By: Aaron R. Hurd, FRM, Senior Portfolio Manager

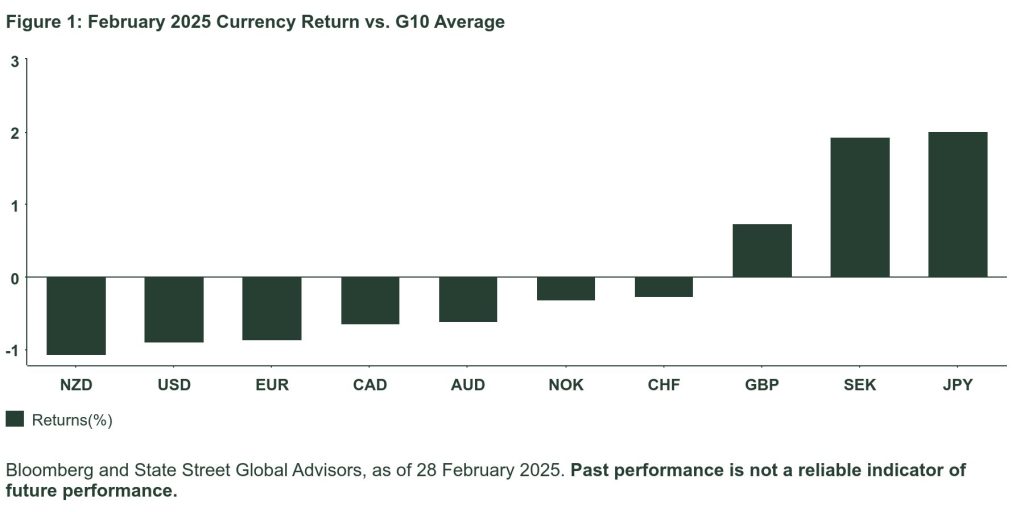

Cracks began to emerge in the bullish USD story during February as poor retail sales and plunging services PMI reinforced negative fiscal headlines. Tactically, we are now positive on SEK and turned neutral on EUR.

We highlighted signs of US dollar weakness on the horizon last month, but now that horizon appears much closer, and the signals are even clearer. The highly publicized fiscal cuts in the Department of Defense and projected cuts in the proposed budget moving through Congress are likely to weigh on US growth expectations and the dollar going forward. In contrast, the European Union (EU) has proposed up to 800 billion euro in defense spending, alongside Germany’s proposed 500-billion-euro infrastructure fund and an additional 1% increase in defense spending. These are game-changing amounts.

Despite this, we would not count the US dollar out just yet. US growth, while slower, does not appear poised to fall off a cliff, and most of the negative news has come from sentiment indicators rather than hard economic data. More importantly, tariffs will be an increasingly significant and US dollar-supportive factor in April. The current euro rally could easily extend another 2–4% before tariff risks and concerns over the specifics of fiscal spending cause a setback.

The British pound is also benefiting from positive momentum, but the recent improvements in UK retail sales and employment data do not look sustainable; we continue to see risks tilted toward the downside for Bank of England (BoE) policy rates and pound this year.

The Swedish krona has had a strong run but is nearing overbought territory, given EU tariff risks and potential delays in defense spending. The Australian dollar remains undervalued against long-term measures and relative interest rates, with decent fundamentals, stable—though below-potential—growth, strong labor markets, and a likely slow pace of Reserve Bank of Australia (RBA) easing. However, we would limit long Australian dollar positions at this time to account for its high sensitivity to China tariffs and rising equity market risks.

The yen looks overbought in our model but remains a favorite for 2025. Weaker US growth and high Japanese inflation should continue to compress the negative carry, pushing the yen higher. Importantly, the yen is also exhibiting more stable safe-haven behavior, outperforming when equities fall and equity volatility rises. Consider going long on the yen against the Swiss franc for a lower-beta, lower-carry expression of a bullish yen view.

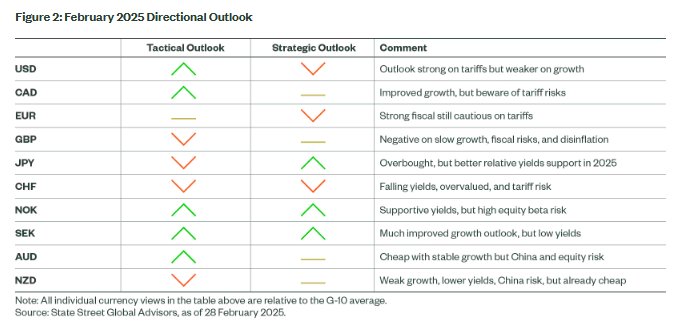

US Dollar (USD)

The US dollar remains one of the top-ranked currencies in our model, but our positive US dollar outlook is softening as US economic data continues to underperform and US yields decline. The negative GDP impact of Trump’s policy agenda is expected to manifest before any positive effects, but even so, the US is still poised to be one of the higher-growth, higher-yield countries in the G10 in the near term.

