By: Elliot Hentov, Ph.D., Head of Macro Policy Research and William A Goldthwait, Portfolio Strategist and Simona M Mocuta, Chief Economist, SSGA

Markets have grown accustomed to the debt ceiling drama, but 2023 has the potential to be an even more dramatic year. Given this possibility, we review the key debt ceiling scenarios, their impact on the macro-outlook and investment implications thereof.

In our view, there are three distinct scenarios through which the debt ceiling episode could play out for the financial markets: 1) a non-event, 2) a temporary stress period with lasting fiscal impact and 3) a severe risk-off event with knock-on consequences.

Scenario 1: A Non-Event

Likelihood: Low

Investment Implication: Neutral

For the debt ceiling to be a non-event, it requires a timely political compromise between the Democrats and the Republicans before the appearance of any undue market stress. Given the competing interests of both sides, we find this to be highly unlikely. Republicans view the debt ceiling as a bargaining leverage ahead of the 2024 US presidential election, while Democrats consider any concession as an abuse of constitutional arrangements. Also, Democrats now view Barack Obama’s negotiations in 2011 and 2013 as a political mistake not to be repeated.

The most plausible avoidance of a crisis would be a short-term delay in aligning the debt ceiling deadline with the end of the budgetary cycle in late September. This would hold electoral appeal for Republicans to fold the debt ceiling into a broader fiscal policy debate. Democrats would certainly prefer to avoid this outcome but may accept it as a lesser evil, perhaps with the hope that the timing of US Treasury’s extraordinary measures could permit a few weeks of government shutdown prior to the so-called “x-date” (when the debt ceiling will limit new debt issuance and Treasury can no longer meet all its obligations). In this scenario, markets would simply be facing the same outlook a few months later.

Scenario 2: Temporary Financial Stress and Lasting Fiscal Contraction

Likelihood: High

Investment Implication: Buy Medium to Longer Duration Treasuries

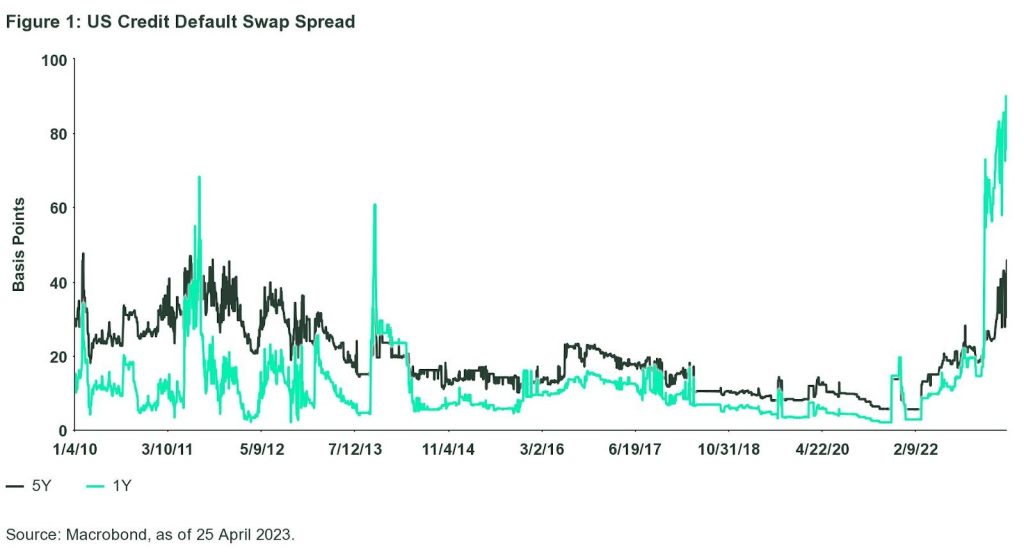

The reality is that an exogenous force is required to break the current political impasse. This could be a foreign policy emergency but is more likely to be financial market stress. During the first major standoff in 2011, markets started to price in default risks only a few trading days ahead of the deadline. Since then, markets are reflecting this risk earlier and more significantly (Figure 1).

