By: Dane Smith, Head of North American Investment Strategy & Research

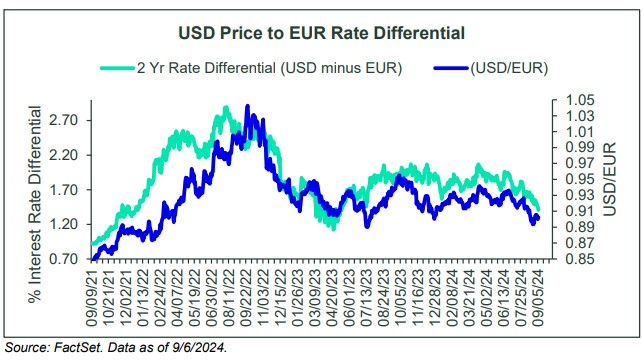

Across capital markets, there are a whole host of influences that have a push/pull effect on asset prices. When it comes to the US Dollar, a strong recent influence has been the interest rate differential between the US and other major economies.

Frequently, during times of economic uncertainty or global risk, the U.S. Dollar tends to be viewed as one of the “safe-haven” assets, providing downside protection. However, when focusing on more stable or recovery periods, interest rate differentials become a key determinant in how the currency moves. A higher interest rate in the US relative to Europe often incentivizes investors to move capital into USD denominated assets, boosting the US dollars value. This trend has been particularly evident over the past few years as the US has maintained higher rates than its Eurozone counterparts. Global economic troubles may have provided some tailwind for USD strength, but the persistent rate differential effects has been dominant over the past few years. The Fed is about to embark on a rate cutting path and is contemplating a 25 or 50 bps cut at the September 18th meeting. The ECB, however, got a head start and initiated its first 25bps cut back in June. Looking forward, we believe the paths decided by central bankers will continue to be a strong influence on the USD, something that historically hasn’t always been the case.

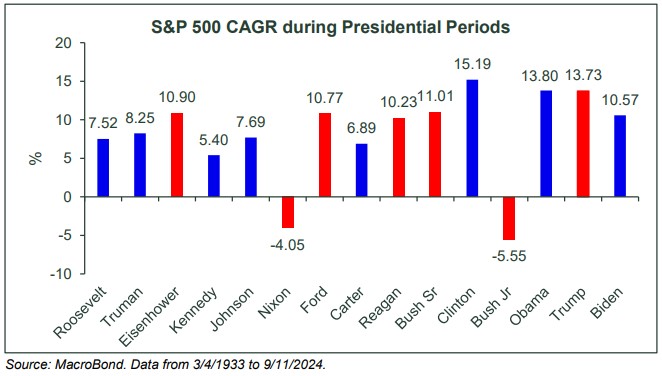

Harris vs. Trump.. Does the Outcome Matter? The presidential debate kicks off the next few months of election season with early voting starting in just a few days in Pennsylvania. Regardless of each candidates performance, we continue to anticipate the presidential race will remain narrow. As investors contemplate the impact of the toss up on the equity market we take a look at history to see how the equity market has performed over prior presidencies.

The chart above is a visual representation of the compound annual growth rate (CAGR) of the S&P 500 across presidential terms. Notably, the majority of presidencies have resulted in positive growth across years in office. However, democratic presidents have shown to produce a higher average CAGR of 9.4% over the studied years compared to 6.7% during republican presidencies. The drag on S&P 500 growth under republicans stems from the terms of Nixon and Bush Jr,. where they both presided over two recessions each. The question remains how much does the candidate matter for the equity market? The value creation inherent in innovating and growing economies such as the U.S. has allowed for equity market price appreciation across almost all presidencies. Although politicians aren’t solely responsible for how the stock market behaves, their policies and fiscal endeavors certainly have an impact. As the race progresses, our policy team has seen the odds of a democratic majority in the house improving. Ultimately this will have implications, positive or negative, for the legislative program and policies of the president-elect. The proposals of the two candidates are likely to impact specific sectors of the equity market and potentially, economic growth.

