By: Michael W Arone, CFA, Chief Investment Strategist

This business requires all of us to read a lot. Like you, I appreciate the rigor of solid research, the suspense of a good plot unfolding, and the beauty of a perfect sentence. In this series called Reading the Markets, I’m excited to share my thoughts on some of the interesting ideas I discover.

It’s been a little more than a year since the Federal Reserve (Fed) responded to the regional bank challenges by launching the Bank Term Funding Program (BTFP), which unwound five months of quantitative tightening by injecting more than $303 billion dollars of liquidity into the market.

That kicked off a liquidity infusion that supported a 19% surge in the S&P 500® through July, from its 0.6% year-to-date gain when Silicon Valley Bank failed in March.1

Liquidity Headwind in April

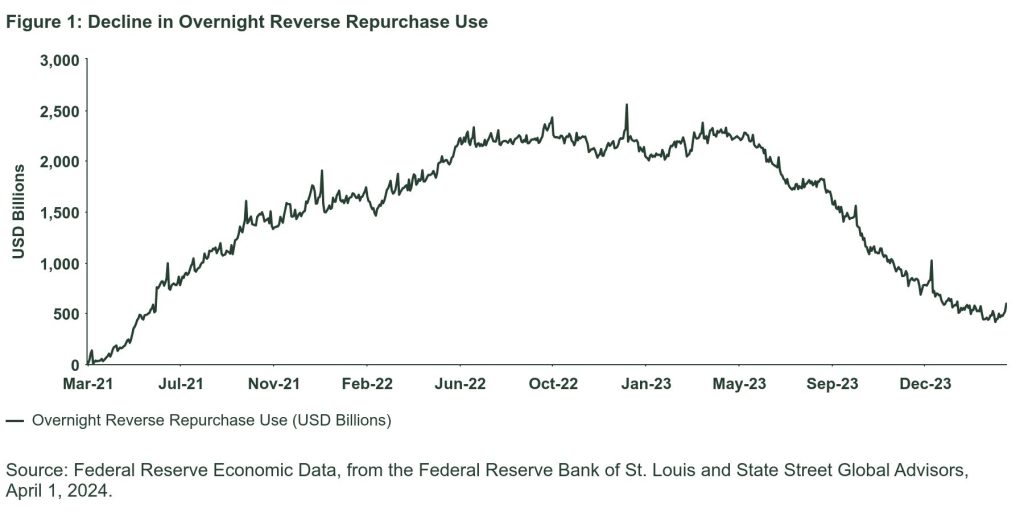

While investors tend to under appreciate the positive impact liquidity has on markets, they do notice when liquidity recedes. And, as Strategas Research Partners warns in “Liquidity & Fiscal Squeeze Has Arrived,” three critical components of liquidity — the Fed balance sheet, Treasury General Account, and reverse repos (RRP) — could turn negative in April and cause a temporary liquidity squeeze.

Figure 1: Decline in Overnight Reverse Repurchase Use

What’s driving the liquidity drain? According to Strategas:

- Taxpayers are expected to withdraw upwards of $250 billion from the financial system to pay their taxes.

- The Fed abruptly ending the BTFP in March means banks have already begun to repay their $160 billion in loans due over the next year.

- The Treasury is expected to retire $300 billion of T-bills in the second quarter, the first reduction in more than two years. And less T-bill issuance means higher RRP balances.2

Reacting to Volatility

We’re already seeing some volatility, but I don’t believe investors should worry. When liquidity contracted in August and November last year, the Fed and the Treasury came to the rescue. That will likely happen this time too, especially since it’s an election year.

The Fed continues to signal rate cuts and may slow its Quantitative Tightening later this year. And after tax-season, the Treasury will have more than $1 trillion available to spend heading into November’s election.

So, while the threat of a liquidity hiccup in April is real, I don’t believe there’s a need to reposition portfolios because it should be short-lived. But the brief window of volatility could feature attractive pricing that may prompt some investors to move hefty cash balances off the sidelines.

A temporary liquidity squeeze doesn’t change our positive outlook on equities. From the expanding economy and strong labor market to growing earnings and high profit margins, the backdrop remains very attractive for risk assets.

PHOTO CREDIT :https://www.shutterstock.com/g/pandorastudio

Via SHUTTERSTOCK

Originally Posted April 3rd 2024, on State Street Global Advisors’ blog

Footnotes

1 Bloomberg Finance, LP., as of March 26, 2024.

2 Policy Outlook, Strategas, March 25, 2024.

Disclosure

The views expressed in this material are the views of Michael Arone through April 2, 2024, and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETFs net asset value. Brokerage commissions and ETF expenses will reduce returns.

The S&P 500® Index is a product of S&P Dow Jones Indices LLC or its affiliates (“S&P DJI”) and has been licensed for use by State Street Global Advisors. S&P®, SPDR®, S&P 500®,US 500 and the 500 are trademarks of Standard & Poor’s Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”) and has been licensed for use by S&P Dow Jones Indices; and these trademarks have been licensed for use by S&P DJI and sublicensed for certain purposes by State Street Global Advisors. The fund is not sponsored, endorsed, sold or promoted by S&P DJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of these indices.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Investing involves risk including the risk of loss of principal.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

{kind=link}

{kind=link}