However, we would not count the dollar out just yet. We expect Trump will impose significant tariffs on the EU and additional sectoral tariffs in April. As a result, we view the recent US dollar weakness as a correction—a justified one— but not yet the beginning of a sustained downtrend. For that, we would likely need to see a more significant deterioration in US economic health and a reduction in tariff-related uncertainty.

Our long-term outlook remains unchanged. We have consistently maintained that the US dollar is likely to decline by at least 15% over a two year horizon, as US yields and growth revert to the G10 average, and the US continues to contend with significant fiscal and current account deficits.

If historical patterns hold, any stimulus introduced by Trump is likely to accelerate the accumulation of US debt, which would lead to a more challenging long-term outlook for the US economy, corporate earnings, and the US dollar. For investors with an investment horizon of over two years, we favor short US dollar positions.

Canadian Dollar (CAD)

Improved economic data has pushed our Canadian dollar forecast higher, making it the top ranked currency in the G10 as of month-end. However, it is challenging for the models to capture the tariff impact. President Trump’s decision to follow through with the tariffs introduces the risk of a material slowdown in economic activity, which could pressure the currency to 1.47 or even 1.50 if the tariffs remain in place for a while.

That said, we still believe Trump will lift the tariffs after a short period, as they do little to benefit the US economy, and targeting Canada is unlikely to appeal to US voters. And lingering trade war threats, even if the current tariff is lifted quickly, is likely to weigh of Canadian sentiment and growth.

Thus, we see the Canadian dollar largely in a 1.44–1.48 range with a bias toward the top end of the range against the US dollar over the very near term. Later this year, we expect USD/CAD to fall back into the high 1.30s as clarity on tariffs and the United States–Mexico–Canada Agreement (USMCA) improves, and as we begin to see greater growth benefits from the Bank of Canada’s aggressive rate cuts and a moderation in US growth and yields.

Euro (EUR)

Our tactical outlook for the euro has stabilized at a neutral level. While household balance sheets are strong, unemployment is low, real wage growth is positive, and the need for increased defense spending and the proposed 500-billion-euro German infrastructure fund are positive for the euro. Meanwhile, growth remains stagnant, with little evidence of a catalyst to encourage consumer spending. In the long term, potential growth is weak, and Trump has made it clear that he intends to apply further pressure through tariffs next month.

The European Central Bank (ECB) is on track for a sub-2% policy rate in 2025. While the euro could extend its recent gains, it is more likely to retreat, possibly even back to its range lows around 1.03 versus the US dollar, depending on the intensity of the US trade war.

The massive proposed fiscal stimulus is a game changer from a long-run perspective and both limit euro downside in the face of tariffs and help it recover more durably after any tariff shock.

British Pound (GBP)

We are bearish on the pound over the short and medium terms. While the British pound looks better in terms of tariff risk, the recent improvement in retail sales and employment data does not seem sustainable. The increase in the National Insurance (NIH) payroll tax in early April is likely to contribute to a further softening of labor markets and household demand.

The UK has avoided direct threats of US tariffs, given its trade deficit with the US, but weaker regional growth resulting from US tariffs will likely have a negative spillover effect in the coming months. Although the recent fall in yields provides some relief, the increased issuance of government debt to fund the budget is likely to keep investors wary of fiscal risk. The UK cannot match the massive stimulus proposed in the EU and Germany.

Our long-run valuation model has a more positive pound outlook as the currency screens as cheap to fair value. But we expect sticky inflation and chronically weak potential growth post-Brexit to likely weigh on fair value somewhat limiting that potential pound upside over the next several years.

Japanese Yen (JPY)

Our model suggests the yen is overbought following its rapid appreciation in January and February. While we respect the potential for a near-term retracement lower in the yen, we remain more positive on it over the course of the year. We see plenty of room for the interest rate differential to continue to compress in the yen’s favor, and the yen has regained its appeal as a safe-haven currency, reliably outperforming in times of equity market stress.

Weaker global growth, led by the US, and tariff risks suggest room for further monetary easing while high inflation, strong wages, and the recent pick up in growth support further Bank of Japan rate hikes.

We continue to favor expressing our medium-term positive view through long positions in yen versus franc in the short term, given still high US yields and potential US dollar upside risks from tariffs. Short euro and pound against the yen also look attractive, albeit with a negative drag from carry.

The risk to this view is a broad reacceleration in US and global growth and inflation that drives US yields to new highs. Even then, while the yen may struggle against the US dollar, it is likely to easily outperform currencies of regions with subpar growth, particularly in Europe.

Swiss Franc (CHF)

We remain negative on the franc over both the tactical and strategic horizons. The franc is the most expensive G10 currency, according to our estimates of long-term fair value, and it has the lowest yields and core inflation in the G10. At the same time, the real trade-weighted franc is in the upper half of its 30-year range, and the Swiss National Bank (SNB) is cutting rates.

We expect the SNB to become more open to direct currency market intervention to weaken the franc once the policy rate falls below its current level of 0.50%. In fact, considering that a major source of the undershoot in inflation is directly related to franc strength through import prices, we believe it makes sense for the SNB to shift focus away from rate cuts and toward a weak currency policy.

