By: Dane Smith, Chris Carpentier and Christine Norton

Small caps underperform as yields rise due to higher financing costs and limited ability to refinance debt compared to large caps. While large caps locked in lower rates earlier, small caps may face refinancing at higher rates, affecting their bottom line.

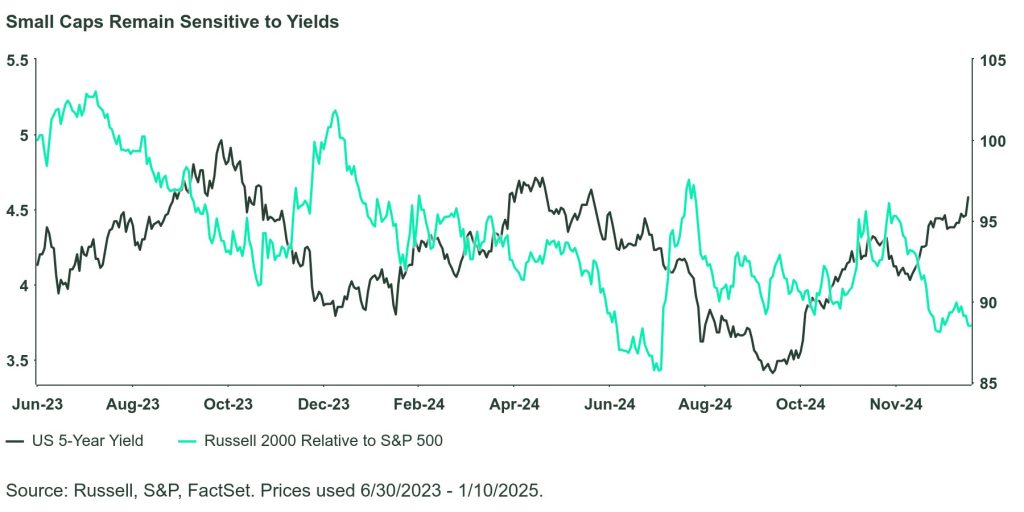

The chart below illustrates moves of the 5 year yield compared to the relative returns of the Russell 2000 index vs the S&P 500, highlighting the relationship between small vs large cap equities and interest rates. An inverse relationship is evident – small cap stocks tend to underperform as yields rise. A little over a month ago the 5 year yield was around 4% and has since climbed to almost 4.6%. And during this time we’ve seen small caps lag.

Higher interest rates mean higher costs to finance operations. This affects small caps more for two reasons. First, since small caps are generally more risky, they already start with a higher cost of debt. Second, small caps are usually unable to refinance and lock in long term debt in the same way as large caps. For instance, some large caps were able to issue 10-year bonds a few years ago when rates were low, locking in this low cost over a long period. Many small caps, however, need to roll their debt over every 3–5 years, meaning they are closer to refinancing at current higher rates, which will directly affect their bottom line.

For 2025, while we do have a preference for US large caps, we also expect a rounding out of earnings to other sectors of the market. Should unemployment remain low and economic growth remain healthy, this may allow small caps to perform to higher expectations.

Originally published on January 20, 2025 on SSGA blog

PHOTO CREDIT: https://www.shutterstock.com/g/oland

VIA SHUTTERSTOCK

DISCLOSURES:

Marketing Communication

ssga.com

State Street Global Advisors Worldwide Entities

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the applicable regional regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the “appropriate EU regulator”) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication.

The views expressed in this material are the views of Dane Smith, Christopher Carpentier, Christine Norton, and Devin Foster, through the period ended January 16, 2025 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Investing involves risk including the risk of loss of principal.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Currency Risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

Generally, among asset classes, stocks are more volatile than bonds or short-term instruments. Government bonds and corporate bonds generally have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. U.S. Treasury Bills maintain a stable value if held to maturity, but returns are generally only slightly above the inflation rate.

© 2025 State Street Corporation. All Rights Reserved.

{kind=link}