Figure 1: US Credit Default Swap Spread

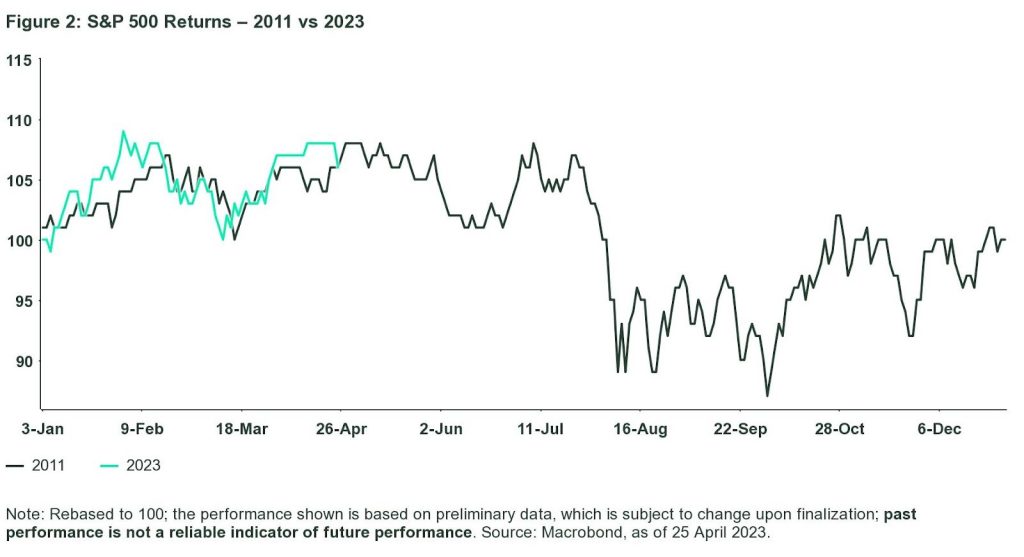

However, for market stress to become a substantial “political force,” it must worsen. This means, for the needle to move, it would not only require big moves in short-term US Treasury yields but also a sizable drawdown in the equity market. In 2011, the S&P 500 lost only about 5% in advance of the political deal but dropped another 10% in the days that followed (Figure 2). In 2023, these types of market moves would have to precede any last-minute political compromises, including a bipartisan deal.1