To make matters worse, President Trump has explicitly mentioned tariffs on the pharmaceutical sector, a key Swiss export sector. Overall, we see the franc transitioning toward a prolonged reversion back to our estimate of its long-term fair value.

Norwegian Krone (NOK)

Our tactical view remains positive for the krone, driven by relatively high yields and stronger local equity performance. Expected monetary easing in 2025 could reduce yield support, but the krone is likely to retain yields well above the G10 average while the growth outlook remains modestly positive, especially when compared to regional neighbors like the EU and UK.

Longer-term forces also favor the currency. Despite our modestly constructive view, we caution that the recent drop in oil prices and increased equity market volatility may introduce greater risk for the krone, which tends to have a high beta to both oil prices and equity market sentiment.

In the long term, the krone is historically cheap relative to our estimates of fair value and is supported by steady long-run potential growth and a strong balance sheet. While we remain net positive on the Krone, we acknowledge material short-term risks. Oil prices have trended lower since mid-January, and the krone has shown sensitivity to global risk sentiment, which is likely to be more volatile given high equity valuations, growth struggles across much of the G10, and high US policy uncertainty.

Swedish Krona (SEK)

We shift to a modestly positive bias on the krona over the short term, driven by improved economic data and higher inflation. Long-term, we are more constructive. The upside surprise in CPI and a strong bounce back in Q4 GDP (+2.4% YoY vs. 1.1% expected) bode well for the currency, pushing Sweden’s composite economic growth score to the best in the G10.

Markets expect another 1–2 rate cuts from the Riksbank this year, bringing yields down to 1.75–2%, which is close to the expected rate for the ECB by year-end. Additionally, the market is now expecting three cuts from the Fed. However, the krona faces near-term risks. High US tariffs on the EU, promised for April, will almost certainly slow Swedish growth, and pricing in a surge from EU defense spending may be premature.

In the long term, the currency is very cheap relative to its long-run fair value. If the recent growth recovery continues and tariff risks are resolved (or more fully priced in), the krona has ample room to continue its recovery.

Australian Dollar (AUD)

We are slightly positive on the Australian dollar due to stable, albeit below-trend, growth, strong labor markets, and relatively high yields. However, we anticipate that the Australian dollar will struggle against the US dollar at least through mid-March due to heightened equity volatility and tariff risks. Beyond that, there are many positive aspects for the Australian dollar. Labor markets remain strong, household consumption has materially improved, the fiscal stance is supportive, and YoY core inflation is sticky near the top of the band. Given this context, a serious dovish shift in monetary policy seems unlikely.

Additionally, Australia’s direct exposure to US tariff risks is moderate. Direct exports to the US are minimal, and the knock-on effects from Chinese demand may be muted if tariffs prompt China to increase fiscal stimulus, which could benefit exports like iron ore.

In the long term, the Australian dollar outlook is mixed. The currency is cheap compared to the US dollar, pound, euro, and franc, with room to appreciate, but it is expensive against the yen and Scandinavian currencies.

New Zealand Dollar (NZD)

Our tactical model shifted to a negative outlook on the New Zealand dollar. The benefit of New Zealand’s high yield has diminished as the RBNZ continues to ease policy in response to disinflation and recessionary conditions. Ongoing growth challenges and a weak external balance (with the current account at -6.7% of GDP) are likely to keep the New Zealand dollar depressed. On a more positive note, the significant sell-off in the New Zealand dollar over the past four months already reflects a discount for lower growth and yields, which may limit further losses.

In the long term, our outlook is mixed. Our estimates of long-term fair value suggest that the New Zealand dollar is cheap against the US dollar and Swiss franc and has room to appreciate, but it is expensive against the yen and Scandinavian currencies.

Originally posted on March 13, 2025 on SSGA blog

PHOTO CREDIT : https://www.shutterstock.com/g/mayk.75

VIA SHUTTERSTOCK

DISCLOSURES

Marketing Communication

State Street Global Advisors Worldwide Entities

Investing involves risk including the risk of loss of principal. All material has been obtained from sources believed to be reliable.

There is no representation or warranty as to the accuracy of the information and State Street shall have no liability for decisions based on such information.

Currency Risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

The views expressed in this material are the views of the Aaron Hurd through the period ended 02/28/2025 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

This document may contain certain statements deemed to be forward-looking statements. All statements, other than historical facts, contained within this document that address activities, events or developments that SSGA expects, believes or anticipates will or may occur in the future are forward-looking statements. These statements are based on certain assumptions and analyses made by SSGA in light of its experience and perception of historical trends, current conditions, expected future developments and other factors it believes are appropriate in the circumstances, many of which are detailed herein. Such statements are subject to a number of assumptions, risks, uncertainties, many of which are beyond SSGA’s control. Please note that any such statements are not guarantees of any future performance and that actual results or developments may differ materially from those projected in the forward-looking statements.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator”) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged. Past performance is not a reliable indicator of future performance. Assets may be considered “safe havens” based on investor perception that an asset’s value will hold steady or climb even as the value of other investments drops during times of economic stress. Perceived safe-haven assets are not guaranteed to maintain value at any time.

{kind=link}