the Russell 1000 Index.

15 Bloomberg Finance, L.P., as of May 13, 2025.

16 Bloomberg Finance, L.P., as of May 13, 2025, based on MSCI ACWI Index.

DISCLOSURES

The views expressed in this material are the views of Michael Arone, Matthew Bartolini, and Anqi Dong through the period ended May 14, 2025, and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

Past performance is not a reliable indicator of future performance.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

Investing involves risk including the risk of loss of principal.

Diversification does not ensure a profit or guarantee against loss.

Frequent trading of ETFs could significantly increase commissions and other costs such that they may offset any savings from low fees or costs.

Passively managed funds invest by sampling the index, holding a range of securities that, in the aggregate, approximates the full Index in terms of key risk factors and other characteristics. This may cause the fund to experience tracking errors relative to performance of the index.

Asset Allocation is a method of diversification which positions assets among major investment categories. Asset Allocation may be used in an effort to manage risk and enhance returns. It does not, however, guarantee a profit or protect against loss.

Investing in commodities entails significant risk and is not appropriate for all investors.

See the section ‘Important Risk Disclosures’ here for further disclosures.