By: Jose Torres, Interactive Brokers’ Senior Economist

Construction workers are enjoying an employment feeding frenzy with onshoring projects and clean energy manufacturing facilities being built at a rapid pace, but individuals focused on residential construction may find their tool belts gathering dust with the U.S. Census Bureau this morning reporting weak activity among homebuilders. The report is pushing equity indices to new 17-month highs, however, as Treasury Yields decline because of easing fears that a strong construction industry recovery in May could have stimulated economic growth excessively and ignite renewed inflationary pressures. Today’s optimism comes with the market believing that next week’s 25 basis-point (bps) fed funds hike will be the last of the current cycle, despite policy makers frequently claiming that the central bank is likely to do two more.

From Strong to Weak

Across the country, businesses are increasingly building new manufacturing facilities as they onshore production of their goods while foreign companies are claiming a U.S. beachhead to be closer to customers. Unlike the current real estate market, which is heavily influenced by mortgage rates, manufacturing construction is booming within a secular trend. The Taiwan Semiconductor Manufacturing Company’s (TSMC) headquarters and fabrication plant under construction in north Phoenix, which is just one of many facilities being built, for example, is expected to create some 80,000 jobs over the next few years.

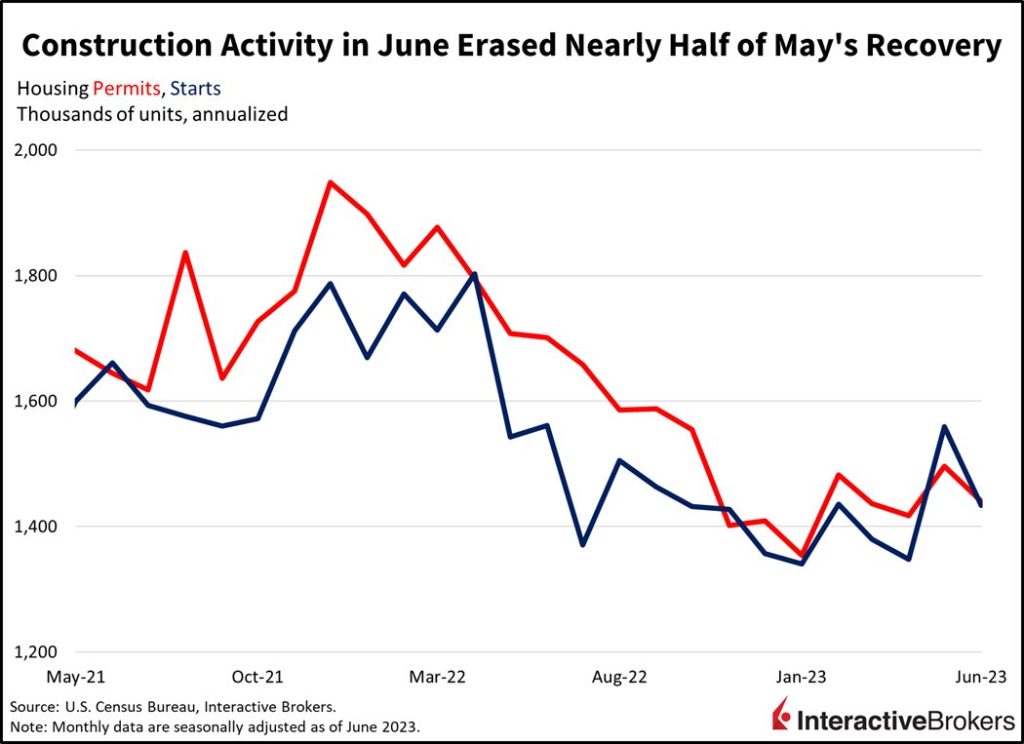

Residential construction, however, is sagging, with mortgage interest rates of nearly 7% creating a huge headwind for home buyers. Last month, permits for new home construction fell to 1.44 million seasonally adjusted annualized units (SAAU), 3.7% less than the previous period’s rate of 1.496 million. Today’s June data also missed the consensus expectation calling for 1.49 million.

Housing starts, which are recorded once shovels hit the ground, also missed projections by a mile. June had 1.434 million starts, substantially trailing the 1.48 million consensus estimate. June also marked a significant 8% decline from May’s lofty 1.559 million level, erasing about half of the month’s recovery from April and questioning new home demand with prices and mortgage rates causing houses to become less affordable.

