Last week, I blogged on the theme of the recent shifting narrative in the money and bond markets. One of the key catalysts behind this changing dynamic came from two inflation readings (CPI & PPI), which revealed that the ‘cooling’ effect that had been on display in Q4, had been dialed back a bit to begin 2023. Well, now we can add the Fed’s preferred inflation gauge to the conversation as well.

For the record, this preferred measure is known as the Personal Consumption Expenditure Price Index (PCEPI). For January, the year-over-year rates for both the overall and core measures actually increased by 0.4pp each, to 5.4% and 4.7%, respectively. Needless to say, this news only provided more fuel to the aforementioned narrative shift, pushing Treasury yields higher, accordingly.

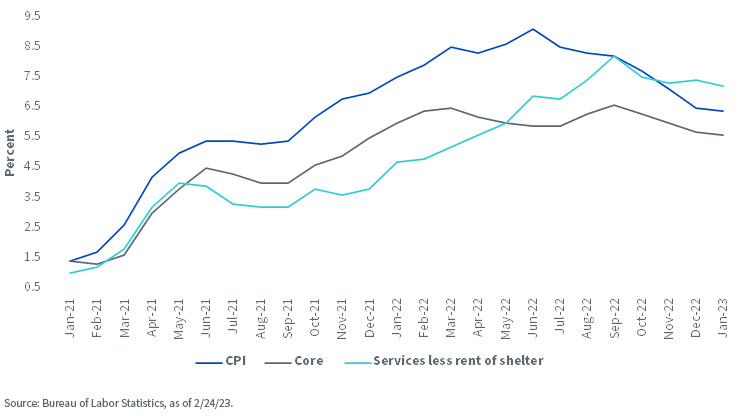

CPI Gauges – 12-month % Change

This takes us to where we may be headed. While progress was being made on the core inflation front, it appeared to have a more ‘sticky’ component to it. One of the key points centered around how the Bureau of Labor Statistics (BLS) measures housing, or shelter costs. Indeed, a compelling argument was being made that the BLS data overestimated housing inflation. As a result, the ‘services less rent of shelter’ component within the CPI release began to garner more attention. Looking at inflation from a three-month interval perspective, there was a definitive downward trajectory to this category prior to the January 2023 report, which reinforced the ‘overestimating’ case. To be sure, the three-month change plunged from 3.4% in June to only a scant 0.2% in December. Interestingly, this component reversed course completely to open 2023 by rising 1%.

Conclusion

Where does that leave us? While inflation does appear to have peaked last summer, unfortunately for the Fed, and by extension the bond market, the future road may not be as much of a one-way street to the downside as we saw during the autumn months. Nevertheless, a continued broader cooling in price pressures still remains a reasonable case scenario. However, against this backdrop, the Fed will continue to operate under the assumption it ‘has more work to do’.

Originally Posted March 1st, 2023 WisdomTree

PHOTO CREDIT:https://www.shutterstock.com/g/pictureguy

Via SHUTTERSTOCK

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see the prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.