By: Michael Kramer

We have the Federal Reserve meeting on Wednesday, followed by the European Central Bank (ECB) meeting on Thursday. Meanwhile, the Bank of Japan (BOJ) made waves last Friday by raising its policy rate to 50 basis points, signaling that they are far from finished tightening. This move is significant because Japan has spent decades in a deflationary environment, and even small rate increases are a big deal. BOJ Governor Kazuo Ueda has suggested that Japan’s neutral rate might be around 1%, meaning we could see another 50 basis points of hikes throughout 2025. This marks a significant shift for Japan, a global low-rate anchor.

The yen has weakened substantially against the dollar, euro, and other major currencies, which has historically supported carry trades and added liquidity to global markets. However, the narrowing basis swap spreads for USD-JPY suggest that this trend may be unwinding.

Rising rates in Japan could also put upward pressure on global bond yields. Japan’s role as the world’s low-rate anchor is shifting, and if that base begins to lift, it could ripple through markets.

Here in the U.S., the week is packed with economic data. We’ll see new home sales, durable goods orders, and the S&P CoreLogic Home Price Index on Monday. Tuesday brings consumer confidence data and the Richmond Fed survey at 10 AM. The big event, however, will be Wednesday’s Federal Reserve meeting. While the market isn’t expecting any changes to interest rates, I believe the Fed would be wise to avoid signaling any cuts in the near term.

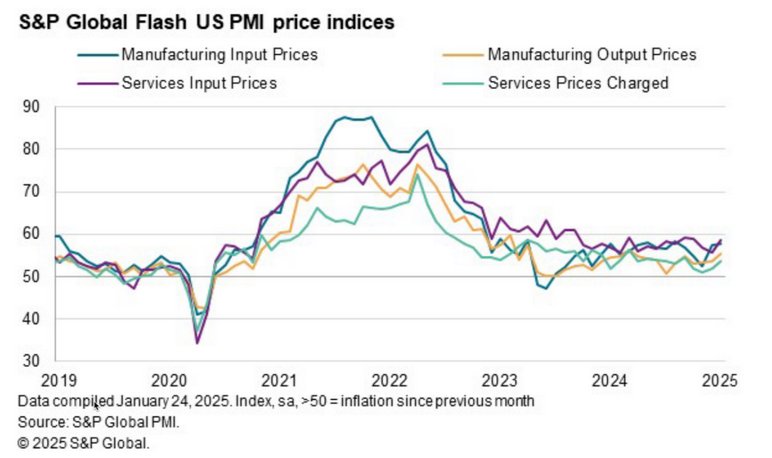

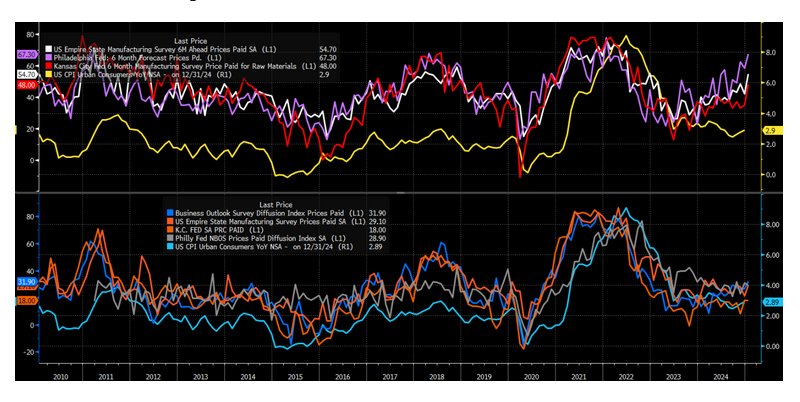

Inflation remains a concern, and recent data suggest that it may accelerate. For instance, the S&P Global report released on Friday indicated a pickup in inflation and hiring activity.

Many corporate surveys also point to rising inflation expectations over the next six months, a key indicator of where the inflation might be headed.

Even the University of Michigan’s five-to-ten-year inflation outlook remains elevated at 3.2%, near the higher end of its historical range. If I were in the Fed’s shoes, I’d view this as an uncomfortable position, as it signals that inflation expectations haven’t fully stabilized.

Thursday will bring the advance GDP report, with the market expecting 2.7% quarter-over-quarter growth. Personal consumption is projected to grow by 3.2%, and the price index is expected to increase by 2.5%. Together, that indicates a strong nominal growth rate of 5.2%. We’ll also get the core PCE price index for Q4, which previews Friday’s monthly PCE report. While the quarterly and monthly figures are related, they don’t always align perfectly, so any surprises on Thursday may not necessarily translate into Friday’s numbers.

On Friday, we’ll see the Employment Cost Index (ECI), expected to rise from 0.8% to 0.9%, reflecting accelerated wage growth in Q4. The monthly PCE inflation report will also be released, with estimates pointing to a 0.3% month-over-month increase, up from 0.1% in the prior month. The year-over-year core PCE is expected to remain steady at 2.8%. Notably, market expectations for core PCE were revised lower following the recent CPI and PPI reports. Still, the market has become adept at predicting these figures based on prior inflation data.

