Each month, the State Street Global Advisors’ Investment Solutions Group (ISG) meets to debate and ultimately determine a Tactical Asset Allocation (TAA) that can be used to help guide near-term investment decisions for client portfolios. By focusing on asset allocation, the ISG team seeks to exploit macro inefficiencies in the market, providing State Street clients with a tool that not only generates alpha, but also generates alpha that is distinct (i.e., uncorrelated) from stock picking and other traditional types of active management. Here we report on the team’s most recent TAA discussion.

Macro Backdrop

The global economic environment has become considerably more precarious following the Russia-Ukraine War. The resultant stagflationary shock has worsened monetary policy trade-off for nearly every central bank. Central banks badly misread the inflationary environment and must accelerate rate hikes, which poses a material risk to growth.

Inflation has remained elevated and the longer it lasts, the stickier it gets. Inflation appears to have impacted consumer spending with retail sales numbers weaker and this fits with some anecdotal commentary about businesses experiencing a harder time passing on higher prices. Supply shocks continue to disrupt economies, with the COVID-zero policy in China and the Russia-Ukraine War further pressuring supply chains. Additionally, there is no fiscal or monetary backstop to support growth. We have trimmed our global growth forecast by a full percentage point to 3.6% and see risks skewed to the downside.

Risks have certainly been mounting, but there is still a strong underlying economy that gives hope of a “soft landing.” The underlying state of the US economy is better than what the 1.4% seasonally adjusted annual rate (SAAR) decline in the first quarter gross domestic product (GDP) would suggest. The massive deterioration in the real trade deficit, now at a new record, subtracted a massive 3.2% from GDP growth, more than offsetting the combined contributions from household consumption (+1.8%) and fixed investment (+1.3%). We should see a bounce back in the second quarter as trade and inventories normalize.

China’s lockdown has thwarted demand, but stimulus could provide a bounce. Strong household balance sheets and a robust labor market are supportive. Although a tight labor market can be associated with a slowdown in economic growth due to the impact on wages and profit margins, the strength across both businesses and consumers is encouraging.

Corporate profit margins remain sturdy and balance sheets are solid. State Street Global Markets notes that over 1,200 companies have reported globally and that most have exceeded analysts’ expectations, with sales surprises being particularly spectacular. While the majority of positive earnings surprises have been in the United States (US), earnings in Europe have also been solid.

Consumers remain healthy with Bank of America noting that consumers are still spending, with total transactions up 8% year over year with a shift toward services. This normalization of consumption patterns could help ease supply chain issues and in turn inflation. To the extent we are approaching peak inflation, the US Federal Reserve could soften their stance in the second half of 2022, which would be good for economic growth as rates will rise, but we are not in a restrictive policy at present. Lastly, although purchasing managers’ indices (PMI) for both manufacturing and services have generally slipped, they remain expansionary and are consistent with positive global growth.

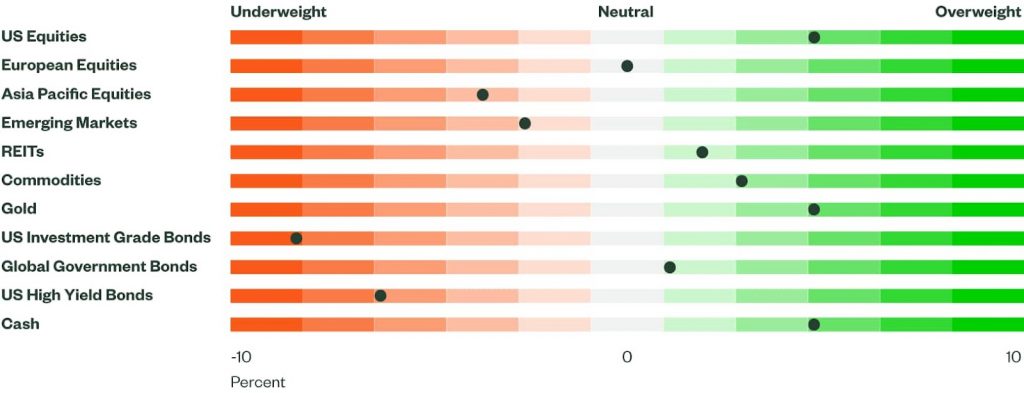

Figure 1: Asset Class Views Summary

Source: State Street Global Advisors, as at 10 May 2022.

Directional Trades and Risk Positioning

Investors have been digesting numerous risks that continue to threaten global growth and sour risk appetite. However, the fear may have peaked with our Market Regime Indicator (MRI) moving into a crisis regime. In our framework, a crisis regime typically means investors have become overly pessimistic, which could be read as a contrarian signal supportive of equities.

In April, our MRI began at high risk where it remained for most of the month. Another record inflation reading in April coupled with more aggressive comments from central banks, rising bond yields and further lockdowns in China weighed on the sentiment. The move into the crisis was driven by implied volatility on equity, which spiked over the past two weeks and now resides at the top end of high risk. Both risky debt spreads and implied volatility on currencies have remained elevated and reside in the crisis regime.

