By: Jose Torres, Interactive Brokers’ Senior Economist

Markets are stumbling after Fed Chief Jerome Powell’s higher-for-longer reiterations on 60 Minutes last night. Significantly, Powell’s hawkish message was recorded prior to Friday’s blockbuster jobs number, which points to a Fed committee that’s increasingly tilting to the hawkish side. This morning’s stronger-than-expected ISM-Services print underscored Powell’s statements about the risks of a potential increase in inflation, with the data showing prices expanding faster than a cheetah, fueled in part by robust consumer demand.

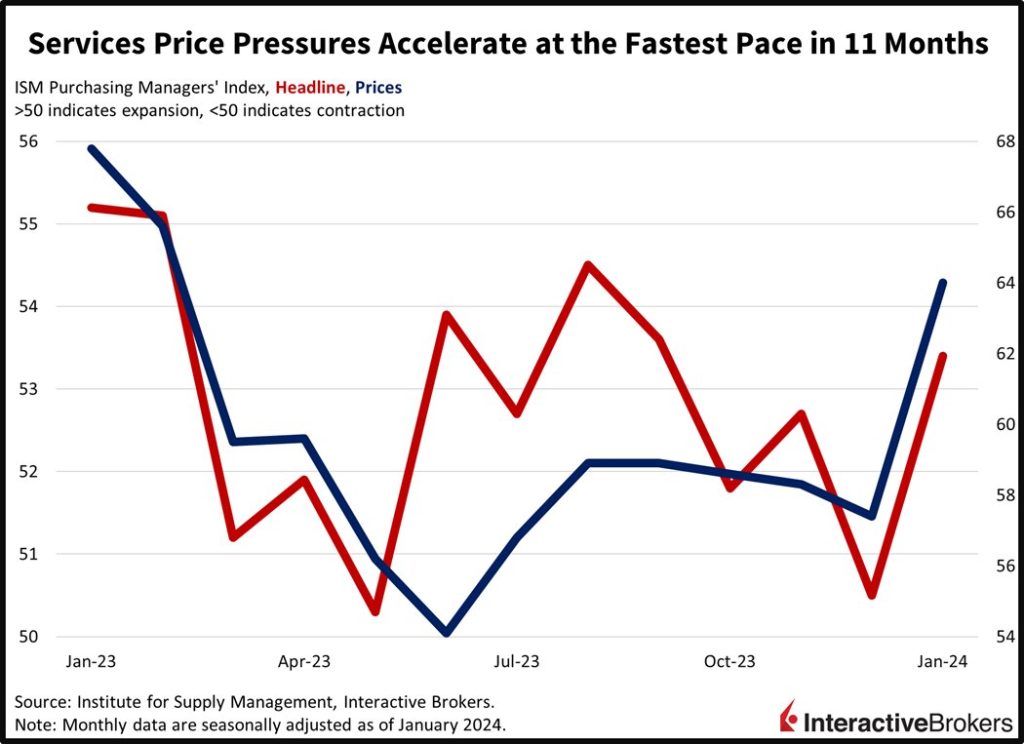

ISM Underscores Fears of Transitory Price Stability

The services sector expanded sharply to start off the year, achieving the quickest pace of growth since September. ISM’s January Purchasing Managers’ Index for Services rose to 53.4, much stronger than projections for 52 and December’s 50.5 figure. What’s worrisome is that prices were the main driver of the services sector’s expansion, with the report’s inflation segment reaching the highest level since February of last year. At a whopping 64, it was much higher than estimates of 56.5 and December’s 57.4. Customer orders drove much of the price gains, with the segment accelerating to 55 from 52.8. Business activity and employment also expanded, reaching levels of 55.8 and 50.5. The former was unchanged from December while the latter reversed from 43.8. Overall, services providers are anxiously awaiting interest rate reductions while they remain wary of persistent price pressures and geopolitical conflicts.

Corporate Guidance Underwhelms

The Middle East conflict is weighing upon McDonald’s Corporation’s results while significant cost cutting has helped Tyson Foods surpass earnings expectations. Meanwhile, the construction industry continues to limp along although energy and infrastructure are exceptions. Those are a few themes from the following fourth-quarter results:

- McDonald’s benefited from increasing its prices, but international franchise licensing growth was challenged by the Israel-Hamas war. The company’s earnings per share (EPS) of $2.95 after adjusting for one-time expenses climbed 13% from $2.59 in the year-ago quarter and beat the analyst expectation of $2.81. Revenue of $6.41 billion climbed 8% year-over-year (y/y) but missed the analyst estimate of $6.45 billion. On a positive note, the company’s global comparable sales, which comprise restaurants that have been operating at least 13 months, climbed 9% y/y. In the US, comparable sales climbed 4.3% with growth driven by price increases that boosted the average store transaction. McDonald’s reported strong international results for corporate-operated stores with locations in the UK, Germany and Canada posting the biggest gains, while sales in France declined. Within its licensed markets, which entail franchisee-operated stores, results were strong except for the Middle East. In a statement, McDonald’s said it anticipates challenging economic conditions throughout the year but said it is confident in the resilience of its business model.