Earnings season also ramps up this week. Microsoft, Meta, Tesla, and Apple are all reporting after the close on January 29th and 30th, while Alphabet is scheduled for next week. Implied correlations in the S&P 500 have been falling, with the one-month implied correlation index hitting 7.6 on Friday—the second-lowest level ever recorded. This trend aligns with earnings season, where implied correlations typically drop as individual stock volatility rises ahead of earnings announcements. However, as we exit earnings season, implied correlations tend to rise, which could signal increased market risk.

Historically, low implied correlations have coincided with market tops. As correlations rise and earnings season winds down, we may see heightened market volatility, particularly with the Fed meeting and key economic data releases on the horizon.

Additionally, the Treasury General Account (TGA) has risen sharply in recent weeks, draining liquidity from the financial system. Reserve balances have fallen as the TGA climbs to around $760 billion, adding another layer of potential pressure on markets.

From a broader perspective, the risk-reward balance in equities appears skewed. With tightening liquidity, low implied correlations, and potential for a more hawkish Fed outlook, the upside for equities seems limited compared to the downside risks.

Forward markets suggest that rates may rise slightly over the next 12–18 months, contrary to expectations of cuts. This reinforces the idea that the Fed is likely not done tightening and could surprise markets later in 2025.

Originally posted on January 26, 2025. For more data charts, see Mott Capital blog

PHOT CREDIT : https://www.shutterstock.com/g/limbi007

VIA SHUTTERSTOCK

FOOTNOTES

(TERMS BY CHAT GPT)

1. Carry Trade:

A strategy where investors borrow money in a currency with low interest rates and invest it in assets denominated in a currency with higher interest rates to profit from the difference.

2.Basis Swap Spreads:

A financial metric that reflects the cost of swapping interest rate payments between two currencies. Narrowing spreads often indicate tighter market conditions or reduced risk in currency swaps.

3.Core PCE (Personal Consumption Expenditures) Price Index:

A key inflation measure used by the Federal Reserve that excludes volatile food and energy prices, providing a more stable view of underlying inflation trends.

4.Employment Cost Index (ECI):

A quarterly measure of total employee compensation, including wages and benefits, that indicates trends in labor costs and wage inflation.

5.Implied Correlation Index:

A measure of how correlated the price movements of individual stocks are with the broader market index. Low implied correlation suggests stocks are moving more independently, often seen during earnings season.

6.Implied Volatility:

The market’s expectation of future price fluctuations, derived from the pricing of options. Higher implied volatility generally reflects increased uncertainty or risk.

7.Liquidity:

The availability of cash or assets that can be quickly converted to cash. In financial markets, it often refers to the ease of buying or selling assets without significantly affecting their price.

8.Nominal Growth Rate:

The growth rate of the economy measured without adjusting for inflation, reflecting the total dollar value of goods and services.

9.Forward Market:

A financial market where contracts are made to buy or sell assets at a predetermined price on a future date. Forward rates often indicate market expectations for interest rates or currency movements.

10.Treasury General Account (TGA):

The U.S. Treasury’s primary operating account held at the Federal Reserve. Movements in the TGA can influence liquidity in the financial system.

DISCLOSURES:

Charts used with the permission of Bloomberg Finance L.P. This report contains independent commentary to be used for informational and educational purposes only. Michael Kramer is a member and investment adviser representative with Mott Capital Management. Mr. Kramer is not affiliated with this company and does not serve on the board of any related company that issued this stock. All opinions and analyses presented by Michael Kramer in this analysis or market report are solely Michael Kramer’s views. Readers should not treat any opinion, viewpoint, or prediction expressed by Michael Kramer as a specific solicitation or recommendation to buy or sell a particular security or follow a particular strategy. Michael Kramer’s analyses are based upon information and independent research that he considers reliable, but neither Michael Kramer nor Mott Capital Management guarantees its completeness or accuracy, and it should not be relied upon as such. Michael Kramer is not under any obligation to update or correct any information presented in his analyses. Mr. Kramer’s statements, guidance, and opinions are subject to change without notice. Past performance is not indicative of future results. Neither Michael Kramer nor Mott Capital Management guarantees any specific outcome or profit. You should be aware of the real risk of loss in following any strategy or investment commentary presented in this analysis. Strategies or investments discussed may fluctuate in price or value. Investments or strategies mentioned in this analysis may not be suitable for you. This material does not consider your particular investment objectives, financial situation, or needs and is not intended as a recommendation appropriate for you. You must make an independent decision regarding investments or strategies in this analysis. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Before acting on information in this analysis, you should consider whether it is suitable for your circumstances and strongly consider seeking advice from your own financial or investment adviser to determine the suitability of any investment.

{kind=link}