By; Steve Sosnick, Chief Strategist at Interactive Brokers

Timing can sometimes be fortuitous. My first trip to Europe was in March 1985. I had a friend studying in the UK and decided to pay him a visit. The combination of having a floor to crash on and an airfare war between Peoples Express and Virgin meant that the trip would be cheaper than heading to Florida for spring break. But the real key to the affordability was the strength of the US Dollar (USD). It turns out that the all-time low for the British Pound (GBP) vs. USD occurred just before my trip. The exchange rate was between 1.05 and 1.10 during that visit – something that seemed unimaginable for decades to follow. Using my friend’s dorm as a base for another visit, I returned during the summer. The Euro (EUR) didn’t exist then, but if it had, it would have been about 0.75 – a level never seen as a common currency. By then, GBP had bounced back over 1.20, a level that was a huge bargain for decades. Until now, that is.

The point was not to bore you with a bygone travelogue, but to illustrate the significance of the recent upward move in USD. The following chart shows how USD has spiked since the start of this year.

U.S. Dollar Index (USDX), Continuous Futures (DX), 3-Years, Daily Bars

Source: Interactive Brokers

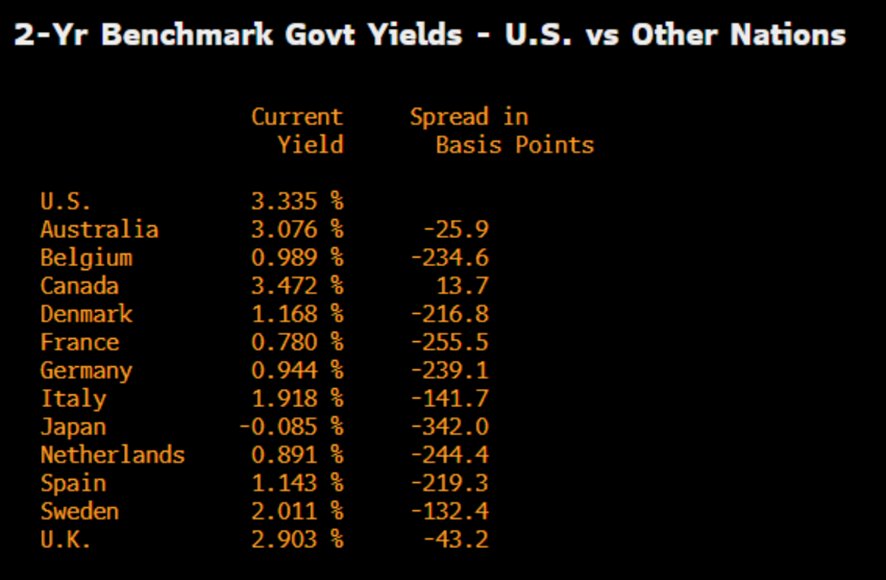

Parabolic moves of this sort mean that some sort of dislocation is occurring. While this is far from the steepest parabola that we have seen, bear in mind that foreign currency is the most liquid and most actively traded market of all. It takes quite a bit to get major moves of this type. Yet it should be obvious that major macroeconomic forces are at work. The Federal Reserve and other global central banks are raising rates, though not at the same pace. I noticed the following table this morning, which brought that notion into sharp relief:

Source: Dow Jones via Tullet Prebon via FactSet

It is apparent that the Fed is much further along its rate hiking path than most of its peers. All things being equal (and they rarely are), a currency with higher risk-free rates should trade at a premium to a lower yielding alternative. When the country behind that economy is showing greater growth prospects than its peers – remember, this on a relative, not absolute basis – that helps too. Under that scenario, it is understandable why USD would outperform GBP and certainly EUR.

The ramifications for a stronger dollar are manifold. Strong inflows into US fixed income can suppress Treasury and other yields, complicating the interest rate messages sent by the bond market. Those inflows could also find their way into equities, which benefit from foreign buying. At the same time, however, a stronger dollar can be a headwind for multinational corporations.

US domiciled companies that sell goods and services in a wide range of countries find that their non-US revenues and profits suffer when converted back to USD. A Euro earned in say, Spain, is worth less on a USD income statement than it was just a few months ago. CFOs work very hard to hedge the impact of foreign currency translations, but some companies are more successful in those efforts than others. In general, it is difficult to expect that all multi-nationals can completely immunize themselves from foreign currency effects. And we all know that US equity indices are dominated by multinational corporations. Thus, if the dollar continues onto further strength, we can expect to see a negative impact on major US companies. That can have a profound effect on equity valuations, and not in a good way. Of course, if the dollar reverses its recent uptrend, the opposite will be true.

That said, my wife wants us to visit Europe and the UK this fall. I never expected to be planning a trip with the pound at levels not seen since one of my first forays.

This post first appeared on August 24th 2022, Interactive Brokers Traders’ Insight Blog

PHOTO CREDIT: https://www.shutterstock.com/g/ImagePixel

DISCLOSURE: INTERACTIVE BROKERS

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers LLC, its affiliates, or its employees.

Any trading symbols displayed are for illustrative purposes only and are not intended to portray recommendations.

In accordance with EU regulation: The statements in this document shall not be considered as an objective or independent explanation of the matters. Please note that this document (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and (b) is not subject to any prohibition on dealing ahead of the dissemination or publication of investment research.

{kind=link}