Single-Family Construction Is a Bright Spot

While overall construction activity slowed significantly, single-family performed much better than multi-family, with permits for single-family up 2.2% during the month while multi-family declined 13.5%. The trend within starts is similar as single-family declined 7.0% while multi-family declined a sharper 11.6%. From a regional perspective, the Northeast, West and South weighed on permits, with month-over-month (m/m) declines of 23.4%, 4.0% and 2.6%. The Midwest helped alleviate some weakness, however, with permits up 5.9% m/m. All regions reported a m/m contraction in starts.

Higher Interest Rates and Weary Consumers Challenge Earnings

Residential construction isn’t the only area of the economy feeling the sting of higher interest rates and consumers struggling with inflation. Goldman Sachs this morning reported a $500 million impairment with its expected sale of its fintech consumer financing platform, GreenSky. It also reported a $485 million loss in commercial real estate, declines in investment banking revenues and sluggish activity with asset management and trading. Goldman posted second-quarter earnings per share (EPS) of $3.08, missing the consensus expectation of $3.18. Ally Financial, which focuses on auto financing, saw the rapid climb in short-term interest rates increase its financing costs while its auto loan net charge-offs climbed from $108 million in the year-ago quarter to $277 million in the quarter ended June 30. Its GAAP net income dropped from $454 million to $301 million year-over-year (y/y) but its EPS of $0.99 exceeded the $0.94 EPS expected by consensus. Logistics company JB Hunt also reported disappointing results with its trucking volume declining, due largely to consumers curtailing their goods spending as inflation increases living expenses while higher rates make durable products much more expensive. The company’s revenues have dropped 18% y/y and its EPS of $1.81 missed the consensus expectation of $1.92.

Markets Breathe Sigh of Relief

Markets are alleviated by softer construction data which is paving the way for further upside in stocks, with the S&P 500 Index reaching its highest level since March of last year. In fact, the S&P 500 Index is only approximately 5% away from its all-time high of 4818 reached in January of 2022. All major U.S. indices are higher, with cyclicals leading amidst mixed participation. While most sectors are higher, technology, materials, homebuilders and industrial are lower. Unexpectedly, however, the defensive utilities sector is reaping the most gains this morning, gaining 1.3%. Bonds yields are slightly lower across the curve, with the 2-and 10-year maturities down 1 bp each to 4.74% and 3.78%. Lower inflation readings out of Great Britain and Canada are pulling down those countries’ currencies and causing a double-digit bp drop in British Gilts. The combination is pushing the Dollar Index higher by 54 bps to 100.46, above the important 100 support level. Lower oil inventories in the U.S. against a risk-on backdrop are driving WTI crude oil up 1% to $76.30 per barrel.

Easy Comps Cut Challenging Future

Rallying this hard into earnings season raises investors’ expectations of companies, making additional gains from here harder to come by. After all, the market is 5% from all-time highs, a time that coincided with zero interest rates, $120 billion in monthly liquidity injections and peak earnings.

The latest episode of loosening financial conditions has been driven largely by lower y/y inflation readings around the globe. Investors may be way over their skis; however, because $130 oil caused by the Russia-Ukraine conflict caused inflation to surge last summer, leading to easy comps this summer. With important earnings looming and Fed Chairman Jerome Powell taking the mound next week in Washington and next month at Jackson Hole, investor expectations may be riding too high. Rallying this hard into earnings season raises investors’ expectations of companies, making additional gains from here harder to come by. After all, the market is 5% from all-time highs, a time that coincided with zero interest rates, $120 billion in monthly liquidity injections and peak earnings. Are equities immune to rate hikes, liquidity contractions and earnings declines over the medium-term?

Visit Traders’ Academy to Learn about Building Permits and Other Economic Indicators

This post first appeared on July 19th 2023, Traders’ Insight Blog

PHOTO CREDIT: https://www.shutterstock.com/g/yuttana+jeenamool

Via SHUTTERSTOCK

DISCLOSURE: INTERACTIVE BROKERS

Information posted on IBKR Campus that is provided by third-parties and not by Interactive Brokers does NOT constitute a recommendation by Interactive Brokers that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with permission from IBKR Macroeconomics. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and IBKR is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation to buy, sell or hold such security. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

In accordance with EU regulation: The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

Any trading symbols displayed are for illustrative purposes only and are not intended to portray recommendations.