Figure 2: S&P 500 Returns – 2011 vs 2023

The Consequences of a Bipartisan Deal

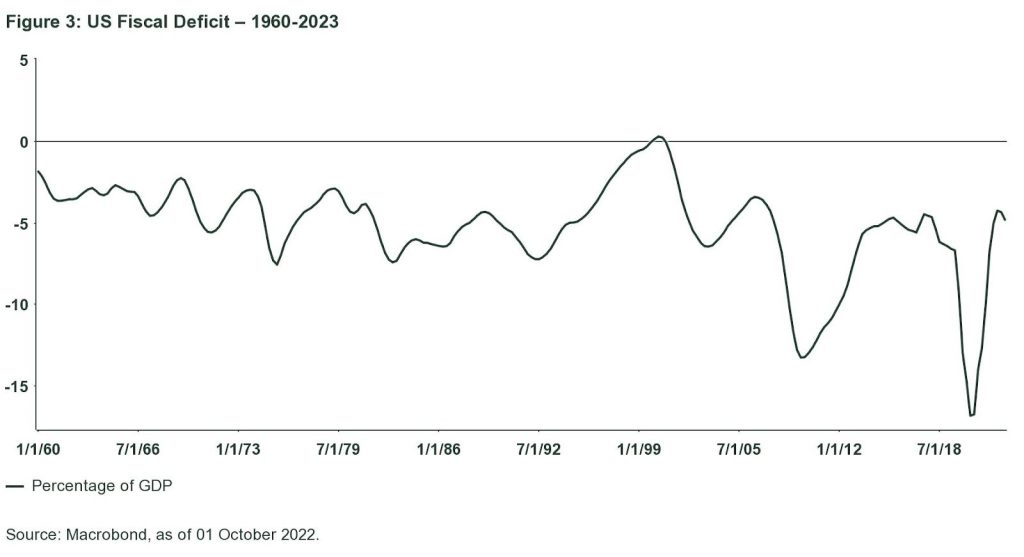

What would not be temporary, and have arguably helped the equity drawdown in 2011, is the fiscal contours of any bipartisan deal. What is included in that deal matters enormously. Directionally, we know that significant spending reductions would be embedded in medium-term fiscal plans. In other words, after several years of massive positive fiscal impulses, the economy will suddenly have to contend with a material fiscal drag.

The Republican bill has penciled in US$4.3 trillion in spending cuts over ten years. Any compromise would be no more than half that figure, but that would still be the equivalent of 1% of nominal GDP getting shaved off per year in 2024-2026. In real terms, the hit would be somewhat less but still substantial and the tightest fiscal stance since pre-2008 (Figure 3). This is why aspects of the bill that attempt to resolve the debt ceiling crisis (i.e., the agreed-upon budgetary savings) hold such importance.

Figure 3: US Fiscal Deficit – 1960-2023

The deal’s more austere fiscal positioning is likely to occur alongside a less-accommodative monetary stance. After all, even as we expect the US Fed to be in a position to cut rates before end-2023, there still remains a need to reduce the Fed’s balance sheet. In this scenario, both fiscal and monetary policies are likely to be set up for draining liquidity from the system – the reason we think the Fed’s quantitative tightening (QT) will have to end after the debt ceiling. The last rate hike will have been in May 2023, so the Fed is likely to object to financial conditions tightening. And with the likely explosive burst of new Treasury issuance following a debt ceiling deal, QT will no longer be sustainable.

At the same time, not only growth, but inflation, too, is bound to be lower in that environment, although inflation volatility could remain elevated as the world will be more vulnerable to supply shocks.

Scenario 3: Severe Risk-Off

Likelihood: Medium

Investment Implication: All-Round Defensive Positioning

The alternative to any resolution of the debt ceiling would be a non-resolution, leading to more extreme market reactions as chances of a default in US debt would continue to rise. This does not imply a debt default but simply that the deadline would pass. In this scenario, we would expect the Biden administration to draw on controversial legal justifications to continue to make debt payments (despite current denials of the technical and political feasibility), thereby delaying non-debt obligations as much as possible to avert any technical default (see Addendum).

