By: Samuel Rines , Macro Strategist (Model Portfolios)

Key Takeaways

- The U.S. economy has slowed steadily throughout the year, with GDP growth decreasing from 3% in the first quarter to 2.1% in the third quarter, which aligns with pre-COVID norms.

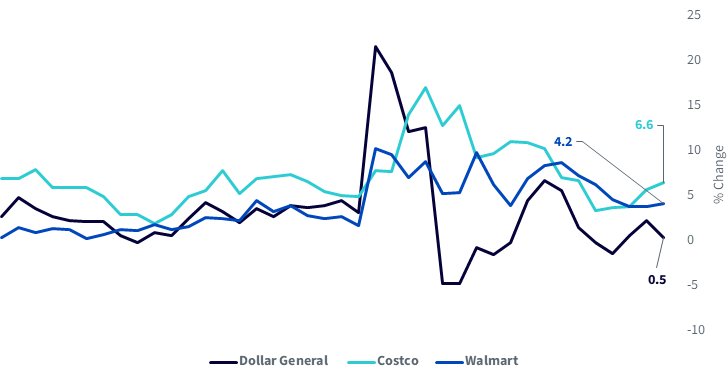

- Retail performance varies, with Dollar General showing weakness, while major retailers like Walmart and Costco report stable or increasing sales, signaling resilience in consumer spending.

- The economic slowdown reflects a normalization after years of volatility, particularly in sectors like rural America, and should not be seen as alarming.

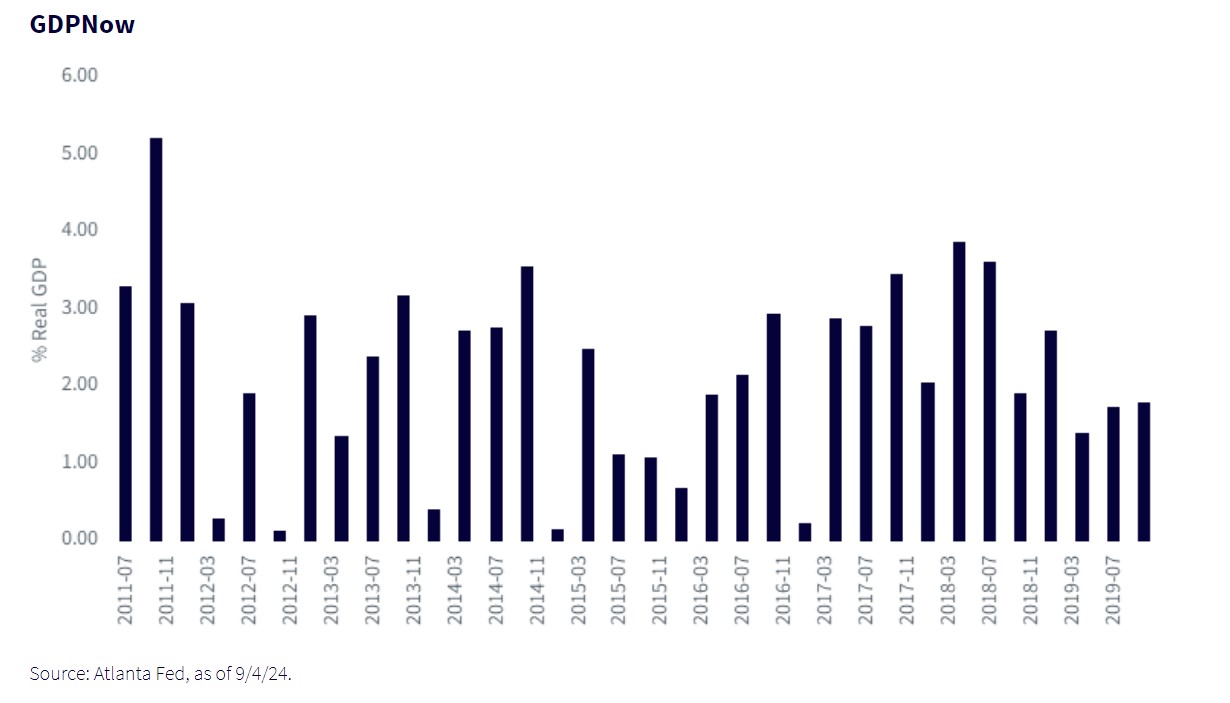

The U.S. economy has slowed. But “slowed” requires a bit of context. There is no shortage of ways to parse the economic outlook, and—with the benefit of hindsight—point out the places and times the variables appear to have broken. In some circumstances, that may be a useful exercise. Most of the time, it is not. It is important to note where the economy has been only in the context of where it may be going. Thankfully, there is the Atlanta Fed’s GDPNow metric. It is a sort of “wayback” machine for the U.S. economy.