The newly elected President will have the most impact on the corporate tax rate, trade, regulation, energy, and healthcare. Investors looking to create tactical positions around the election may choose to position more heavily, or lightly, into sectors most impacted.

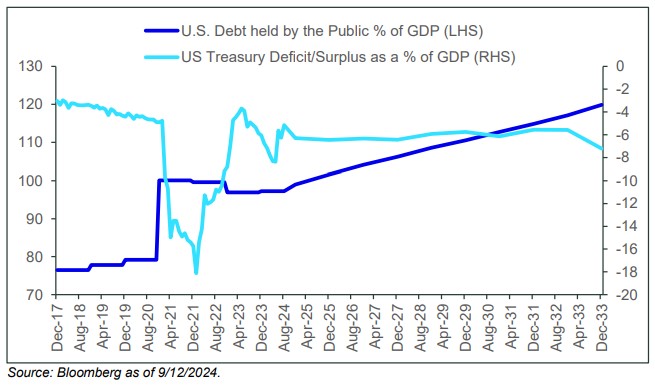

Will U.S. Treasuries Continue to Be a Safe Haven U.S. Treasuries are generally considered to be free of default risk. They are backed by the U.S. government and often serve as a safe haven especially during tumultuous economic environments. During the COVID 19 pandemic, the U.S. government initiated large scale debt fueled spending to stimulate the economy. The first two years (2020 and 2021) saw government spending increase by 50% driven by a combination of tax cuts and stimulus programs. Outstanding US government debt subsequently ballooned. With elections around the corner, and both candidates promising tax and spending plans, that would potentially further increase national debt, the haven status of treasuries could change. In the paper “Government Debt in Mature Economies, Safe or Risky” presented at the Jackson Hole Symposium, authors Roberti Gomez-Cram, Howard Kung, and Hanno Lustig discuss how governments underestimate their capacity to borrow debt. If governments choose to protect taxpayers, and issue large amounts of debt unfunded by taxes, they create an environment known as a risky debt or a fiscal dominance regime. In this environment, bondholders are forced to mark down treasury valuation when government cash flows backing their claims deteriorate, and therefore, demand a higher risk premium.

According to the Congressional Budget office, the U.S. national debt is expected to increase to $56 trillion by 2034 as rising spending and interest expense outpace tax revenues. As a share of the economy, debt held by the public is expected to be 122% of GDP. Annual interest costs are expected to rise to $1.7 trillion in 2034, approximately as much as current Medicare costs. *Under a potential Trump presidency, tax cuts could result in between $3.6 trillion to $6.6 trillion added to the U.S. deficit over the next decade. Potential outcomes under the still-developing Harris plan range from a deficit reduction of $400 billion to an increase of $1.4 trillion over the same period*.

Both candidates are expected to put popular policies ahead of fiscal responsibility, like contributing to further deficit expansion. While investors so far seem unconcerned with US government credit risk, a ballooning debt problem coupled with structural headwinds (low long-term growth and productivity) could make U.S. debt less attractive to investors in the long run (affecting both the ability and cost of borrowing). *Estimates provided by Committee for Responsible Federal Budget, University of Pennsylvania, Oxford, and Tax Foundation Source: State Street Global Advisors, Bloomberg.

Originally Posted September 16th, 2024, SSGA

PHOTO CREDIT: https://www.shutterstock.com/g/Saxarinka

Via SHUTTERSTOCK

DISCLOSURES:

Investing involves risk including the risk of loss of principal.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

The views expressed in this material are the views of the State Street Global Advisors Practice Management Group through the period ended August 15, 2024 and are subject to change based on market and other conditions. The opinions expressed may differ from those with different investment philosophies. The information provided does not constitute investment advice and it should not be relied on as such. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon.

This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

{kind=link}