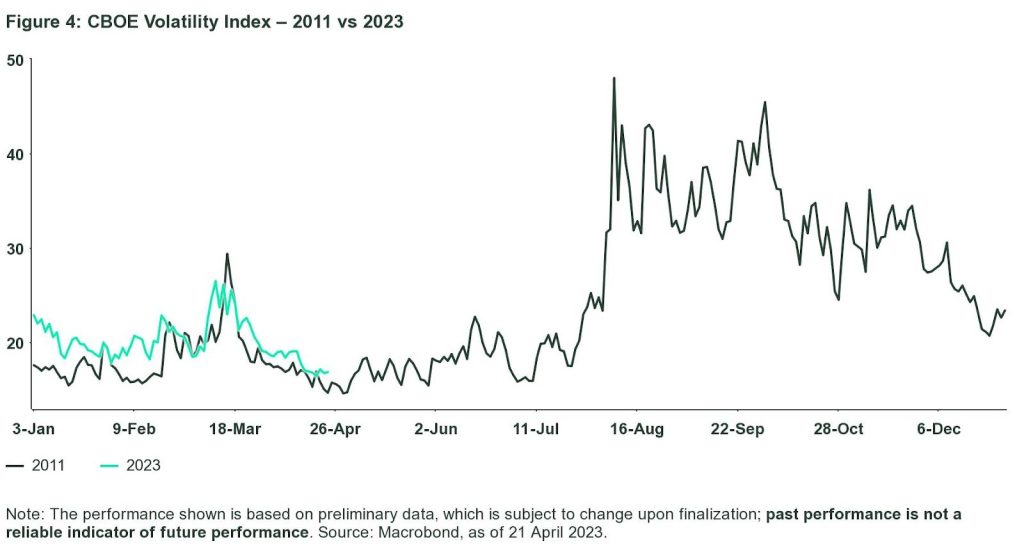

Given the unprecedented nature of such actions and the fiscal impact of suddenly freezing large channels of regular government expenditure, market reactions could continue to exude extraordinary volatility with very rapid moves in short-term rates and sharp drawdowns in equities, commodities and other risk assets (Figure 4). Against this background, rating agencies are likely to issue a credit watch or a downgrade even absent an actual missed bond payment, which could set off a chain of negative reactions.

Figure 4: CBOE Volatility Index – 2011 vs 2023

In the aftermath of the SVB crisis, we were reminded how quickly risks can snowball out of control. Soon after the bruising experience of a widespread deposit flight, the last thing any US banking institution needs is a sudden decline in loan collateral values and a surge in non-settlements. Similarly, the last thing that the US itself needs is another debt downgrade that could impact the ability of certain buyers to own US debt.

While this would be unprecedented, the Fed could help sustain this situation by offering to swap some of their System Open Market Account Holdings (SOMA) holdings for any particular Treasury issue maturing at the time. Currently, the Fed owns US$367 billion of Treasury bills (T-Bills), and while balance sheet expansion and politicization are clearly counter to their current policy stance, these could come under consideration during a scenario of extreme financial stress.

Lastly, once precedent is broken, it is not clear how a sustainable balance is restored. Any political truce could re-erupt with the budget discussion in late September and any unilateral action of the Biden administration could trigger a judicial review process. Either way, some residual higher uncertainty would be sustained, which will anchor tighter financial conditions and prolong a risk-off environment.

Conclusion

The debt ceiling dispute in 2023 is unlikely to be a passing phenomenon. At a minimum, it will produce lasting fiscal headwinds to the US economy and in a worse-case scenario, it could constitute a durable financial stress event. In both cases, long-term yields are likely to come down and risk assets will underperform. As a result, to a certain degree, it may result in the more pessimistic economic forecasts actualizing.

This post first appeared on May 4th 2023, State Street Global Advisors’ Blog

PHOTO CREDIT: https://www.shutterstock.com/g/AndyDeanPhotography

Via SHUTTERSTOCK

Footnotes:

1 An alternative scenario would be where other forms of bipartisanship prevail under market pressure, such as a discharge petition initiated by Democrats that only requires the support of five Republican rank-and-file congresspeople. All in all, this scenario would witness a meaningful, albeit temporary, tightening in financial conditions, as any bipartisan resolution would shift the next debt ceiling limit to 2025 or later. However, the odds of this are extremely low as the discharge petition would require 37 legislative days of preparation and Republican unity in the House disqualifies that pathway.

Disclosure

Marketing Communication

State Street Global Advisors Worldwide Entities

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without State Street Global Advisors’ express written consent.

The views expressed in this material are the views of Elliot Hentov, William Goldthwait and Simona Mocuta through the period ended 03 May 2023 and are subject to change based on market and other conditions.

This document contains certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

All information is from State Street Global Advisors unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Past performance is not a reliable indicator of future performance.

Investing involves risk including the risk of loss of principal.

Generally, among asset classes, stocks are more volatile than bonds or short-term instruments. Government bonds and corporate bonds generally have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. U.S. Treasury Bills maintain a stable value if held to maturity, but returns are generally only slightly above the inflation rate.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates rise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

For EMEA Distribution: The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

© 2023 State Street Corporation – All rights reserved.

{kind=link}