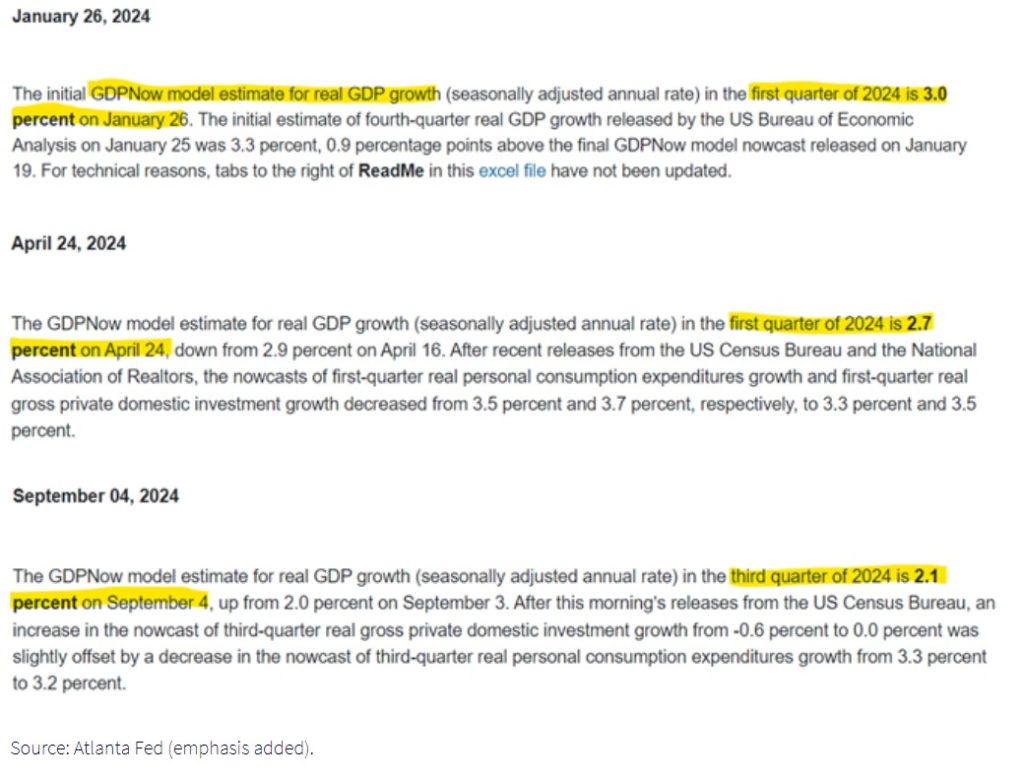

In late January, the GDPNow Model for the first quarter—basically, a pseudo real-time estimate of GDP growth—was showing a 3% growth rate. That was the initial estimate for growth in the first quarter. By the time the quarter closed, it was down to 2.7%. Today, the estimate for the third quarter is 2.1% growth. The takeaway is straightforward: there has been a slow and steady deceleration from the beginning of the year to today.

GDPNow

What does 2.1% real GDP growth mean? Looking at the pre-COVID period (from the beginning of the GDPNow dataset), the average quarter-end reading was 2.1%. That perspective matters only in framing the current outlook. The current slowdown is not all that disturbing within this context. It might even be described as normal. And, after the last four years, ”normal” is a strange thing for the economy.Not to mention, there have been plenty of one-off earnings reports to raise eyebrows about the health of the U.S. consumer and economy. The comments from Dollar General pointed to their core consumers, those making under $35,000, being under pressure. That should not be ignored, but it should also be heavily caveated. Dollar General has not exactly been one of the better operators in the post-COVID era.

Same Store Sales Last 10-Years

In the grand scheme of retail, Dollar General’s comments are only potentially important on the margin. Costco and Walmart are having none of it. In fact, they are going in the opposite direction with either stable or accelerating comparable sales. The combination of Walmart and Costco increasing their sales is far more important than Dollar General’s comments. Taking Dollar General as a signal of a broad economic problems would have sent numerous false positives. Incorporating a wider swathe of retailers would have avoided these issues. That is likely the case today.

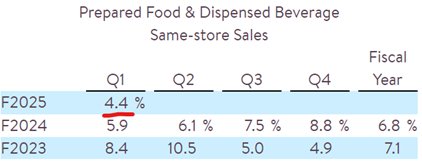

Casey’s General Store is a gas station. That also happens to be the fifth- largest pizza company in the U.S. The company targets smaller population towns in Middle America and flyover country. If there is a public company with insight into the rural economy, it is Casey’s. Its results showed something similar to the rest of the economy: a normalization. A 4.4% same-store sales figure in prepared food and beverage is not a blowout figure. But it is not disturbing, either. Middle America remains in decent shape.

The U.S. economy is muddling through the middle of normalizing. It feels strange. And that is ok.

Originally Posted September 12th, 2024, WisdomTree blog

PHOTO CREDIT: https://www.shutterstock.com/g/JoPanuwatD

Via SHUTTERSTOCK

DISCLOSURES:

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.