- Tyson Food’s fourth-quarter earnings beat expectations despite declining y/y. Its earnings benefited from shutting certain US chicken plants, which helped to partially offset the impact of declining chicken prices. For the quarter, the company produced an EPS of $0.69 compared to the analyst consensus expectation of $0.42 but it declined from $0.85 in the year-ago quarter. Tyson’s revenue of $13.3 billion, however, missed the consensus estimate of $13.6 billion but increased slightly from $13.2 billion y/y. Tyson said average chicken prices dropped about 4% and sales volumes declined 1.5%. However, beef prices climbed, resulting in revenue increasing 6.3% despite a 4.1% decline in sales volume. An abundance of hogs caused pork prices to drop 8.5% but overall sales climbed 7.7%. Tyson said it expects sales this year to be flat compared to 2023.

- Caterpillar’s adjusted EPS of $5.23 jumped 35% y/y and surpassed the analyst consensus expectation of $4.75 despite revenue climbing only 3% to $17.1 billion. The revenue met the analyst expectation while Caterpillar’s operating margin climbed y/y, a result of the company increasing prices and a favorable comparison with its year-ago quarter having a goodwill impairment. At a time when the US is promoting clean energy and infrastructure improvements, Caterpillar’s energy and transportation sales climbed 12% y/y to $7.67 billion. For overall sales, North America was the sole region to grow with sales climbing 11% to $7.67% even with dealers decreasing inventories. The maker of heavy machinery and construction equipment estimates its current-quarter results will be similar to the same quarter of 2023 when the company produced $15.9 billion in sales. Analysts anticipated guidance of $16 billion.

Powell and ISM Data Drive Yields Up, Equities Down

Yields are soaring this morning as the one-two punch of Powell and ISM-Services data prevents market players from achieving further upside. All major equity indices are lower with the rate-sensitive, small-cap Russell 2000 leading the decline, dropping 2.1%. The Dow Jones Industrial, S&P 500 and Nasdaq Composite indices are down 1%, 0.6% and 0.4%, meanwhile. Sectoral breadth is in the tombs, with all sectors lower except for the defensive health care sector, which is up 0.5%. Materials, real estate and consumer discretionary are losing the most on the session, with the segments down 2.6%, 2.1% and 2.0%. The yield curve is shifting higher in a bear-steepening manner, as 2- and 10-year Treasury maturities trade at 4.46% and 4.15%, 8 and 13 basis points (bps) higher on the session. The US dollar is at its highest level since mid-November when gauged relative to a basket of currencies. It is benefiting from anticipations of less rate cuts and loftier long-term yields due to inflation expectations, with its index up 49 bps to 104.47. The greenback is gaining relative to the euro, pound sterling, franc, yen, yuan and Aussie and Canadian dollars. Energy markets are suffering despite continued Middle Eastern tensions, as oil traders focus increasingly on the stifling effects of the Fed’s restrictive monetary policy and persistent economic weakness out of Beijing. WTI crude oil is down 0.2%, or $0.15, to $72.16 per barrel amidst the cross currents.

Powell Reiterates on 60 Minutes

The Federal Reserve believes its monetary policy tightening has controlled inflation during the past six months, but the central bank needs more evidence that moderating price gains are durable before it feels confident enough to lower the fed funds rate. In sharing his view yesterday, Powell reiterated that he doesn’t think it will cut rates at its March meeting as policymakers will likely want more data to illustrate that recent gains in controlling inflation aren’t transitory. Powell signaled that mid-year would likely be a better time to introduce a cut. Complicating the inflation battle is the potential for goods and commodities to experience price gains as last year’s cooperation on both fronts will be difficult to reproduce. Furthermore, last Friday’s fiery jobs data alongside this morning’s hot services price results are likely to incrementally deter the committee from cutting, with 2024 potentially bringing a resurgence of price pressures. Finally, Powell also suggested that the Treasury is on an unsustainable fiscal path, which is emboldening him and his colleagues, with policy accommodation providing fiscal authorities with further leeway on the deficit front. Kicking the can down the road endangers our children and grandchildren’s generations.

This post first appeared on February 5th, 2024 on the IBKR Traders’ Insight blog

PHOTO CREDIT: https://www.shutterstock.com/g/chanawut13

Via SHUTTERSTOCK

Visit Traders’ Academy to Learn More About Economic Indicators

DISCLOSURE: INTERACTIVE BROKERS

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}

{kind=link}

{kind=link}