By: Kevin Flanagan, Head of Fixed Income Strategy

With the money and bond markets preoccupied with inflation, the chance of a recession and, of course, Fed rate hikes, the state of the U.S. government’s finances has not received much attention, if any. The situation has rather reminded me of the classic line in the Wizard of Oz: “Pay no attention to that man behind the curtain.”

With that in mind, I thought it would be interesting to provide some insights on this front. Before getting started, here is a quick ‘U.S. budget 101’ as a refresher. The federal government’s fiscal year (FY) does not line up with the calendar year. It runs from October through September, so we have now received the results for FY 2022.

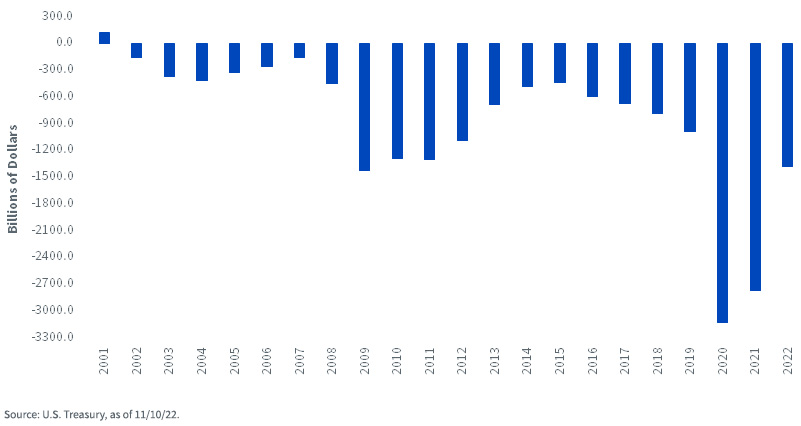

U.S. Budget Deficit/Surplus

According to the Treasury Department, the U.S. ran a deficit of $1.38 trillion in FY 2022. Interestingly, some of the headlines relating to this announcement seemed almost euphoric, pronouncing that the prior year’s deficit was cut in half, and that it was the biggest decline in history.

This is where things need to be put into some proper perspective. While the headlines were technically accurate, the total of FY 2022 red ink was an improvement on the second-largest deficit ever recorded: $2.77 trillion for FY 2021 (the largest shortfall, at $3.13 trillion, occurred in FY 2020), but it was only slightly below the previous peak of $1.42 trillion in FY 2009.

Obviously, the improvement from the 2020 historical peak, as well as last year, has had a lot to do with reduced government spending following the earlier adverse effects of the Covid lockdown. In addition, revenues increased as the economy rebounded into positive territory. For FY 2022, total outlays declined by 8.1%, while overall receipts surged by 21%.

That’s the past. What about the future? For all intents and purposes, it looks as if the baseline still resides somewhere around a deficit of a trillion dollars, at least in the near term. The future is another story.

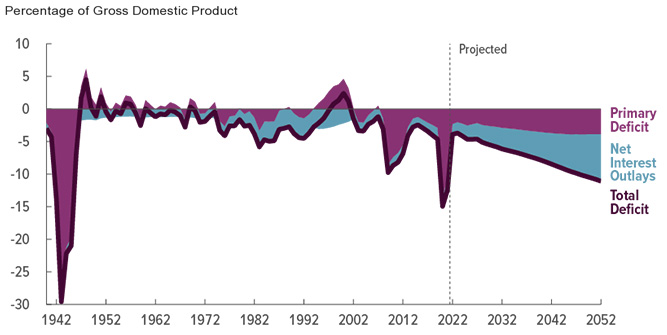

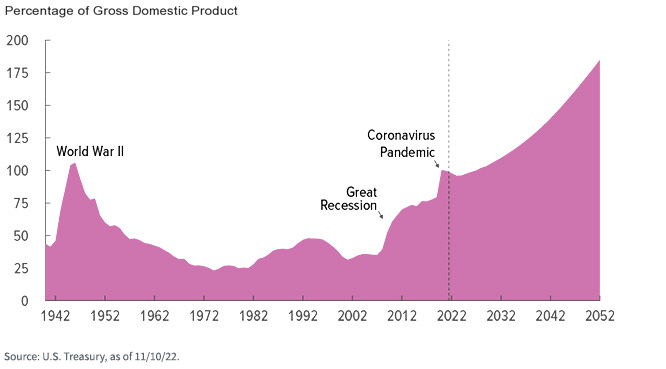

The Congressional Budget Office (CBO), which operated under the assumption that “current laws governing taxes and spending generally do not change,” reported that “federal deficits are projected to nearly triple over the next 30 years, from 4% of GDP in 2022 to 11% in 2052.” The primary driver of this increase is expected to come from net interest expense. Based on the CBO’s projections, net interest outlays will expand from the current pace of 1.6% of GDP to 7.2%. As a result, this could cause the federal debt held by the public to rise to 185% of GDP in the next 30 years (see below).

Total Deficits, Primary Deficits, and Net Interest Outlays

Federal Debt Held by the Public, 1940 to 2052

Conclusion

While deficits do matter in the long run, interest rate trends tend to take their primary cues from Fed policy as well as the economy and inflation in the shorter run. In that regard, the lack of attention the fixed income arena is currently paying to the U.S. government’s finances may seem reasonable on the surface. However, let’s hope those storm clouds that Dorothy and Professor Marvel (later the Wizard) saw coming dissipate in the years ahead

This post first appeared on November 16th, 2022 on the WisdomTree blog

PHOTO CREDIT: https://www.shutterstock.com/g/vchal

Via SHUTTERSTOCK

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see the prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

{kind=link}

{kind=link}