By: Olivia Engel, CFA, CIO, Active Quantitative Equity and Timothy J Herlihy, CFA, Portfolio Specialist

The language and tone a management team uses can signal how it feels about quarterly results or how it expects the market to react to them. Subconscious communications in earnings calls can carry important insights for investors.

Each quarter, the Active Quantitative Equity (AQE) team closely examines conference call language and tone for subconscious communications from company management to investors. We use natural language processing to evaluate individual company conference call transcripts and assign each company a score for Conference Call Sentiment (CCS). Specifically, this CCS “factor” seeks to reflect the tone, the level of optimism or pessimism, and the type of verbiage in the call, providing an indication of the attractiveness or unattractiveness of a particular stock.

Given the current uncertainty of the macroeconomic landscape and the increased focus on second quarter earnings, the CCS factor can contribute valuable insights to our research process. Management teams have a closer proximity to and understanding of the drivers of return for their companies and industry, and the language they use during conference calls can give subtle, unscripted signals of their expectations.

Our focus in this piece is on the interpretation of our CCS factor. However, it is important to note that no one signal in our process is used on a standalone basis to assess the returns potential of a stock, sector, or industry; rather, CCS is incorporated with several diversified factors in the AQE team’s multi-factor stock selection model to arrive at an investment decision.

Reading Sector Results for Insights

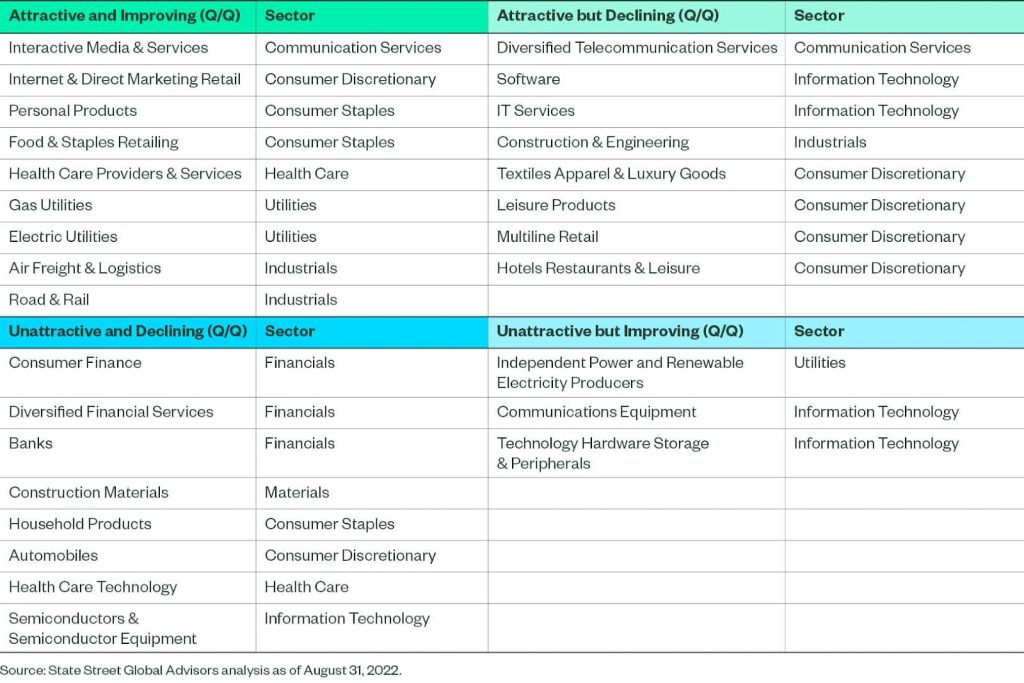

The findings from the AQE team’s CCS factor can offer valuable insights in the research process. The latest results from our CCS factor results are shown in Figure 1, followed by some insights.

Figure 1: Conference Call Sentiment Factor Results

The AQE team sees a relationship between improving Conference Call Sentiment and cyclical versus defensive characteristics broadly. The global economy has been stuttering this year, and company management and investors are worried about the impact of inflation and slowing growth on company earnings. It is understandable, therefore, that the majority of the industries with “attractive and improving” quarter-over-quarter CCS scores are non-cyclical or defensive in nature, as they are better able to withstand the current environment. The opposite is true within the “attractive but declining” bucket, where the majority of industries are cyclical and the outlook may be starting to wane.

Among industries with unattractive CCS scores, we again find a relationship with cyclicality; the majority of industries where management is showing less confidence reside in the cyclical space, notably Financials and IT Hardware.

However, some industries do not show a relationship between CCS and cyclicality. The Internet and Direct Marketing Retail, Air Freight and Logistics, and Road and Rail sectors are cyclical but have a CCS factor that is positive and still improving.

On the flip side, management in Healthcare Technology and Household Product companies, although within naturally defensive sectors, seem less confident about the outlook and demonstrate a declining CCS.

The Bottom Line

As concerns about inflation transitioning to stagflation mount in today’s market, the AQE team is seeing significant trends in the preference for, and expectations of, cyclical versus non-cyclical sectors. By digging deeper and assessing sectors using our CCS lens, the AQE team believes that there are strong corporate distinctions across the industries within these sectors.

We believe opportunities remain for some cyclicals, while some defensive industries appear less sanguine. Adopting a nuanced view that takes conference call sentiment into account enables us to glean additional insights and to construct portfolios that better navigate today’s current turbulent environment.

Originally Posted September 20, 2022, SSGA

PHOTO CREDIT:https://www.shutterstock.com/g/nengnatee

Via SHUTTERSTOCK

Disclosure

ssga.com

Marketing Communication

State Street Global Advisors Worldwide Entities

For use in EMEA: The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

This communication is directed at professional clients (this includes eligible counterparties as defined by the appropriate EU regulator) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons, and persons of any other description (including retail clients) should not rely on this communication.

Important Risk Information

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor.

All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Investing involves risk including the risk of loss of principal.

The views expressed are the views of Active Quantitative Equity through September 14, 2022, and are subject to change based on market and other conditions.

Quantitative investing assumes that future performance of a security relative to other securities may be predicted based on historical economic and financial factors, however, any errors in a model used might not be detected until the fund has sustained a loss or reduced performance related to such errors.

Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions.

© 2022 State Street Corporation.

{kind=link}