By: Kevin Flanagan, Head of Fixed Income Strategy

Key Takeaways

- Rates in the U.S. credit market are expected to stay higher for longer, regardless of the actions of the Federal Reserve.

- U.S. corporate bonds have been considered expensive due to narrowing spreads, with investment-grade spreads declining by over 40 basis points and high-yield differentials falling by roughly 140 basis points.

- The current spread levels in the U.S. credit market are not unusual, as there have been previous periods when corporates have traded at similar or even lower levels.

While the money and bond markets continue their Fed-watch saga, there is one constant that we have been emphasizing for the fixed income landscape: a new rate regime. An integral aspect of this investment setting is that, despite what the Federal Reserve may or may not do, rates appear to be on course for staying higher for longer.

Against this backdrop, investors have been trying to determine where they should allocate funds in the fixed income universe, specifically within the U.S. Typically, one can break down the bond market into two distinct sectors: interest sensitive and credit sensitive. I’ve been spending a good amount of time in recent blogs posts and podcasts on the interest-sensitive side of the equation, so I thought it would be prudent to address trends for U.S. credit.

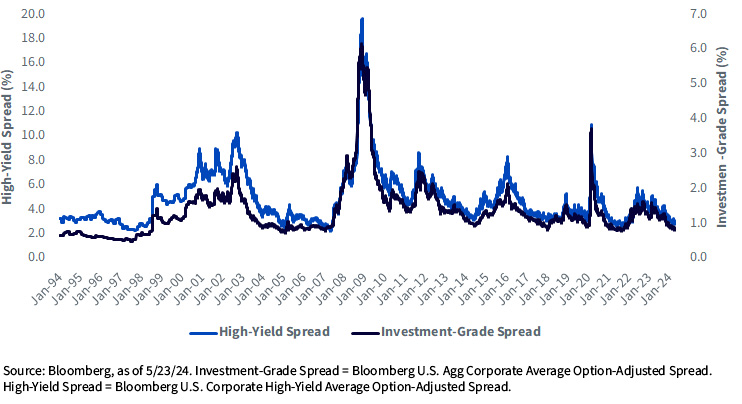

Investment-Grade Spread (RS) vs. High-Yield Spread (LS)

For definitions of terms in the chart above, please visit the glossary.

A key gauge in measuring relative value in U.S. corporate bonds is to look at spread relationships when compared to Treasury securities. These differentials can help determine where current corporate bond yields may reside in relation to historical levels. This analysis applies to both the investment-grade (IG) and high-yield (HY) universes. For reference, a narrow spread is often viewed as a sign that corporates could be leaning toward being expensive, while a wider differential would be viewed as the opposite, or comparatively cheap.

Throughout the better part of this year, there has been a sense among investors that U.S. corporate bonds appear to be more on the expensive side of the ledger due to the fact that both IG and HY spreads have been visibly narrowing since late October. To provide some perspective, IG spreads have declined over 40 basis points (bps) while HY differentials have fallen roughly 140 bps, as of this writing. Their current respective levels of 87 bps and 300 bps places them at the lower end of historical ranges.

This is where things get interesting. To listen to some of the current narrative on the subject, one could be forgiven for thinking the current readings are an unusual development. However, as the above graph illustrates, IG and HY spreads are definitely not in uncharted territory. In fact, there have been a variety of periods in the past when corporates have traded at these levels, and in some cases, even lower.

While I’d be the first to admit that, based on current spread levels, U.S. credit is not necessarily cheap, the resilient economy and somewhat favorable fundamentals seem to suggest they are not necessarily overly expensive either. In fact, using history as our guide, as long as the economy doesn’t fall off the cliff anytime in the months ahead, IG and HY spreads could continue to trade in their present respective ranges, but we would emphasize a quality-screened approach. In fact, if the fundamental backdrop can be maintained, one could potentially argue that a notable re-widening in spreads could be viewed as a buying opportunity, as we saw in pre-Covid trading.

This post first appeared on May 30th, 2024 on the WisdomTree blog

PHOTO CREDIT:https://www.shutterstock.com/g/pandorastudio

Via SHUTTERSTOCK

Disclosures:

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see the prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.