At our latest rebalance, we modestly increased our exposure to equities, now a small overweight, while reducing our allocation to US aggregate bonds. While the change in MRI drove our re-risk, our forecast for equities has improved and remains positive.

A difficult 2022 for equities has weakened price momentum but this is partially offset by improving valuations. Elsewhere, macroeconomic factors remain poor, particularly the macrocycle signal, but supportive quality and sentiment factors buoy our outlook.

Our forecast for aggregate bonds has improved but equities remain more attractive. Our models now expect a small decline in rates. Despite negative real GDP growth in the first quarter, higher nominal GDP relative to long-term treasury yields still points to higher rates. But with interest rates having risen so sharply, our model anticipates some reversion given the slowing PMIs and weakening momentum.

Relative Value Trades and Positioning

Within equities, we reduced our overweight to US equities to bring our Europe allocation to neutral. Our forecast for the US is constructive, and we remain overweight, but a material decline in sentiment relative to other regions helped produce an improved outlook for Europe, which drove our reallocation. Elsewhere, due to continued model deterioration in emerging markets, we rotated out of emerging markets and increased our previously underweight position in real estate investment trusts (REIT) to a slight overweight.

Within the US, we equally sold both small and large caps but maintained an overweight in both. Earnings season is wrapping up and the negative effects of supply chain disruptions, labor shortages and inflation are permeating our models through weakening sentiment scores. However, the US continues to benefit from robust macro factors, still positive price momentum and favorable quality factors.

Valuations in Europe remain enticing and while short-term price momentum is negative, long-term measures remain contributory. Additionally, advantageous sentiment, both earnings and sales, helps strengthen our Europe forecast.

Our emerging market forecast continues to deteriorate, especially dragged down by momentum and quality factors, which continue to worsen. Valuations remain appealing but are offset by poor macroeconomic factors. On the flip side, our REIT forecast continues to sit in positive territory due to beneficial price momentum, strong sentiment and healthy balance sheets supporting the asset class.

Within fixed income, improvements in our government bond forecasts prompted a rotation out of high yield and cash into intermediate government bonds and non-US government bonds. As mentioned above, our model is looking for a small decrease in the level of rates, which supports intermediate government bonds. Expectations for rates outside the US are mixed, but a likely positive impact from the currency aids the outlook for non-US bonds. For high-yields, recent weakness in equity performance, higher equity volatility and unfavorable seasonality dent the outlook. Further, higher government interest rates suggest more challenging financing conditions and higher spreads.

From a sector perspective, energy and materials remain favored while we rotated from financials to utilities. Financials still score fairly well in our models with strong earnings estimates and positive valuations. However, a meaningful deterioration in price momentum, both short and long term, weighs on our forecast and knocks them down in our rankings. For utilities, meaningful improvements in both sentiment and momentum, coupled with strong macro factors, reinforced our upgraded outlook. The sturdy supply and demand backdrop for energy has supported the sector, which is reflected in our models through a strong forecast.

Energy ranks well across most factors with exceptional price momentum and robust sentiment. Both sales and earnings helped to underpin our outlook for energy. Sentiment for materials has softened slightly but remains positive. Solid price momentum and attractive valuations buttress our sanguine forecast for materials.

This post first appeared on May 19th, 2022 on the State Street Blog

PHOTO CREDIT: https://www.shutterstock.com/g/pandorastudio

Via SHUTTERSTOCK

Marketing Communication

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

The views expressed are of Investment Solutions Group as of 10 May 2022 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor. All information is from State Street Global Advisors unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed.

There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Past performance is not a guarantee of future results. Investing involves risk including the risk of loss of principal.

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

For EMEA Distribution: The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research.

Equity securities may fluctuate in value in response to the activities of individual companies and general market and economic conditions.

Investing in foreign domiciled securities may involve risk of capital loss from unfavorable fluctuation in currency values, withholding taxes, from differences in generally accepted accounting principles or from economic or political instability in other nations. Investments in emerging or developing markets may be more volatile and less liquid than investing in developed markets and may involve exposure to economic structures that are generally less diverse and mature and to political systems which have less stability than those of more developed countries.

Investing in REITs involves certain distinct risks in addition to those risks associated with investing in the real estate industry in general. Equity REITs may be affected by changes in the value of the underlying property owned by the REITs, while mortgage REITs may be affected by the quality of credit extended. REITs are subject to heavy cash flow dependency, default by borrowers and self-liquidation. REITs, especially mortgage REITs, are also subject to interest rate risk (i.e., as interest rates rise, the value of the REIT may decline).

There are risks associated with investing in Real Assets and the Real Assets sector, including real estate, precious metals and natural resources. Investments can be significantly affected by events relating to these industries.

Bonds generally present less short-term risk and volatility than stocks but contain interest rate risk (as interest rates rise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Investing in commodities entails significant risk and is not appropriate for all investors. Commodities investing entail significant risk as commodity prices can be extremely volatile due to a wide range of factors. A few such factors include overall market movements, real or perceived inflationary trends, commodity index volatility, international, economic and political changes, change in interest and currency exchange rates.

Illiquid risk/Asset investments may have difficulty in liquidating an investment position without taking a significant discount from current market value, which can be a significant problem with certain lightly traded securities.

{kind=link}