Like so many of us, I’m operating on a significant sleep deficit. As I write this, we are still awaiting clarity about the ultimate winner of the Electoral College vote and the battle for Senate control remains in the air.

Yet the markets are clearly voting “Yea”, in the face of all this uncertainty. There are so many swirling factors affecting markets right now that a series of bullet points is the best way that I can explain what we are seeing and what we might see going forward.

- Conventional market wisdom for post-election trading stinks. It didn’t work in 2016, and it’s not working today. Markets were said to be dreading an uncertain outcome with the potential for a contested election. That is exactly what we have at the moment, yet markets don’t care.

- That said, markets tend to like divided control between the House, Senate and Presidency. That appears to be a likely scenario at the moment.

- The Blue Wave idea is dead and so are the investment themes that were predicated upon it. Yesterday I wrote about the recent outperformance of value versus growth stocks based upon hopes of massive fiscal stimulus, and how that trade has proven to be yet another “widow maker”. It certainly is not working out for traders this morning.

- Banks are among the day’s losers, partly because of the move away from value stocks, partly because bond yields have plunged as fiscal stimulus hopes diminish. That also means that the Federal Reserve may need to be more forthcoming with monetary stimulus, including yield curve control. Bank stocks benefit from a steeper yield curve, so the flattening curve is not helpful to their stock prices.

- Investors love tech. When times are uncertain, investors tend to revert to the playbook that worked for them. Buying big cap tech stocks has proven to be a winning strategy, and it’s winning once again. One tech investing theme is that lower interest rates boost stock valuations, especially if those valuations are rich. They just got richer.

- Tech stocks are likely benefitting from the reduced fears of a major capital gains tax increase. Vice President Biden made it clear that he is in favor of raising capital gains tax rates to match those of ordinary income. Even if he prevails in the Electoral College, it is unlikely that he will have sufficient Senate support for such a move. Considering that tech stocks have performed best, it is reasonable to assume that taxable investors would have been incentivized to sell those shares before year-end. That removes some potential overhang from these shares.

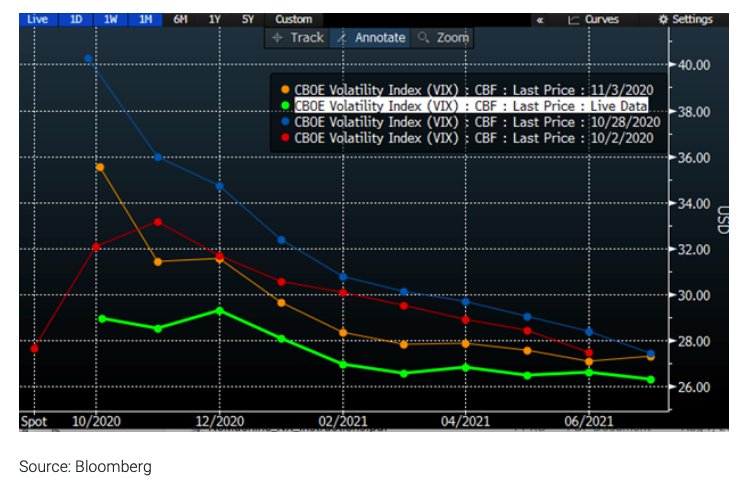

- VIX is sharply lower today, but the futures curve is telling us that we are not out of the woods yet. As we can see from the graph below, today the whole VIX complex is well below recent levels (green line vs. recent counterparts). The extreme backwardation that we saw last week and yesterday (blue, orange) is behind us. Yet we still see a peak for the VIX futures curve in December and November remains firm. The stock markets seem to be unconcerned that a contested election could bring volatility. The volatility markets don’t fully share that sanguine outlook

Source: Bloomberg

- Wither the Fed? In a normal week, the focus would be on a 2-day Federal Reserve meeting. Chairman Powell is scheduled to give a press conference tomorrow afternoon. It seems unlikely that he would wade into an uncertain election and explicitly resume his push for fiscal stimulus. With that backdrop, will he be able to provide the type of clarity that the markets desire? We have seen markets reverse during and/or after Fed meetings several times in the recent past. Will he be able to stave off that pattern tomorrow?

Photo Credit: Democracy Chronicles via Flickr Creative Commons

DISCLOSURE: INTERACTIVE BROKERS

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}

{kind=link}